Summary of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations

When a company (or another entity) plans to sell an asset and / or stop some part of its business, then it might affect its future cash flows, profitability and overall financial situation.

Therefore, the users of financial statements, mainly investors, should be informed about these events.

That’s why the standard IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations was issued – to highlight the results of discontinued operations and to separate them from the results of ongoing or continuing activities.

So, if you or your company plans to sell some non-current assets and discontinue some operations, then IFRS 5 is for you.

The only exception is when a company regularly sells assets normally considered as non-current. In this case, these sales represent one of primary activities and the related assets are inventories in fact. For example, a car dealer presents all vehicles for resale under IAS 2 Inventories, not under IFRS 5.

Let’s take a closer look to the main IFRS 5 rules.

Objective of IFRS 5

IFRS 5 focuses on 2 main areas:

- It specifies the accounting treatment for assets (or disposal groups) held for sale, and

- It sets the presentation and disclosure requirements for discontinued operations.

Let me point out that you should apply IFRS 5 for all non-current assets – no exception.

The standard IFRS 5 lists some measurement exceptions and you can read about them in the later paragraphs, but you still need to present and disclose the information about these assets under IFRS 5.

When to classify an asset as held for sale

You should classify a non-current asset as held for sale if its carrying amount will be recovered principally through a sale rather than continuing use.

The same applies for a disposal group.

Disposal group is a new concept introduced by IFRS 5 and it represents a group of assets and liabilities to be disposed of together as a group in a single transaction.

For example, when a company runs a few divisions and decides to sell one division, then all assets (including PPE, inventories, deferred tax, etc.) and all liabilities of that division would represent a disposal group.

What if we abandon an asset?

The question is whether you should classify a non-current asset as held for sale in the case when you plan to stop using it, or abandon it.

The answer is NO.

Why?

Because, you will recover its carrying amount through asset’s continuing use and not sale.

What does it practically mean?

Well, it means that you will NOT apply “held-for-sale accounting”, i.e. you will NOT keep an asset at lower of fair value less costs to sell and its carrying amount (as specified below).

But, it also means, that you WILL need to assess the criteria for presenting the abandoned asset or operation as discontinued operation.

When will an asset be recovered through a sale?

In other words, what are the conditions for classifying an asset as held for sale?

First of all, the asset or disposal group must be available for immediate sale in its present conditions and the sale must be highly probable.

IFRS 5 sets a few criteria for the sale to be highly probable:

- Management must be committed to a plan to sell the asset;

- An active program to find a buyer must have been initiated;

- The asset must be actively marketed for sale at a price reasonable to its current fair value;

- The sale is expected to be completed within 1 year from the date of classification;

- Significant changes to the plan are unlikely.

The similar criteria also apply to assets held for distribution to owners.

How to account for assets held for sale

Once you classify an asset or a disposal group as held for sale, then you should measure it under IFRS 5.

However, IFRS 5 lists a few measurement exceptions (IFRS 5.5):

- Deferred tax assets (IAS 12 Income Taxes).

- Assets arising from employee benefits (IAS 19 Employee Benefits).

- Financial assets within the scope of IFRS 9 Financial Instruments.

- Non-current assets that are accounted for in accordance with the fair value model in IAS 40 Investment Property.

- Non-current assets that are measured at fair value less costs to sell in accordance with IAS 41 Agriculture.

- Contractual rights under insurance contracts as defined in IFRS 4 Insurance Contracts.

When you classify any of the above types of assets as assets held for sale, you continue measuring them under the same accounting policies as before classification (e.g. financial instrument held for sale will still be measured under IFRS 9, not IFRS 5).

Why have we classified these assets as held for sale though?

The reason is that although you don’t change their accounting treatment, you change their presentation and disclosures. You will still need to present these assets separately from others and disclose some additional information.

All other assets not excluded in the above list must be measured at lower of their carrying amount and fair value less costs to sell. That’s the main measurement principle of IFRS 5.

How to do it?

Measurement after classification

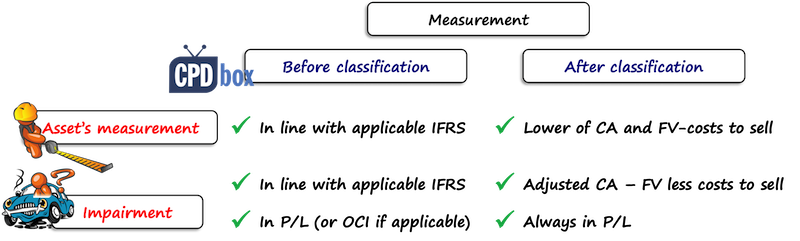

Immediately before you classify an asset as held for sale, you should measure it under applicable IFRS. For example, you would measure an item of property, plant and equipment under IAS 16.

