Tax Reconciliation under IAS 12 + Example

When I was an audit freshman, my least favorite task was to prepare the income tax reconciliation. I frankly hated it.

Why?

The main reason was that I did not understand the purpose of it. For me, it seemed like a bunch of numbers and percentages that never add up and the magic table never gets balanced.

Our clients hated it too, especially if their transactions were complex, or there was a change in the tax rate or whatever happened.

Let me tell you my own story about the tax reconciliations. Sure, if not interested, then skip it and go straight to theory and example below.

Here’s the story…

Many years ago I was assigned to an audit team lead by very competent, but strict audit senior. Let’s call her Jess (not her real name!).

Jess was very hard working, clever and pedantic senior. Her working papers just looked great – all clean and neat. It was big pleasure to review them.

However, she was moody, vague, unpredictable and sometimes very unpleasant. She literally loved some audit assistants and praised them a lot and on the other hand, she could really dislike the other assistants and make their lives difficult.

You could never know in which category you were.

I was unlucky to end up in the second category. I have no idea why.

To this day, when we occasionally meet, we could barely look at each other and I even gave up greeting her, because she just never responded and looked straight through me like I was the air.

So, when I learned I would be in her audit team in a big manufacturing company with even bigger mess in the books, I instantly knew what would happen. And yes, it happened.

I was swamped in the worst and nastiest tasks you could ever imagine. I had to attend the inventory count in the cold freezing midnight of the New Years Eve (no dancing and having fun that year!). And yes, you guessed it – I had to check the client’s tax reconciliation and propose corrections.

That was the exercise! Worse than the stock count, believe me.

I understood one point: if I don’t make it right, Jess would give me very bad feedback and it can have bad impact on my future career in that company. After all – that was her goal.

Speaking in a really vulgar slang (please pardon me), I was working my butt off. I worked so hard to understand the tax reconciliation and to make it right for the client, but after the whole night staring at the worksheets, it was done – to the big surprise and dislike of Jess.

You know the old saying – when life gives you lemons, make lemonade.

Why did I tell you the story?

The reason is that based on my own experience I realized I could have saved a lot of time, if I would have taken the right sources of information and the right approach for tackling the tax reconciliation.

In this article, I’d like you to learn from my mistake, learn the right approach on the example and save the sleepless night ☺

What is the tax reconciliation?

The standard IAS 12 Income Taxes requires many disclosures, including the tax reconciliation.

It is the explanation of the relationship between the tax expense (income) and your accounting profit.

What’s the meaning of that?

Theoretically, you could calculate the tax expense as your accounting profit before tax multiplied with the tax rate applicable in your country.

In reality it does not work this way due to many different things, for example:

- Non-deductible expenses:

These are all items that you incurred, but you cannot deduct them for the tax purposes. In other words, you need to add them back for the purpose of your tax calculation. The examples are expenses for lunch with potential clients (in most countries), excessive petrol consumption, etc. Of course, it depends on your specific legislation. - Change in the tax rate during the period:

If the tax rates changed, then it affects the future periods and as a result, the deferred tax originated in the previous periods must be adjusted to reflect the new tax rate. - Adjustments related to previous periods

- Adjustments related to tax losses, etc.

- Adjustments related to changes in tax bases

- Adjustments related to changes in the manner of settlement or recovery

- Effect of foreign tax rates, etc.

Due to these differences you have to explain why your income tax expense is NOT equal to the accounting profit multiplied with the tax rate.

How to present the tax reconciliation?

The standard IAS 12 gives you the 2 options:

- Tax expense (income) reconciliation:

Here, you try to explain the differences between:- Your tax expense or income, and

- Your theoretical tax expense or income, which is your accounting profit multiplied with the tax rate.

- Tax rate reconciliation:

In this case, you explain the differences between:- The tax rate applied, and

- The average effective tax rate, sometimes called “theoretical tax rate”, which is your tax expense or income divided by your accounting profit.

