How to Implement IFRS 16 Leases

The new lease standard IFRS 16 is exactly one of these earthshaking things that can make your head spin around.

Well, especially if your company uses the operating lease as an effective tool of getting your assets quickly with relatively low risk.

I wrote a few articles in the past for you:

- Summary of IFRS 16 Leases – contains the nice video

- Troubles with IFRS 16 Leases – I discussed the main difficulties when applying this standard

- IFRS 16 vs. IAS 17: How the lease accounting changed – you can find an easy numerical illustration of the whole trouble there.

Plus, I added the full course about the IFRS 16 Leases and its application into the IFRS Kit, so if you are dealing with that right now, I highly recommend checking out!

However, I keep getting the questions about how to implement IFRS 16.

What to do first and what to do next.

And, additional questions like: “Do I really need to go study my old 4 000 contracts and reassess them under the new rules? Oh holy s..t!!!”

As usual, I’d love to help a bit and give a helping hand.

In this article, you will learn:

- 3D strategy to implement IFRS 16

- What accounting policies do you have and what accounting policies are the best for you to select

- Do you really need to reassess everything???

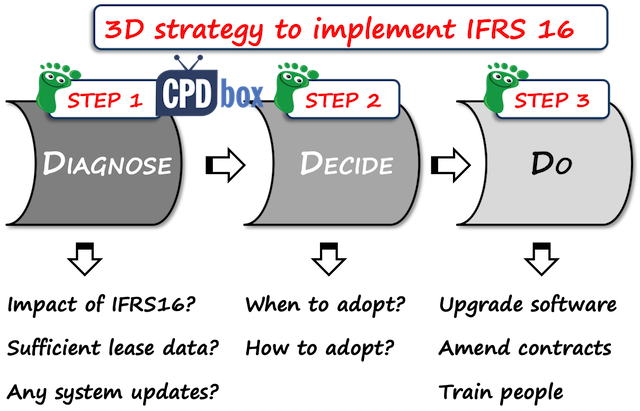

3D strategy to implement IFRS 16

No worries, I’m not going to show you any special visual 3D effects here – I leave that to Mr. Spielberg or other Hollywood masters.

Each D stands for some step to take in order to adopt IFRS 16 and stay healthy, sane and cool at the same time.

Maybe you have already started with this process, but if not, let me quickly sum up:

D1: Diagnose

In the first stage, you should focus on assessing your own business and impact of IFRS 16 on it.

What should you be diagnosing?

Here’s the short list:

- Is your company heavily exposed to the changes in lease accounting or not? How big is the impact?

- Do you have the sufficient database of your leases containing all the information necessary for the new disclosures?

- Will the change require any technology or system updates?

- Will the change trigger the change in the business development or purchasing? Contracting?

D2: Decide

After you analyze and diagnose, you should focus on the important decisions.

I would say that two of them are especially important:

- When are you going to implement IFRS 16?

You have to apply IFRS 16 mandatorily for all periods starting on or after 1 January 2019.

However, there’s another big change – the new revenue standard IFRS 15 Revenue from Contracts with Customers that needs to be adopted earlier, from 1 January 2018.

For me, it’s always better to do all the changes at once, in order to make just one system or technology upgrade, just one restatement in the financial statements and just one big work.

Therefore, would you rather implement IFRS 16 one year earlier, from 1 January 2018?

- Which accounting policies are you going to select?

There are more transitional options in IFRS 16. You can select more accounting policies to adopt IFRS 16.

Which one is the best for your business? I write more below, just keep on reading.

D3: Do

At this stage, you need to work hard, spend a lot of money and simply go ahead.

If you did your homework in the first 2 stages well, then you have an easier job.

So, upgrade your software, amend your contracts and train your people to work under the new system.

Don’t forget to involve people from across your company, not only accountants, because omitting the purchasers, lawyers or other relevant areas could result in inefficiencies and you paying a price.

OK, that was a very rough outline of what you should do and if you haven’t started yet by now, I would say it’s time.

Do we have to reassess all existing lease contracts?

The standard IFRS 16 introduced the new lease definition and as a result, some contracts might contain the lease under IFRS 16, but not under IAS 17 or IFRIC 4.

What does it practically mean?

Well, if you want to apply the new lease standard to all contracts, then you should go through all of them and seek whether they contain the lease as defined under IFRS 16.

A lot of work!

Luckily, IFRS 16 brings so-called practical expedient. It is a relief that permits:

- To apply IFRS 16 to the same contracts as to which IAS 17 and IFRIC 4 were applied, and

- Not to apply IFRS 16 to the contracts to which IAS 17 or IFRIC 4 were not applied.