Subsequently, after you classified an asset as held for sale, you should measure it at lower of its carrying amount and fair value less costs to sell (except for measurement exceptions listed above).

Impairment

With regard to any impairment, immediately before classification as held for sale, the impairment is recognized in line with the applicable IFRSs, for example, under IAS 36 for property, plant and equipment.

In this case, you would recognize any impairment loss in profit or loss, but sometimes also in other comprehensive income – that’s when you apply revaluation model for your property, plant and equipment and you have a revaluation surplus to decrease.

After you classify an asset as held for sale, you would recognize any impairment loss in profit or loss only.

What are discontinued operations

IFRS 5 specifies that you need to pay special attention to presenting any discontinued operation. But, what is it?

It is a component of an entity (understand: a cash-generating unit or a group of cash-generating units) that either has been disposed of or is classified as held for sale, and at the same time:

- Represents a separate major line of business or geographical area of operations,

- Is part of a plan to dispose it of, or

- Is a subsidiary acquire exclusively with a view to resale. (IFRS 5.32)

How to present discontinued operations

Once you identify a discontinued operation, you should present it separately from other continuing operations in your financial statements.

Thus, the readers of your financial statements will be able to see what you put away and what you keep going on in order to generate future profits and cash flows.

More specifically, you should present (IFRS5.33):

- In the statement of comprehensive income: a single amount comprising the total of:

- The post-tax profit or loss of discontinued operations, and

- The post tax gain or loss recognized on the measurement to fair value less costs to sell a or on the disposal of assets or disposal groups.

The analysis of a single amount shall be reported in the notes or in the statement of comprehensive income.

- In the statement of cash flows: the net cash flows attributable to the operating, investing and financing activities of discontinued operations. You can present these disclosures in the notes or in the financial statements themselves.

- In the statement of financial position (IFRS5.38): you shall present a non-current asset or assets of a disposal group classified as held for sale separately from other assets. The same applies for liabilities of a disposal group classified as held for sale.

Please watch the following video with a summary of IFRS 5 Non-current Assets Held for Sale and Discontinued Operations:

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

117 Comments

Leave a Reply

Hi

If you run a car business and you sold 8 cars for R80000 each, 15% vat inclusive.

The mark up is 45%

What will be the income earned from the sale of vehicles?

Will it be R640 000 or do you deduct the vat amount that is included in the R80000 for each vehicle and then income would be R 556520

Regards

Hi Silvia,

Thank you for this. I have a question relating to a parent and subsidiary A who signed an agreement to transfer lease and customer contracts from subsidiary A to parent by end of 2020. Would ROU recognized on leases be required to be accounted for under IFRS 5 in subsidiary A’s book? There is a buyer, but the asset was not actively marketed for sale.

Thanks and regards,

Sa

Hi Sylvia,

In line with IFRS 5, we are to present the assets and liabilities of subsidiary held for sale as one line. My question is how about the components of equity? Do we present it as one line as well for a subsidiary held for sale? For example, a line that says “Amounts in equity relating to non-current assets held for sale”.

Hi Josh, although not explicitly said in the standard – yes, you in fact do need to present it separately. The reason is that you need to present the elements of total comprehensive income separately and that affects the equity, too. I recommend looking at the Example 12 of Implementation Guidance related to IFRS 5 published by IASB.

Can anyone please advise me on the following case

The company abandon the operation before the start of business and end up in paying compensation for the landlord from whom the building is to be leased.

Well, Fahim, what advice do you need? I think that the company just generated expenses.

Thanks Sylvia

How should this expense be treated?

Can the treatment be as per IFRS 5 or to be considered as an operation expenses

Hi Silvia,

If the Group has sold subsidiary company (the major seperate business line) in 2018, but has not prepared financial statements for previous years. When preparing financinal statement for 2016 should it present that subsidiary sold as held for sale? In 2016 they did not plan to sell that subsidiary.

