IFRS for Banks and Financial Institutions

If you work for a bank or any other financial institution, then you are very well aware of the fact that IFRS is a little bit different there.

OK, not quite like that: IFRS is still the same, just the way how you use it is a bit different.

Why is it so?

Unlike product-based and other service-based companies, banks work basically with money itself.

For other types of companies, money is mostly only the mediator of their transactions and most goods or services do not revolve around money.

In other words, money transactions – like having a bank account – are “supporting” transactions to the main business line.

But the main product or service of any bank or a financial institution (let me just call them “banks”) is money in various forms:

- Lending money,

- Saving money,

- Multiplying your money (or sometimes shrinking your money, too!),

- Taking care of your money,

- Enabling you using your money (credit cards, cheques, etc.), just name it.

As a result, the financial reporting of banks’ activities looks pretty different from what you would expect based on “normal” company.

In this article, I would like to outline the main specifics of the IFRS use by banks and the IFRS standards that are top priority for any CFO, accountant or a finance person working in banks and financial institutions.

We will look at 3 hottest IFRS topics for the banks and financial institutions.

#1 Financial Instruments (IFRS 9, IAS 32)

If you are working in a bank, then the standards about financial instruments are absolutely a MUST for you.

Of course – money is a financial instrument itself!

Financial instruments are very complex and involve lots of considerations and topics. Not only banks face financial instruments – any trading company has some financial instruments, too (if selling and invoicing).

The truth is that banks enter into many complicated transactions, issue various types of compound financial instruments (in which both equity and liability element is present, e.g. convertible bond), generate loans to different portfolios of clients with different credit risk and many others.

Within the financial instruments, the hottest issues are as follows:

1.1 Impairment of financial assets

The impairment of financial assets as introduced by IFRS 9 in July 2014 brings many big challenges especially to banks.

In brief: IFRS 9 introduced expected credit loss model for recognizing loss allowance to financial assets. And banks are affected severely.

Why?

Majority of other types of companies can use simplified approach permitted by IFRS 9 for the impairment of financial assets and calculate loss allowances solely in the amount of life-time expected credit losses.

To make it clear, I have written an article with numerical example illustrating simplified approach here.

However, banks cannot use simplified approach for the biggest group of their financial assets – loans, because the loans do not fall within the exception.

Banks need to apply 3-stage general model for recognizing loss allowances.

It means that banks must:

- Decide whether the individual financial assets will be monitored collectively (lots of similar loans with lower volumes?) or individually (big loans?)

- Carefully analyze the financial assets and assess to what stage does the financial asset belong:

- Performing, or

- With significantly increased credit risk, or

- Credit impaired.

- Based on the stage, bank must evaluate how to calculate loss allowance equal to:

- 12-month expected credit loss, or

- Life-time expected credit loss

- For the above calculation, bank must collect big volume of data to estimate:

- Probability of default within 12 months;

- Probability of default beyond 12 months;

- Credit losses in the case of default

- Bank may need to categorize its loan into various portfolios and monitor relevant information for each portfolio separately, based on some common characteristics.

All these tasks bring significant tasks for IT department, account managers dealing with the clients, statistic people and many other involved in order to upgrade the internal systems, so that all the information is provided on time and in sufficient quality.

Not an easy task!

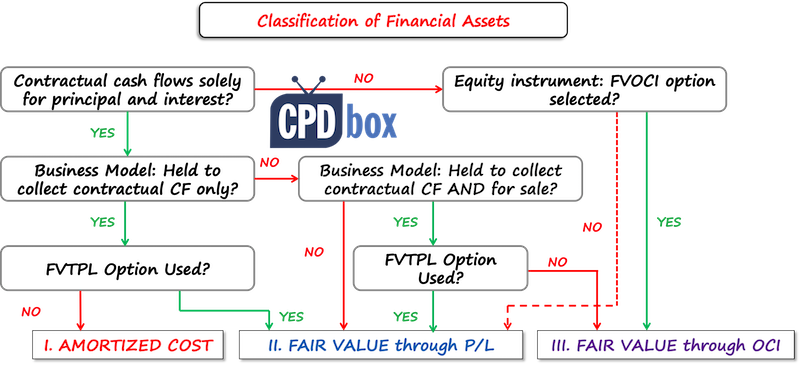

1.2 Classification and measurement of financial instruments

Financial assets make up most of banks’ assets.

Currently, standard IFRS 9 classifies the financial assets based on 2 tests:

- Contractual cash flows test, and

- Business model test.

Based on the assessment of these tests, the financial asset can be classified either as measured at:

- Amortized cost, or

- At fair value through profit or loss (FVTPL), or

- At fair value through other comprehensive income (FVOCI; and here, further accounting depends on the type of an asset).

The banks and other financial institutions, mainly companies trading securities, investment funds and similar entities, need to dedicate their time and effort in order to analyze their own business model for individual portfolios of financial assets (Trading? Collecting cash flows? Both?), and then decide on their classification and measurement.