Simply speaking, you don’t have to reassess the contracts and seek whether they contain the lease.

You can just take all lease contracts that you currently treat as the lease contracts under IAS 17 Leases and apply the new rules to them.

But, of course, you have to assess the new contracts entered into after the date of initial application. The exception applies only to the older contracts.

In my opinion, most companies will apply this expedient and simply account for the change on “old lease contracts” without seeking the lease in other contracts.

However, I can imagine the situation in which you had an operating lease contract, but not a lease under IFRS 16.

In this case, I would probably forget about expedient and reassess the lease, because I would definitely prefer keep that contract off balance sheet rather than accounting for the right-of-use asset.

Also, you should keep in mind that you can’t apply the expedient only to some selected contracts. Either you apply it fully to all contracts, or not at all.

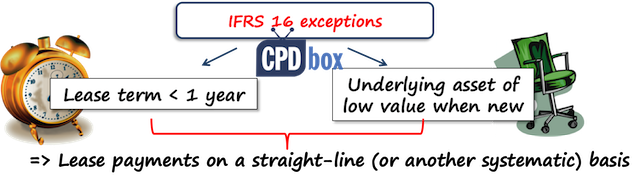

Do we have to bring all the operating leases to the balance sheet?

No.

If you the lease term is maximum 12 months, or the leased asset has the low value (like furniture or computer), then you can account for an operating lease payments straight in profit or loss.

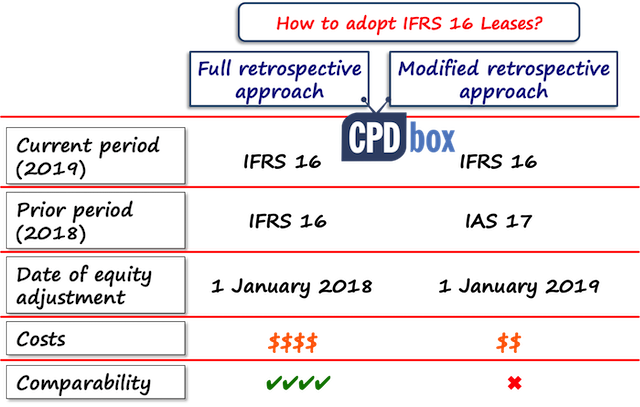

How to account for IFRS 16 adoption?

In other words – how to make transition in your financial statements?

The standard IFRS 16 offers 2 methods of a transition:

- The full retrospective approach

Under the full approach, you need to apply IFRS 16 retrospectively in line with IAS 8.

It means that you need to restate all prior financial information and recognize an adjustment in equity as of the beginning of the earliest period presented.

Therefore, if you adopt IFRS 16 for the period beginning on 1 January 2019, you need to book the adjustment in equity on 1 January 2018.

Also, all your comparative information for the year 2018 will be presented under IFRS 16.

This method is more demanding, because in fact, you need to present the data for the year 2018 under both new and old rules:

- In the financial statements for the year ended 31 December 2018, you present your leases under IAS 17;

- In the financial statements for the year ended 31 December 2019, you present your leases under IFRS 16, including the comparative information – year 2018.

Lots of work!

Special For You! Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!

I guess that exactly because of the terrible amount of work connected with this approach, many companies will select the second one – modified retrospective approach.However, the full retrospective approach has its big advantage – although there’s a lot of work, you are presenting the fully comparative data, because both the years 2019 and 2018 are prepared under the same rules (in the financial statements for the year 2019).

- The modified retrospective approach

Here, you need to apply IFRS 16 from the beginning of the current reporting period.

It means that you do NOT need to restate the financial information for the prior comparative year.

You simply leave the prior year under older rules of IAS 17.

The adjustment to bring your leases under the new rules of IFRS 16 is recognized in equity as of the beginning of the current reporting period (not the earliest presented as under the full approach).

Also, you don’t need to present some disclosures as under the full approach.

Overall, this is a very cost effective, although not very comparable methodology and I bet it will be the most popular among all companies restating their leases.

The comparison of both approaches is here:

Now, please leave me a comment below this article about your biggest challenges when adopting IFRS 16.

Also, I was thinking about posting a numerical example to illustrate how to implement IFRS 16 under the full approach and under the modified approach – but, it’s a lot of work, so if you are interested, just leave a comment “Yes, publish an example!”

Thanks 🙂

Update after a few days

HI GUYS,

OK, understood! 🙂

You want an example!