Hi Silvia,

Your article has indeed elevated my knowledge of IFRS 5. My question is how do we value “Adjusted Carrying Amount” when measuring Impairment after classifying as held for sale? Is it the lower of Carrying amount and Fair Value less cost to sell?

Regards

Dear Slivia

If a company has a wholly owned subsidiary for 10 months in the year and then dilutes its shareholding such that the sub becomes a JV, will this be treated as a discontinued operations?

hi Ebarume, no, this will be treated as a change in a group composition.

Dear Silvia,

The company is in a process of selling its subsidiary, a factory (which is a company as well). Meanwhile, the factory is working full-time and producing goods. Should the factory stop being depreciated? And if so, in its separate financial statements there would be no depreciation and it’ll be extremely profitable?

I simply love you mam! So nice of you to help us out in a quick and easy manner. Lots of love and respect for this effort.

Hi Silvia, I want to thank you so much for your website and explanation to IFRS, it has demystified financial reporting for me.

Thank you.

thank you mam for your nice mail

Hello Silvia and everyone.How to split deferred tax between disc. and cont. operation as per IAS 12.81h and IFRS5 33.b.How to split current tax as well?,current and comparative year.Thank you everyone.

Hello Silva,

If we classify an asset held for sale, Initially we remeasure it as lower of Carrying amount & FV, after one year if we are unable to sale the asset and against want check their values. After one year the FV-CTS is greator than CA, then what to do ? Shall we increase the value upto FV-CTS of NCA-HFS ?

Regards,

Mubbashir

thank you

Hi Silvia,

Congratulation for your website and thank you for your contribution

I want to ask you if XYZ company sold one of it’s subsidiaries on August 31, 2018, also they decided to sell this investment on August 2, 2018. my question is

Q1: Does this comply with terms of discontinued operation?

Q2: Do I need to present discontinued operation if i want to prepare Interim Condensed financial information for Q3 as of Septmber 30, 2018 or is this represent disposal such as any disposal in assets?

Q3: The gain or loss of disposed this subsidiaries = Cash proceed – carrying amount of net assets or Do I need to evaluate the investment sold at fair value at the date of disposed?

Hi Silvia

I would just like to find out, if the entity is transferring their assets to another entity at no consideration, does IFRS 5 still apply

I have a division which is part of plan to disposed off. In basis of preparation we write it as a non going concern but management wants that just after profit and loss we write ”the above results are from continuing operations ” .is that correct?

1. What if the Disposed Non Current Assets were never stated as Non-Current Assets Held for sale in the

Statement of Financial Position before sales commenced.

2. When is proceed on disposal of Non-Current Assets stated as other Income? Is the income here the net of the proceeds and Net Book Value(Carrying Amount) or just the proceeds?

Dear Silvia,

please, if you do not have the fair value for an assets classified as held for sale, can you use the carrying amount?

Dear Sylvia,

a company bought demolished factory (land, buildings, equipment), with the intention to reorganize the business and start the production again. It is completely separated from the business the company is usually in. The price paid was the estimated fair value. However, the plans for reconstructing were not fulfilled, and the management decided to sell the factory. The fair value was estimated again, company actively searched for a buyer etc. Two buyers actually attended the sale process, paid the deposit, however, eventually both of them gave up on buying the factory for other reasons. On December 2017, it was more likely than not that the carrying amount of assets will be recovered through sale rather than trough continuing use. Management has not changed the intention to sell the PPE after December 31, however, it does not seek for a buyer anymore actively. They are disappointed with the fact the first sale was so unsuccessful. None of the buyers indicated that the price is too high. Should the property, plant and equipment be classified as held for sale as of December 31?

your contribution is remarkable and unforgettable is only GOD will reward you for that, i will be happy if you can help me with CD lecture. thank you very much.

Dear Silvia.

If there is an increase in the fair value less costs to sell, BUT there is no measurement model given (cost or revaluation method). Do you just do an adjustment on the fair value that has increased?

Do you simply just Dr Non-current assets held for sale and Cr Fair-value adjustment?

I’ve really been struggling with this. Please will you help me?

They are still planning on doing the sale. They haven’t made the sale as yet

Dear Silvia,

Thanks for your knowledge sharing. A quick one, if a disposal group is held for sale in year 2017 and assets and liabilities presented as a separate line in the financial position, what happen to comparative year 2016, are we going to retrospectively classify in 2016 too?