Maybe it looks simple and easy and indeed it is in many cases.

Sometimes, the company has too many transactions with temporary differences that it’s really hard to prepare.

To illustrate it, let me show you the numerical example with a few tips on how to proceed.

Example: Tax reconciliation

Question

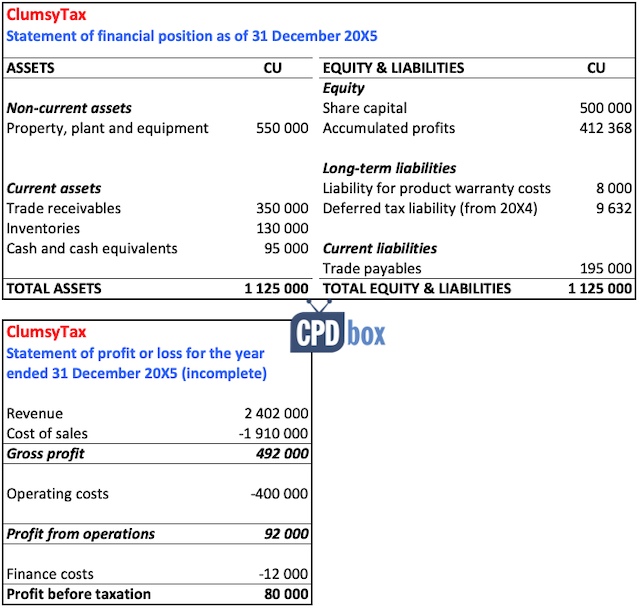

ClumsyTax is a manufacturing company preparing its tax information for the year ended 31 December 20X5. You have the following information:

- Depreciation expense for the year 20X5 allowable in line with tax legislation is CU 103 000. Accounting depreciation included in operating costs is CU 85 000. Cost of property, plant and equipment is CU 800 000 EUR and ClumsyTax deducted depreciation expenses of CU 208 000 in its tax returns prior the year 20X5.

- In 20X5, ClumsyTax increased a liability for product warranty costs by CU 2 500. Product warranty costs are not tax deductible until the company pays claims. Claims paid in 20X5 amounted to CU 3 100.

- Expenses for promotion included in operating expenses amount to CU 900. These are not deductible for tax purposes.

- Tax rate for 20X5 is 30% (28% in 20X4).

- The statements of financial position (before tax expenses) and profit or loss are below:

Calculate current tax expense, deferred tax expense and prepare the tax reconciliation.

Solution:

This example is a bit more complex, because you need to understand the tax reconciliation in the context of the financial statements, tax returns and other information.

It would not be very wise to show you purely this aspect without showing the full picture.

So, before any attempts to work on tax reconciliation, make sure you have the following information ready:

- The statement of financial position

- The statement of profit or loss and other comprehensive income

- The income tax return (or detailed calculation of current income tax)

- The detailed calculation of the deferred tax asset or liability as of the end of the previous reporting period

- The detailed calculation of the deferred tax asset or liability as of the end of the current reporting period.

Without having these 5 papers or worksheets in your hands, don’t waste your time and don’t start working on the tax reconciliation.

Step 1: Prepare all the necessary documents and calculations

We have n. 1 and n.2 in our hands, but we don’t have tax return and deferred tax calculations.

Let’s prepare the tax return first.

- Current income tax calculationWe will start with the accounting profit and then we will make all the necessary adjustments.

Deduct – total (C)-106 100Taxable profit (A+B+C)62 300Tax rate30%Current income tax18 690

Description CU at 31/12/20X5 Accounting profit (A) 80 000 Add back: Accounting depreciation 85 000 Provision for warranty costs (20X5) 2 500 Promotion expenses 900 Add back – total (B) 88 400 Deduct: Tax depreciation -103 000 Warranty claims paid -3 100 Note: You may well see that instead of deducting the positive difference between tax depreciation and accounting depreciation in one single number, I’d rather split this adjustment to 2 numbers. It’s much better for understanding how the temporary differences reverse.

