New profit or loss statement under IFRS 18 and discontinued operations

Question:

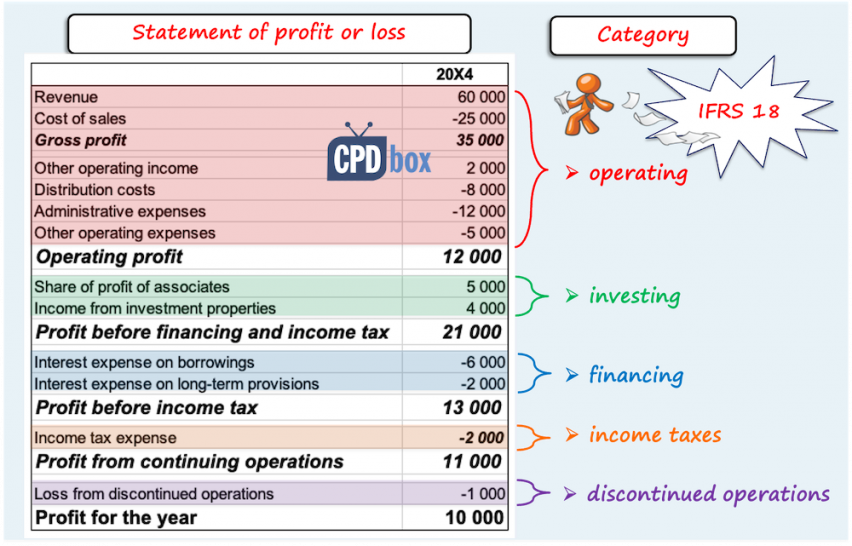

In the new profit or loss under IFRS 18, discontinued operations are shown AFTER the profit from the continuing operations and income tax expense.

Why is income tax not calculated on discontinued operations?

Answer

Yes, it might look a little bit confusing, because under the new format of profit or loss in accordance with IFRS 18 Presentation and Disclosure in Financial Statements, profit or loss from discontinued operations is shown after income tax expense.

After all, “income tax expense” and “profit/loss from discontinued operations” are two mandatory categories of income and expenses in line with IFRS 18.

However, in line with IFRS 5.33, we should always present the profit or loss from discontinued operations POST-TAX, so yes, that single line already contains the tax component.

And, the income tax line then contains just the income tax related to continuing operations.

Further reading

- Summary of IFRS 18 Presentation and Disclosure in Financial Statements

- Top 4 changes in profit or loss under IFRS 18 – step-by-step video tutorial..

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

Leave a Reply