If we classify an investment in JV (Equity Accounted) as held for sale in a mid year, will we end the equity accounting on the date of classification by considering only the proportionate profit (Upto the date of classification calculated pro rata on time proportion) or the whole year profit?

My question is for after the asset is sold over a year end. Putting some numbers to this:

cash proceeds 110

Carrying value 100

expenses to sell (charged to P&L in year occurred) 10

The 110 comes in, you relieve the assets held for sale of 100, what about the 10. RE or gain?

It enters into the gain/loss on derecognition, i.e. in your case the gain = 0.

Dear Silvia,

Your articles & videos are quite understandable and helpfull. Easy for a student too.

Q: Once the NCA is classified as HFS what is the accounting treatment if management subsequenlty withdraw the decision and want to reclassify from HFS to NCA after reporting date.

Dear Silvia, thank you for the great articles!

I have a question, when there is a discontinued operation recognized (NOT held for sale) we report this division separately, and we depreciate all assets as before or we stop depreciating as in the case of assets held for sale? Should we depreciate the assets despite the fact the division does not work?

Thank you!

Dear Lexo, as soon as you have discontinued operation, then you have to perform impairment testing of your assets. That should give you the answer. You recognize the impairment loss first. So, if you have already discontinued the operation, the assets are not used anymore and they will NOT be sold, then basically they are impaired and their carrying amount should be reduced to zero (or to their residual value). Also, if you are not using the assets and will not use them anymore, it means their useful life is over and they should not be depreciated. S.

Hi Silvia,

Many thanks for all materials you’ve prepared on IFRS.

I was wondering, if a company sells a (significant) subsidiary within the year and had no plans to in prior year: it has not been classified as held for sale in prior year’s financial statements. In that case (argueing that the subsidiary represents a major line of business), does the disclosure of discontinued operations apply?

And coming to think of it, in case of a loss on shares: should an impairment on assets (mainly PP&E) have been performed first?

Thanks in advance!

Oh and one more question: according to your guidance, the presentation of result from discontinued operations is not included as such in the income statement (but in the comprehensive income staement). When I lookup guidance from a Big4 firm, they note that the income statement should reflect the result form discontinued operations as well. Is this mandatory in case of discontinued operations? IFRS seems to speak about the comprehensive income statement only.

Dear Siliva, thank you so much for the information provided on the website, it’s very useful.

If a disposal group has been disclosed as held for sale, does it impact going concern considerations?

Thanks in advance.

Regards,

Cathy

Hi Silvia,

I would like to ask that if a company has a reportable segement (a division in opertion) and related PPE items (land, building and equipments) as per IAS 16 and during the year stop the operations and rent out the whole division to its subsidiary company. Whether it is a discontinued operation as per IFRS – 5? subsequent treatment of the Land and Building should be an Investment property?

Regards,

Asad

Hi Asad, if you stopped operations in that division, then yes, it’s a discontinued operation and you should report it separately from other assets. However, at the same time, if you are not going to sell the division, it is NOT classified as held for sale and not accounted for as such. If you are renting the land and building out, then it’s logical to classify it as investment property under IAS 40.

Thank you for your reply, however I need to correct one point in the query i.e. the operations were in fact not stopped but the division was transferred to the other entity on on-going basis. Now, would there be any change in treatment?

Regards

Asad

Hello, Silvia your teaching materials including Video lecture regarding IFRS is so interesting. You are contributing more. Thank you for your effort.

Dear Silvia,

A Group disposes of a subsidiary that does not represent a separate major line of business or geographical area of operations. It has a supporting function to Group’s operations. My understanding is that this case does not respresent a discontinued operations, and income and expenses of disposed subsidiary should be consolidated line by line till the date of disposal (and not in single line of discontinued operations). Is this correct?

Yes.

Hi SIlvia.

In a similar case as above, except that the management has not disposed the subsidiary yet. Assuming that it meets the criteria of NCA held of sale. However, the subsidiary is not considered as a separate major line of business and hence does not represent a discontinued operation, should it still be classified as an NCA held for sale then?

Or in other words, should both NCA held for sale and discontinued operations go hand in hand?

Many thanks for your help in advance!

Hi Max, I explained the link between NCA held for sale and discontinued operations above, in my reply to Hesham – I would be just repeating what I wrote there. You can have an NCA without considering it “discontinued operation”.

Hi Silvia,

Thanks a lot!