- Deferred tax calculation – current yearThe best way is to put all the assets, liabilities and any other potential items (like tax loss) in the table and calculate the temporary differences and deferred tax there.

Item Carrying amount (A) Tax base (B) Temporary difference (C=A-B) Deferred tax (-30%*C) PPE 550 000 489 000 61 000 -18 300 Trade receivables 350 000 350 000 0 0 Inventories 130 000 130 000 0 0 Cash & cash equivalents 90 000 90 000 0 0 Warranty cost liability -8 000 0 -8 000 2 400 Trade payables -195 000 -195 000 0 0 Total -15 900 Notes:

- Insert assets with + and liabilities with –

- The tax base of PPE is its cost of CU 800 000 less tax depreciation prior 20X5 of CU 208 000 less tax depreciation in 20X5 of CU 103 000

- We applied the tax rate of 30% (applicable in 20X5)

- Deferred tax calculation – previous yearThis is also very important, because you need to reconcile how your temporary differences moved.

The method is the same as before, just use the previous year’s numbers and rate.

In this example, we do not have the financial statements from the previous year, so let’s focus only on the 2 temporary differences there:

Item Carrying amount (A) Tax base (B) Temporary difference (C=A-B) Deferred tax (-28%*C) PPE 635 000 592 000 43 000 -12 040 Warranty cost liability -8 600 0 -8 600 2 408 Total -9 632 Notes:

- Your deferred tax figure should be show in your balance sheet in the same amount (9 632)

- Carrying amount of PPE is the carrying amount as of 31-Dec-20X5 of CU 550 000 plus add back the depreciation expense in 20X5 of CU 85 000 = CU 635 000

- The tax base of PPE is its cost of CU 800 000 less tax depreciation prior 20X5 of CU 208 000

- Carrying amount of warranty cost liability is its carrying amount as of 31-Dec-20X5 of CU 8 000 plus add back the claims paid of CU 3 100 less deduct the amount newly created of CU 2 500

- We applied the tax rate of 28% (applicable in 20X4)

Step 2: Calculate the total income tax expense

The total tax expense consists of:

- Current income tax expense: CU 18 690 (from the calculation 1 above)

- Deferred income tax expense: CU 6 268 (see below)

Total income tax expense in 20X5 = CU 18 690 + CU 6 268 = CU 24 958.

The deferred income tax expense is calculated as a difference between:

- The deferred tax liability as of 31 December 20X5: CU 15 900 (calculation 2 above)

- The deferred tax liability as of 31 December 20X4: CU 9 632 (calculation 3 above)

Anyway, this is very important: It is necessary to understand how that deferred tax expense arose, just in case your tax reconciliation does not balance:

| Item | CU |

| Deferred tax expense related to PPE | 5 400 |

| Deferred tax expense related to warranty cost liability | 180 |

| Increase in DTL resulting from the increase in the tax rate | 688 |

| Total deferred tax expense | 6 268 |

Where did I get these numbers?

Let me explain:

- Deferred tax expense related to PPE is coming from your actual current income tax calculation:

- Accounting depreciation of 85 000; less

- Tax depreciation of 103 000;

- Multiplied with 30%.

- Deferred tax expense related to warranty liability is coming from your actual current income tax calculation:

- New provision in 20X5 of CU 2 500; less

- Claims paid in 20X5 of 3 100;

- Multiplied with 30%.

- Increase in DTL resulting from the increase in the tax rate is calculated as

- Opening balance of DTL of CU 9 632;

- Adjusted from 28% to 30%: CU 9 632/28*2 = CU 688.

Step 3: Perform tax reconciliation

We are almost done!

The only thing is to explain the relationship between:

- The accounting profit of CU 80 000 multiplied with the tax rate of 30% = CU 24 000, and

- The income tax expense of CU 24 958.