Regardless analyzing the 2 tests above I’d like to stress here, that every single financial asset and liability needs to be initially recognized at its fair value (well, sometimes you add transaction cost).

Here, the standard IFRS 13 Fair Value Measurement comes to the light. This standard sets principles for determining the fair value and therefore, it becomes very important in the financial reporting of any bank.

1.3 Distinguishing liabilities from equity

Banks enter into various contracts and transactions related to money and financial instruments – we have already said that.

Thanks to complexity and diversity of banks’ operations it might be demanding to classify correctly whether the bank’s instrument is equity or liability, or even a mixture of both.

The standard IAS 32 Presentation of financial instruments gives us more precise rules on how to correctly distinguish between these two types of instruments and this becomes particularly hot in banks.

Why?

Because incorrect identification of equity/liability/mix can lead to wrong presentation of bank’s financial results including various rations assessing bank’s capital and financial situation.

#2 Presentation of financial statements (IAS 1, IAS 7, IFRS 7)

Banks present their financial position and financial performance in totally different way than other companies.

Let’s break it down.

2.1 Statement of financial position in a bank (IAS 1)

The standard IAS 1 Presentation of Financial Statements does not prescribe the format of the statement of financial position – however, it brings some examples of accepted formats.

As soon as you include items mandatorily required by IAS 1, you are OK with your selected format.

When you look at the statement of financial position of any bank, you will not see the balance sheet that you are used to in other types of companies, starting with non-current assets (property, plant and equipment, intangibles), followed by current assets (inventories, receivables, cash), and then the second part starting with equity, non-current liabilities finishing with current liabilities.

What you would see instead is the statement in which individual items are ordered by their liquidity, starting from the most liquid assets, finishing with the least liquid ones. The equity & liabilities part corresponds with the assets – it starts with the current liabilities in a descending order of liquidity and finishing with equity.

Why is it so?

I have said it several times by now: money is the key. When you look to bank’s financial statements, you want to see how much money and liquid asset it owns rather than how many buildings and computers there are.

In other words – liquidity order is much more relevant for banks.

2.2 Statement of profit or loss and other comprehensive income in a bank (IAS 1)

Similarly as with the statement of financial position, IAS 1 does not prescribe the exact format of the statement of total comprehensive income.

It is up to entity’s choice to present its results in a format fitting the best the entity’s business.

No surprise that banks’ statements of profit or loss and other comprehensive income usually start with interest income and interest expenses!

Normally, you would expect to see the interest reported somewhere close to the end of the statement, in the financial operations, and often netted off.

However, interest income and expenses are the most important caption for the bank as that’s what banks usually do – they deposit your money and give you the interest (=their interest expense) and they lend you money + charge you the interest (=their interest revenue).

As the banks usually charge you some fees for your bank account, fee and commission income follows (just a side note – as the interest rates are quite low right now and fees are climbing the roof, I just wonder when the fee and commission income goes in the top line before interest).

We can continue, but the main principle here is to present the most important revenue – generating activities at the top.

For your illustration, here’s the comparison of 2 statements of profit or loss and other comprehensive income -1 for a product-based company and 1 for a bank:

2.3 Statement of cash flows

I am going to repeat myself a bit. Money rules in the banks and therefore, cash flow statements look different.

When you prepare the statement of cash flows, you normally classify individual cash flows into 3 parts:

- Operating part,

- Investing part, and

- Financing part.

Although IAS 7 Statement of Cash Flows gives you examples of items reported under each heading, this basically does not apply for banks.

The reason is that the bank’s principal revenue and cash flow generating activities are totally different from other companies.

Therefore, while you normally see interest paid in financing part and acquisition of securities in investing part, for banks all these activities are reported in operating part. We can continue like that with the other items too: including profit from trading activities, etc.

2.4 Disclosures

On top of disclosures presented by other non-financial companies, banks must present a number of other disclosures related to their activities.

The most important disclosures are:

- Capital disclosures under IAS 1:

Here, the bank presents how it manages capital, with focus on:- Descriptive information about capital management strategies,

- Some numerical data about capital managed,

- Whether there are some externally imposed capital requirements for the bank (and you bet there are!) and

- Whether the bank complied and if not, what are consequences.

- Whole range of disclosures in line with IFRS 7 Financial Instruments: Disclosures.

These disclosures relate mainly to financial instruments which is what the bank is about anyway. The focus is on:- Significance of financial instruments, including the breakdowns by categories, fair values and how they were set, accounting policies for financial instruments,

- Risks attached to financial instruments and their nature and extent, including credit risk, market risk and liquidity risk;

- Transfers of financial assets;

And other.

#3 Consolidation and special purpose entities IFRS 10, IFRS 12)

Banks love to use special purpose entities.

Before some time, it was a “great and creative” way of hiding some undesirable or toxic assets from the eyes of public, as the special purpose entities were usually not included in the consolidation (understand: no one saw them).

However, after a few accounting scandals (for example, Enron), there were new and strong rules adopted. In IFRS, we have the standards IFRS 10 Consolidated Financial Statements and IFRS 12 Disclosure of Interests in Other Entities, that require inclusion of structured entities in the consolidation when they meet the conditions (basically, when banks has control over SPE).