Hi Silvia,

I read some of the comments below, and someone asked about how you would treat an abandoned asset. So once a company decides to abandon an asset, an impairment test should be performed. It is discontinued operation in income statement. How do you recognize it on balance sheet? since the company doesn’t use it anymore, does it remain on the book and get depreciated? (but what is the useful life?) or can we just write off the whole asset? and recognize loss under discontinued operation in income statement? Please clarify, thank you.

James

Dear Silvia,

thank you for your knowledge sharing, simply amazing. Related to the topic, I have a question relating to impairment reversal.

In 2015 we decided to sell a hotel and recognised it as asset held for sale. Following the requirements of IFRS 5 we performed valuation, which showed impairment loss, which was booked in P&L. During 2016 negotiations with buyer took place. The contract was signed on January 5, 2017. The question: is this adjusting or non-adjusting event? The price was higher than what was estimated in 2015, therefore the quesiton is, whether impairment reversal should/could already be recognised in 2016? Thank you for your view.

Dear redhotar,

this is non-adjusting event in a sense that you DO NOT recognize revenue in 2016, but in 2017. However, as for the reversal of impairment loss, I would recognize it in 2016. The reason is that by 31 December 2016, you have already got the sufficient evidence that the fair value of a hotel is much higher than its carrying amount. The evidence is that the sale contract has been prepared and the price and everything were confirmed by the seller. S.

Dear Silvia M, Thank u very much for the articles indeed! Can you please help me on following questions?

1)Is this IFRS equally applicable for NGO’s FS repoeting?

2)In case the management didnt classify asset group for sale in prior financial year,but slod a group of asset on following year.will this issue be treated as a departure from IFRS 5?

Hi Silvia,

We have recently sold a part of business (several retail properties out of larger group) and we have determined it is discontinued operations as it is a strategic shift. I have a query regarding the disclosure for the Financial Statement. The properties were all sold in the this year and the transaction was only known about a month before it happened., hence we never moved them to held for sale in the prior year Financial Statements. On completion, any associated carrying values were disposed off against the proceeds received. The carrying values were taken as is (i.e. not measured at FV less costs to sell). It assumed this is lower than the FV. There were also several costs associated with disposal that are not “costs to sell” i.e. redundancy payments as a result of the restructure but not directly related to the

MY question is 1) We need to disclosure the net profit on sale (and should this be the proceeds less the carrying value of net assets less direct sale costs?). We assume the FV less costs to sell is lower than the carrying values.

2) How do we treat the other expenses incurred but not directly related to the cost to sell. (costs that would not have occurred if the disposal hadnt happened but are not a cost to sell, so should not form part of the gain or loss on disposal). Do these form part of the costs associated with the discontinued operations (i.e. added to thh operating costs of these properties for the 6 months they operated?) or can we show these in an exceptionals line / separately?

Many thanks for your help.

Sarah

Dear Sarah,

in the statement of comprehensive income, you should dislose one single amount that comprises of:

– post-tax profit or loss of discontinued operations (I guess all the related expenses would come here) and also

– post-tax gain or loss recognized in the re-measurement to fair value less costs to sell or on the disposal of assets constituting the discontinued operation.

So, profit/loss on the disposal and all other revenues and expenses of discontinued operations enter to one single amount (i.e. no “exceptionals line”).

However, you need to provide the breakdown of this amount in the notes to the financial statements (or on the face of the statement, as you wish).

You need to show the revenues, expenses, pre-tax profit or loss, gain or loss on the remeasurement of assets to fair value less cost to sell and gain or loss on the disposal, plus tax expense.

It means that if you derecognized your assets in their carrying amounts on disposal without revaluation to fair value less cost to sell, it’s OK, but you need to analyze total gain/loss on the disposal and calculate the amount attributable to remeasurement to fair value less cost to sell, and amount representing the gain/loss on the disposal. It’s an exercise, but you need it for your notes.

S.

Hi Silvia,

If an operation is discontinued, can you please help me understand how the comparative figures should appear on face of statement of financial position ?

For E.g. Inventory during comparative period as at 2015 was $20,000 and $7,000 is part of discontinued operation.

Now when we prepare Statement of financial position for continuing operation the comparative period 2015 should be $20,000 less 7,000 = $17,000 ? or should we still show as $20,000 for continuing operation

Please advise.

Thank you!

Dear Sudhindra,

I’m not sure I got it fully. So, you say that in 2015, inventory in continuing operation was 13 000 and discontinued 7 000 = total 20 000.