I’ve done that in the following table:

| Item | CU |

| Accounting profit | 80 000 |

| Tax at the applicable rate of 30% | 24 000 |

| Tax effect of non-deductible promotional expenses (CU 900*30%) | 270 |

| Increase in DTL resulting from the increase in the tax rate (in step 2 above) | 688 |

| Total income tax expense | 24 958 |

Good piece of advice:

If your tax reconciliation does not make any sense, go back your current income tax calculation and make sure that you included all items either in the deferred tax calculation or added them as your outstanding items here in the reconciliation (such as promotional expenses for which no deferred tax was recognized).

Alternatively, we can explain the relationship between:

- The average effective tax rate calculated as the tax expense of CU 24 958 divided by the accounting profit of CU 80 000 = 31,20%, and

- The applicable tax rate of 30%.

I’ve done that here:

| Item | % |

| Applicable tax rate | 30.00 |

| Tax effect of promotion expenses (270/80 000) | 0.34 |

| Tax effect of increase in DTL from the increase in the tax rate (688/80 000) | 0.86 |

| Average effective rate (same as 24 958/80 000) | 31.20 |

Finally…

Phew, that was an exercise!

It was very simple, but you can still see that there’s a lot of work in it and you can’t do it isolated from other things – you must prepare all your tax calculation while seeing the full picture and relationships.

My own experience tells me that the biggest troubles arise exactly in the deferred tax part.

Make sure that you have the clear deferred tax calculations from the current year and from the previous year and compare them with the current income tax return.

If you are sure that the reversals of temporary differences were correctly recognized in both your tax return and your books, then you’re on the best way to succeed.

Sleep well! ☺

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

101 Comments

Leave a Reply

Thank you for your education. May i know you how would have handled the example if the deferred tax balances brought forward were impacted upon by movement in FX rate?. This happens when the firm is booking in multiple currencies.

Wow! Great learning centre. This is amazingly good. Please keep it up. Silvia, thank you for the good work.

Hi Silvia thank you so much. do you share me an exell example (the general model) to calculate impairement on ifrs 9

Loving the course – thanks so much!

Hi Sylvia

Your deferred tax liability on PPE (previous year) needs to be R 12 040 and not R 12 400.

Yes, thank you, it was a typo!

is there any changes in retained earnings due changes in tax rate?

Hi Silva,

I have a question. I want to calculate effective tax reconciliation for a loss making company who is not obliged to pay tax due to being loss making. Hence, the company has untilized capital allowances brought forward and unutilized losses. In essence, no current tax was charged except deferred tax which has considered the unutilized losses and capital allowances in its computation. I learnt the only items that are reconciled are items of permanent differences which does not exist in the deferred tax computation. How do I go about this?

IAS 12 – DTA/DTL calculation explained in an easy and simplified manner. Good work.

Thank you so much Silvia, you have made my Tax life in this topic easier. I wish i could attend your lecture class live

God bless you, asante sana !

Thank you 🙂

Awesome piece…truly useful for auditors and tax professionals, I would spread the word!

That means , say my tax exemption period is 10 years from now, I have a PPE asset with accounting depreciation for 8 years and for tax purpose depreciate for 6 years. In this case there is no differed tax impact.

But , say if accounting depreciation for 12 years and for tax depreciation for 8 years, what will be the impact on deferred tax? can we eliminate those assets from my deferred tax calculation considering it as permanent difference ?

Also, should I take gratuity provision for my differed tax computation?

Appreciate very much if you could answer for these things.

Thanks & Regards,

Suneth ( Sri Lanka)

Hi Silvia,

Great explanation. thanks a lot..

Could you please tell me, whether there is any difference in computing deferred tax for companies which are exempt from income tax for a period of time (eg. 10 years)

Yes, there is – in the tax rate that you apply. So, if you expect that your deferred tax will reverse in the period of tax exemption, then you should apply 0% tax rate and the deferred tax will be zero as a result. Please read more here.

Pleas help! If there is loss before tax then how to make reconciliation ?

