Should we apply ECL model under IFRS 9 if we have only trade receivables?

Question:

We do not have any financial assets, except for trade receivables. Do we have to apply Expected Credit Loss rules under IFRS 9?

Answer

Yes, of course, because the trade receivables are in fact financial assets at amortized cost under IFRS 9.

However, it is NOT that difficult, with the right data.

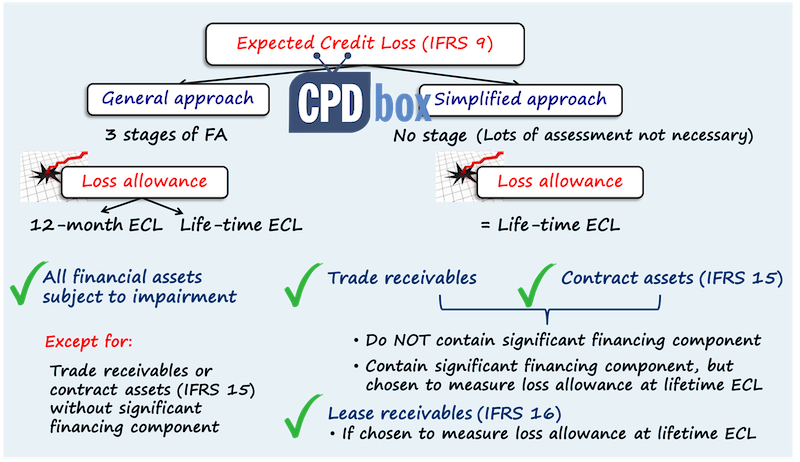

You do NOT have to apply general model and determine the stages depending on the receivable’s performance and credit risk.

The reason is that IFRS 9 offers some exceptions:

- “Short-term” trade receivables (WITHOUT significant financing component): apply simplified approach – the ECL allowance is measured as lifetime ECL, and you can simply derive the percentages of credit losses and create a provision matrix;

- “Long-term” trade receivables (i.e. WITH significant financing component): you have a choice here: either apply general model and determine your stages, or just use simplified approach as with your short-term receivables.

Further reading

Here are more detailed articles about ECL under IFRS 9:

- How new impairment rules in IFRS 9 can affect you

- Measurement of ECL: probability of default vs loss rate approach – learn about two most common methods applied when measuring ECL, their pros and cons and illustrative examples

- How to measure probability of default – this article describes a few methods of measuring probability of default (PD) and contains my personal recommendation for external help if you need (discounts for CPDbox subscribers and readers)

- How to calculate bad debt provision under IFRS 9 – here, you will find step-by-step process of determining the default rates and calculating the provision under IFRS 9

- Example: ECL model on interest-free on-demand loan

Also, we would like to draw your attention to our course ECL for Accountants focusing on trade receivables – this course will give you the strong knowledge and practical tools to calculate your ECL provision on trade receivables.

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

Leave a Reply