And now, in 2016, you don’t have any discontinued operation as it’s gone, so you’re asking how to present 2015?

If that’s the case, then you should present 2015 exactly as the last year, i.e. in the split between continuing (13 000) and discontinued (7 000) operation. In 2016, inventory for discontinued operation will be 0.

I hope it’s what you asked. S.

Hi Silvia,

Hope you are well. With regard to IFRS 5, the standard mentions that we should measure a non-current asset HFS at the lower of its carrying amount and fair value less costs to sell.

Given the context, can we expense all related expenses (i.e. consultancy fees/ professional fees etc.) against the sale transaction?

Dear Ashvin,

if consultancy fees and professional fees relate directly to the sale of your asset, then yes, these should be taken into account when estimating asset’s FV less cost to sell. S.

Hello silvia! Thanks for the good work and helping us. So if i understood correctly, then i shall only disclose the profit/loss from discontinued operation separately in PL and do not classify its assets as separate line of item in SOFP, if i do not intend to sell them. Likewise, i want to sell a CGU which is not discontinued but running in loss, i hv to present its asset separately in SOFP as Classified as HFS, but do not give separate disclosure of its Profit/loss in PL? And i do both wen its discontinued aswell as i intend to sell them. Right? Sorry for the long question.

Ahsan,

I think you got it just partially right.

For discontinued operation – you do disclose it separately in both P/L and balance sheet. Assets held for sale – on top of disclosures, you need to measure them at fair value less cost to sell. So, if you want to sell a CGU, then it’s both a disposal group (asset held for sale) and discontinued operation (by definition), and therefore you need to measure it at fair value less cost to sell + disclose it separately in your P/L and SoFP. S.

Hi Silvia, congratulation for your website and thank you for your contribution, I have a doubt, when a company plan to close, can I present PPE as a assets held for sale? or as an impairment. Thanks and regards

Dear Edmundo,

if you just plan to close, but not to sell, then your PPEs are NOT assets held for sale, but they definitely ARE discontinued operation. Therefore, you need to test assets for any impairment and at the same time, you need to present them separately from continuing operations in your financial statements (well, if a company plans to close one part of a business).

Be careful, because when a company plans to finish the closure within 1 year, then it’s NOT a going concern. S.

Hi Silvia,

Following Edmundo Gomez s question, in his case, shall we cease depreciations after booking impairments?

Thanks!

Hi Serena,

yes, of course. You depreciate carrying amount (that is AFTER recognizing an impairment) over remaining useful life. S.

Hi Silvia,

Thanks for your reply.

Following my previous question, in the case that an asset is idle, shall we still depreciate the asset’s carrying amount (after impairment posting) over its remaining useful life?

Hi I would like how to account the asset held for sale if the sale is not yet completed during the following year. I have a subsidiary which we intend to sale hence we classified it as asset held for sale. During the middle of the following year, we have not completed the sale yet. How can we account the asset held for sale and the accounting for the discontinued operation.

Thanks!

DB

Hi DB,

you do account for it under IFRS 5 – the only exception is that you should discount the cost to sell to its present value. S.

If your sale is disturbed by uncontrollable factors then you can classify under IFRS-5.

But if sales are not happened by controllable factors then you should reverse the entry..

This article was really helpful to me thank you so much Silva

Thank you Silva. Explanations are really great.

Thank you Silva. Your explanations are fantastic and very enlightening.

Thanks Silivia for your articles. Keep it up . We follow up them and learn from you .

Hello Silva,

Thanks for this wonderful article.It really made my day.

Hello Silvia,

Your articles are enlightening. Thanks.

@Hesham, as per your 2nd question,I think the segment should be classified as discontinued operations. That is if that segment represents a separate major line of your company’s business.

The standard described Discontinued operations as such component of an entity (understand: a cash-generating unit or a group of cash-generating units) that either has been disposed of or is classified as held for sale, and at the same time:

Represents a separate major line of business or geographical area of operations.

Is part of a plan to dispose it of, or

Is a subsidiary acquire exclusively with a view to resale. (IFRS 5.32)

Hi Joel,

thank you for your comment. You are right, but it’t not the whole truth. Yes, it’s a discontinued operation, but there are also assets or disposal groups held for sale too. Please see my explanation below Hesham’s comment. S.

Q – If asset measured FV and then categorized “Non-current asset held for sale” which point we need to reverse the revaluation gain in OCI to PL?