If I understand well, tax base = Cost Value – (Accumulated Accounting Depreciation – Accumulated Tax Depreciation)?

No. Tax base = cost – accumulated tax depreciation.

Thanks Silvia. Topic that that I’m very much fond of.

Hi Silvia

Is your course covers IFRS 17 and IFRS 4?

Hi Sam, none of them – it’s insurance, very specific and not examinable in most exams. Majority of my students does not need it, so I did not cover it. S.

Good example

very hand nothing has frustrated me in preparing Tax Returns other than Cashflow and Tax

Hi Silvia,

I always look forward to your emails. This tax lesson is very informative and helpful to me. I understand deferred tax much better now. Co-incidentally I was just about to calculate my company’s deferred tax for the period and you have made it a lot easier for me to do so. Thanks a million!

regards Tara

Great, glad to help 🙂

thank you so much

Dear Silvia,

I would like to thank you for this great article and of course it really helped me.

About the story – I am one of the accountants who hated my job and sometimes I felt I was incompetent due to failure to apply the rules and I found them to be complicated.

But since I came to know you through your work I have increased interest in studying IFRS and I can now see bright future in my Career.

Welcome to Tanzania (The Land of Kilimanjaro, Serengeti and Zanzibar)

Thank You and Stay Blessed.

Msafiri.

Hi Msafiri,

for me, that’s absolutely great to read, because thus I know that my work is sensible and really helps. All the best! S.

Dear Silvia,

That was a great article. It is a “forever” handy tool for every accountant any time she/he wants to do tax reconciliation for IFRS12. Thank you very much for this selfless post and God Bless!. I was in Kenya so I know that Asante means Thank you and Asante Saanaa means Thank you very much. In my language, Tamil, we say “Mikka Nan(pronounced as nun)dri” (Thank you very much)

Hi Ravi, thank you, wow, I will have to keep the spreadsheet with “thank you” in so many languages 🙂 Glad to help! S.

From Kenya, asante sana Silvia(Swahili word for ‘thank you’).

I’ve learnt in a simple yet profound way what I’ve been trying to hack since my accounting class.

Thanks Peter for teaching me my first Swahili word 🙂 Glad you like the article!

S.

you are a lifesaver i now understand IFRS clearly, well explained thanks.

You are a rare gem Silvia. Please keep it up. I have never been able to tackle this aspect of reporting disclosure. With this article, I am certain I will get it right this year.

Thank you so much Silvia for this wonderful and informative piece.

thank you so much silvia

Hi Silvia

thanks for every think

bout i have question about other subject which is what is the Puttable Financial instruments some examples and who we recognize it under IAS32 and IFRS 9?

hello Silvia ,this is very insightful and informative. Keep it up

Hello Silvia, thank you very much for those articles on this blog. It’s a great ressource!

I have just a doubt: I was wondering about when we are reconciling the Accounting profit*30% and the total income tax expense, why we are not showing the impact of the depreciation.

Is this because depreciation is only a question of timing while the marketing expenses are never going to be considered as tax deductible?

Or is there another reason?

Hi Marc,

the reason is that depreciation effect is included in the total tax expense of 24 958, because it comprises both current tax and deferred tax – therefore no point to include it twice. So yes, you were practically right in answering yourself 🙂 S.

Dear Silvia,

Many thanks for this expose; tax reconciliation really made simple.

However, can it be inferred that tax reconciliation only focuses on non-deductible items that will never reverse?

Kind regards.

Hi Oja,

in fact no, because tax reconciliation focuses on all items “outside” the current and deferred tax, plus any changes. So, while depreciation is included in the deferred tax, non-deductible promotion expenses are excluded from both current and deferred tax and that’s why they are reconciled. Also, the effect of change in the tax rate is a separate item. S.

Hi Silvia,

You never know what impact your practical story as above and the tutorial on this most disturbing topic, have made on me and the generality of your subscribers. in fact, i am really impressed with the way you brought it home. Kudos Silvia. Good health of mind and body i wish you, so you could continue in this quest of creating outstanding Accounting Professionals all over the world.