My next article will be all about the example. I’ll try to make a video, but currently I’m spending the holiday season with my 3 kids and the things are getting too busy…. but I’ll try!

Thanks for all your comments!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

57 Comments

Leave a Reply

Thank you Silvia for your explanation,

I was wondering about the accounting treatment of the lessee, why the lessee has the choice to present the lease and non-lease components as separate or combined in one amount? in this case the lessee capitalize the service and maintenance costs to the cost of the asset and charge depreciation in the profit or loss statement instead of recognizing these costs as service costs in separate line.

This is noted, thank you. At reporting date, i will therefore have nil ROU and lease liability. thank you

Hi Silvia

Please assist, i have a scenario where at reporting date (e.g 31 Dec 20) we have terminated a contract with one lessor but moving into a new building under new contract on 1 Jan 21. As we transit from one contract to the other, where we have already paid deposit and rental for the ensuing month: Do we recognize right of use and lease liability at reporting date? If yes, do we use old contract, or we use the new contract?

Hi Matida,

1. Do not mix the old contract with the new contract, please – it seems they are not related.

2. Actually, the accounting for the lease liability and ROU asset under the new contract starts at the commencement date; that is when the asset was made available by the lessor to the lessee. So if the lessor made that asset available to you when you paid, then yes, book lease liability and ROU asset. If not, then just book some prepayment made and start booking lease liability and ROU asset when the new lessor makes new offices available to you.

Hi Silivia. Firstly, thanks for all your IFRS articles which have been very helpful to me and many others.

I am little confused in regards to the full retrospective approach though for ifrs 16.

You said in regards to the full retrospective method:

“Also, all your comparative information for the year 2018 will be presented under IFRS 16.”

But after that you said:

“This method is more demanding, because in fact, you need to present the data for the year 2018 under both new and old rules:

In the financial statements for the year ended 31 December 2018, you present your leases under IAS 17;

In the financial statements for the year ended 31 December 2019, you present your leases under IFRS 16, including the comparative information – year 2018.

Lots of work!”

Initially, you said that IFRS 16 should be applied for the year 2018 and then you said you should present 2018 figures under IAS 17. Am I missing something here?

Yes.

What you are missing is that this sentence “Also, all your comparative information for the year 2018 will be presented under IFRS 16.” relates to the financial statements for the year 2019; and those 2 sentences below related to financial statements of two different periods:

– 1 financial statements for the year 2018 (where you present 2018 as current period and 2017 as comparative period – here, you present the year 2018 under IAS 17 as you have not applied IFRS 16 yet); AND

– 1 financial statements for the year 2019 (2019 = current period and 2018 = comparative period).

I hope it is clearer now. S.

Hi, Thank you for helping us. Please could you share your thoughts re 445 calendar (mostly used for retail businesses) i.e. how to split lease payments, ROU, liabilities, interest and depreciation?

When liability will be reduced? based on actual payment date (which could affect 2 different months in some cases) or based on virtual split of monthly costs into days/weeks? Thank you in advance

Dear Silvia,

I have one question about short-term leases. Do I understand correctly that IFRS 16 permits a company to elect not to recognise assets and liabilities also for leases ending within 12 months of the date of first applying IFRS 16? Please let me know your opinion.

Yes, correct.

Dear Sylvia,

Very useful guidance. I will always come back! ?

Easy and straight forward.

Thanks

Thank you 🙂

Dear Silvia,

This article removed my headache! 🙂 your article showed our concerns about the implementation and also I got the vision of this IFRS16.

Thank you!

You are a great support for us who are using IFRS!

Adrian.

Hi Silvia,

If there is a lease contract that started in 2001 for example and ends in 2021. If we early adopt from 1 Jan 18 using the modified retrospective approach – would the opening balance adjustment take into account the financial impact of the lease from inception of the contract or only from 1 Jan 2017? I know that this is a forward looking view as we calc the NPV but if the NPV was calculated from inception with the payments allocated to it then this does affect the cash flow and interest and depreciation. Under the fully retrospective approach also – would we calculate the impact of the contract as if we always applied IFRS 16 (from 2001)? Thank you

Hi Silvia,

Does the forecasted cost of a make good provision requiring the tennant to return the office to its former state also get included in the right of use amount ?

That depends on how this provision is written in the contract, but in general no.

Hi Silvia.

Our company rented the premises for 3 years and repaired it according to our needs.

Under IAS 17 we accounts for lease payments as operating lease (debit P&L).

Initial cost of repair was accumulated and recognized as assets (IAS 16) and was depreciated during lease duration – 3 years.