Q – Because you change the plan of asset and you going to sell the asset within one year, so can we still keep the revaluation reserve as it is?

Dear Chintaka,

good question – IFRS 5 does not say anything about it and IAS 16 says that you reclassify the revaluation surplus in equity when you derecognize the asset. In my opinion, I would leave revaluation surplus as it is until asset is derecognized. S.

Please tell me about as when we purchase assets what will be happen in accounting cycling.

hello Sylvia,

I just want to ask you, if NCA hed for sale is not classified as held for sale, the financial statment should be restated? or all the adjustments should be done in the current year.

thank you

Dear Silvia,

I use this opportunity to thank you so much for your great website, articles and videos that really helped us a lot. I would like to discuss the difference between the assets held for sale and the discontinued operations. Are they linked together or not? Can you please differentiate in the concept between them?

Another Q, if a segment at our company would be sold in the next year and there is a plan for the sale and other conditions are met, will be classified as held for sale or discontinued operations? I see both concepts are same but do not know when a company can recognize the first or to recognize the second. sorry for the long question.

Dear Hesham,

I understand your confusion. So:

1) Yes, these 2 are closely linked. Sometimes, they are identical, sometimes, assets held for sale is a subgroup of discontinued operations. When you stop some operation, maybe you will have some assets held for sale in there. For example, when you decide to stop one division, then you have a discontinued operation and you need to disclose it separately in the financial statements. Now, if you plan to sell machinery of this division, then you have assets held for sale. If you plan to sell the whole division, then you have a disposal group held for sale. Does it make any sense?

Or the opposite situation. You have a building that you plan to sell and it meets the definition of asset held for sale. But, it is not a discontinued operation in this case, because it is not a component of an entity – it’s just an asset.

The difference in reporting between assets (disposal groups) held for sale and discontinued operation is that:

– for assets held for sale, you need to apply special accounting policy as defined in IFRS 5 (see above), and

– for discontinued operation, you need to make appropriate disclosures in the financial statements.

2) As written in answer 1) – the segment will be both discontinued operation and disposal group held for sale, therefore you need to 1) apply special accounting treatment as for disposal group held for sale and 2) present and disclose discontinued operation separately in the financial statements.

Hope it’s clearer 🙂 S.

Thank you Silvia for your time writing this comprehensive answer. Things are clear now. Thanks again.

Thanks madam

Hi Silvia, I’m curious of something. If say in the above example, the segment is operated by 3 subsidiaries together. Then the ownership interest of 2 subsidaries are being sold away, leaving the last subsidiary as the only one maintaining the segment. So, the segment is not dissolved. Do you think IFRS 5 is applicable here? I’m unsure. Based on the above explanation, is it true that most likely there will be some assets held for sale issue, but it is not a discontinued operation?

Hi Sofia, you need to look at what’s the primary factor defining the segment in this case – is it the nature of operations? Or geographical location? Maybe if you are more specific, then we can look to this closer.

It is the nature of operations, since the segment is based on the type of business done. For example, this segment is in media business, so all 3 are media companies. The Group as an overall has other types of business. So the media business is only one among many other segments. After the sale of subsidiaries, the media segment of the Group remains, continued by that last subsidiary and its parent.

Hi Silvia,

I am battling to distinguish whether or not IFRS 5 applies or not. e.g. I have an unlisted publisher company, revenue is driven from 1. Books, 2.Online news platform and, 3. Magazines. Due to COVID – in July we announced the cancellation of all titles effective in October. The magazine division comprises a number of subdivisions. One relating to Health etc; We are hoping to find a suitable buyer for this sub-division once the economy has recovered. Please advise how I would go about classifying this?

I know that there are two separate components: 1. Disposal of the magazine and 2. the potential for IFRS 5. Please could you assist

Dear Silvia, where the investment property is carried at cost rather than at fair value and is to be disposed of in the next financial year ending 31/12/2017, should the investment property be reclassified as assets held for sale? If yes, should the associated borrowings be reclassified as well?

Dear Wilson, as soon as it meets all the above stated conditions for classifying as held for sale, then yes (e.g. there is a plan, asset is marketed etc.). And no, associated borrowings are not to be reclassified unless you sell them together with an asset. S.

But IAs 40 is an exception as you mentioned above?

Yes – but only if you use fair value model under IAS 40. If you use cost model under IAS 40, then it is not an exception.