Thank you, Chidozie, I am really happy to help and inspire you. Besides tax reconciliation, I just wanted to cheer up all the people suffering under moody bosses. I survived a few of them and I am thankful to each of them, because they really helped me grow, taught me to manage stress, tough situations and dealing with difficult people. And sometimes you must understand that it’s not worth trying to deal with someone, just let him be and go. All the best! S.

I was teaching mathematics 7 years ago and now I become accountant and quite teaching. I took many pedagogical courses that will help teachers teach their students in a simple. But you are really created for teaching and keep up on it and I am sure you will create great number professionals in the world which is great for your and make you unforgettable forever. I am from Ethiopia.

Thank you, Feleke, much appreciated! S.

Kudos IFRSbox! Thank you Sylvia!

Hi Sylvia, very informative. One question though. In another article focussing on deferred taxes you explain that in order to get the correct symbols (+ and -) its is best to deduct tax base from carrying amount. Here it is done the other way around. I’m a little confused by it. Thanks for the rest.

Hi Rachel, I’m not sure what you mean, but I have another article focusing on tax bases here, maybe it helps. S.

insightful. Well appreciated.

Silvia, thank you very much.

Your skill is incredible

Silvia is the best tutor

It is very informative and keep up it

so, Thank you very much

Thank you a lot Silvia for the Article.

I do like the story, it is so inspirational and motivational especially to us who are Freshers in the profession.

Hello Silvia,

I was overwhelmed by going through your article on tax reconciliation. It has been explained in the best possible way. Although I was able to workout the tax liabilities for my company but was not confident enough with the process followed. On going through this article , now I am confident to handle the subject.

I with my colleagues would like to thank you for your great effort in enhancing our accounting concepts.

Thanks a lot , all are liking this post very much .

Regards

Sunil

Thank you, Sunil, I appreciate. I really like that you told me how the article helped. It’s important for me to know! Best, S.

Thank you for the beneficial article.

It is very informative.

Hello Silvia,

I have a couple of questions that are outside the scope of this topic.

1- If we have a building owned by us. we are using half of the building as a head office and the other half is rented to third party as operating lease. Can you please guide regarding the treatment of that part that is rented, I refer to the investment properties standard that the asset should be separated and reported as investment property but in our case the asset is partially rented. should we report the total asset as PPP?

2- stand alone FS for a parent which has two subsidiaries, does it mean that we should account for this subsidiary under equity method or cost method?

Thanks for your time.

NO HESHAM, U CANNOT CONSIDER WHOLE PPE AS OWNED, U HAVE TO DO SPLIT ACCOUNTING. TREAT THE RENTED PART ACCORDING TO IAS 40 AND OWNED PART ACCORDING TO IAS 16.

Thanks Moazam for responding!

As for the point 2 – under IAS 27, you have a choice – either you apply cost method, or equity method or you will treat it as financial instrument under IFRS 9. S.

Thanks Silvia for your response. It is clear now.

Many tanks again.

Thanks Moazam for your response. I guess split should be based on the FV for each part of the building, right?

Thanks your advanced

Excellent article on the Tax reconciliation. You have this uncanny knack for making the Extremely complicated simple. You have no idea how scary this part of the financials is to many of us auditors. My colleagues will be delighted. Loved your story too by the way.

Thank you, Stephen, glad you like it 🙂

Fantastic

Thank you so much Silvia. This is insightful as always.

Hi Silvia,

You are a gem. Your knack of getting to the kernel of the matter is appreciated. Your insight continues to inspire, and we are opportuned to drink from your fountain of pratical knowledge. Please do not relent, we are grateful. Many thanks.

Ibe Nwankwo

Dear Silvia,

Well explained, Thank you.

Dear Silvia,

Excellent as always

Thanks a lot for the wonderful knowledge. please keep it up