IFRS 16 does not consist any point about repair cost of rented premises after start of leasing. Not before the date of agreement, but after start. We have rented and then started costly repair.

What about new IFRS 16 if such case will be with new rented premises? Should we account for repair cost as expenses (current year P&L) or capitalised it as non current assets (IAS 16 as previously) or capitalised as right of use (IFRS 16).

Thank you.

Dear Olena, you will still capitalize leasehold improvements as PPE and depreciated it over the useful life or the lease term, whatever is shorter. However, you need to recognize the right-of-use asset with respect to lease payments. S.

I am really do appreciate your efforts, I am really enjoyed to read and understand the standard easily .

God bless you 🙂

wish you the best

Thank you, Emadeldin 🙂

Hi Silvia,

It is mentioned on your website, if some one subscribe then you will email IFRS Mini-course 1 day book. But I did not get that.

Could you please check?

Kind Regards

Steave

Hi Steave,

this is a misunderstanding. We do not promise an e-book IFRS In 1 Day. We promise a mini-course – that is a few lessons from the IFRS In 1 Day and you will receive these lessons later, 1 email every few days. Instantly after subscribing, you will get the report Top 7 IFRS Mistakes. In case you are not receiving our e-mails, we kindly ask you to check your spam folder. Thank you! Kind regards, S.

Let me restate…

Hello Silvia.

In the section above “Do we have to reassess all existing lease contracts?” you state (paraphrased) that:

a) one may choose not to reassess old contracts for the presence of a lease under the practical expedient principle

b) I can imagine the situation in which you had an operating lease contract, but not a lease under IFRS 16.

If I choose to follow the expedient principle, does this mean I can still eliminate my operating lease in b) above?

I believe this is what you are stating but want to be clear.

Thank you!

Your comment is awaiting moderation.

yes, pls publish an example

It’s been already published 🙂

Yes, publish an example

Great article! pls publish an example

Thank. U so much. I enjoyed all ur write-ups. Could u pls take up IFRS 25 for me

Hi Ibrahim, what is IFRS 25, please?

Thanks a lot Silvia your so much blessed thanks a lot for sharing what you have with others.

Yes, publish the examples.

God bless you for the great work really.

Yes, publish an example! hhhhhh

“Yes, publish an example!”

“Yes, publish an example!”

“Yes, publish an example!”

“Yes, publish an example!”

Hi Sylvia,

If you are half way through a lease at 01 Jan 2019 – say 3 years into a 6 year lease – do you account for the lease on 01 Jan 2019 (assuming modified retrospective approach) as if it is a new lease with three years to go or as if it is half way through a lease and create the lease creditor/asset etc?

Thanks

Hi Andy,

you account for it as if it would have always been accounted for under IFRS 16 – i.e. you recognize the new asset, half depreciated. However, as you apply the modified approach, then you do this adjustment at 1 January 2019, not 1 January 2018. S.

Yes, Publish example

Thank you Silvia. Reading IFRS this way is great.

Hi Silvia

Just 5 minutes reading, lot to share with clients and yes once again, clear and to the point.

Great work

Jerad

Hi Silvia,

Kindly publish a numerical example for the two approach.

Kind regards

Hi ! Sylivia.Great work indeed . Will always appreciate the most if numerical example can demonstrate extract of the application of Ifrs 16.

Be blessed for the heart and great work you share with us on standards !

Silvia, as usuaĺ, thanks a zillion for this article.

Yes,please publish numerical example!

Thanks!

Hi Silvia,thank you for the good work IFRS it is easy to follow expecially with those animated graphics.

Do you have a special IFRS KIT without videos but only excel spreadsheet and graphics?

Hi sunday, thank you! No, the IFRS Kit is all about the videos and excels and graphics are just supporting tools. Silvia

Yes, publish the numerical Example

Thank you!

Yes, publish an example please.

Thank you for the Good IFRS publication and easy to understand. Kindly publish the numerical examples.

Yes would be good to see an example

tnx

Kindly publish the numerical examples to apprehend issues better bette

Very informative article with practical approach.

Kindly update two mistakes as follows;

if you adopt IFRS 6 for the period beginning on 1 January 2019

you present your leases under IFRS 19

Thank you, great catch, corrected! 🙂

“Yes, publish an example!”

Quite expository and educative. Please do well to present numerical examples. Thank you.

Hi Silva,

Thank you for this great post.

I want to believe that a numerical example will greatly help in understanding the impact of the adjustments as well as need for retrospective application of the change.

Regards

Please publish the numeric example.