Even today, many banks use literally hundreds of SPEs for various purposes, mostly for securitization of their loan receivables, holding some tax-efficient leases, for asset-backed financing, etc.

Example of securitization scheme:

The bank needs to evaluate very carefully whether they control structured entity using the same methodology as for any other entities controlled by voting rights.

As a result, you can see lots of entities including in the bank’s consolidated financial statements.

Other issues to watch out

Other critical areas for banks and financial institutions to watch out are mostly the same as for any other company, but they might be more significant and material:

- Leases – some arrangements are not called “lease”, but their substance is often a finance lease. As a result, some contracts might be shifted from off-balance sheet into the balance sheet.

- Employee benefits – banks often provide a range of employee benefits, such as:

- “Employee loans” at the reduced beneficial interest rate;

- Free bank accounts or other bank’s services to employees,

- Contributions to pension funds

- Health-care schemes for both current and retired employees and many other.

As a result, the standard IAS 19 Employee Benefits with all its specifics, curls and curves comes to the daylight.

- Hedge accounting – banks undertake hedges quite often, but they do need to realize that in order to apply hedge accounting, all the conditions including hedge documentation, must be met.

I know this list is not exhaustive, but I hope that I gave you at least some hints and intro into the complex topic of IFRS accounting in banks.

If you liked this article, please share it with your friends and if you have experienced other specific situation in a bank or a financial institution you work for, please share it with me and other readers below in the comments. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

55 Comments

Leave a Reply

many banks have a separate fund for their benefit plans (e.g. Gratuity in India) – these are through a separate SPV like a “Trust”. However, the Trust or Fund managers may sometimes deploy / invest those funds back into the same bank as a deposit (liek any other customer). In such situations, does those moneys qualify as a “plan asset” is a moot point.

Hearty thanks for these important articles you always share with us but for today’s article i would like to ask if you can show us how we can calculate profitability ratios for bank’s financial reports because it seems a bit different with what we normally apply to other companies.

Best wishes

Thanks, very simplified description.

Very attractive and practical presentation.

Thank you

Very helpful !!

Hi Silvia, You are truly genius. Your articles provide great thoughts to understand complex IFRS standards. I would like to attend your live session. Do you also provide live seminar in India.

Thank you, Silvia.

Thank you for your work!

Hi Silvia thank you so much. I am working in Financial institute and i want to know amortization rate with effective interest and we are lending a loan with interest rate and collect some other charges and % of saving as a loan collateral. how can we calculate effective interest rate

Dear Yerom,

If I may take liberty to answer your question. Please arrive at IRR for each loan product based their individual cash flow after considering loan disbursement, interest and principal repayment schedule and fees and other charges collected as processing and penalty fees, etc. Treat IRR as your EIR for the purpose of revenue recognition and measure loan at amortised cost in SOFP. I hope this explanation will meet your quest.

Thank you, Silvia.

Dear Silvia, thank you for your interesting and very helpful articles. I have one question on the method of presentation of the Statement of Financial Position.

A mortgage fund had been presenting its Statement of Financial Position based on liquidity until 2017. For 2018 the management decided to present its current and non-current assets and liabilities as separate classifications in its SFP (like all other types of companies). What should be the approach of auditors to this decision? Shall the they insist on liquidity based presentation which provides information more reliably and more relevantly for financial institutions or accept the change without any note in opinion?

Hi Gunel,

I believe the auditors should form their own opinion on the fact whether the new presentation is more relevant and reliable – because, it is very judgmental. As a matter of fact, IFRS do not prohibit changing the way of presenting. S.

Dear Silvia;

I have a very basic question. That is ,

Is it cash is a Financial Instrument?

Yes, a kind of.

Hi Silvia thanks so much for the article really helpful especially for me as i work in a bank.

Thumbs up.

Hi Silvia thank you so much. if an entity give a loan with decling rate is that mean the entity is using amortized cost with effetive intererest rate

Hi Gemechu,

If I may answer your querry, the answer is no. In order to measure loan, a financial instrument at amortised cost, it has to pass business model test and contractual cash flow test i.e. the company should be having lending as its business objective and in the normal course of business its intention is to collect the principal and interest on the loan till its maturity. If it meets the above criteria then it has to measure the loan (disbursed at depleted interest rate) at its amortised cost by applying IRR as Effective Interest Rate and Interest Revenue shall be recognised at EIR. Thanks

hello thank you so much please sent standarad book ifrs statament fianancial for banks

Thanks Silvia it is really helpfull for us in Ethiopia

Good day Silvia

I really like your articles and they help me out 9 out of ten times. Wondering if you could help me out with this one too. I looked up in the relevant IFRS/IAS but there aint any specific guidance on this. The issue is as follows:

Bank Alpha advances a loan to a counterparty, as security it receives a counter-guarantee from its holding company (sounds weird as to why is the Bank’s holding company providing a counter-guarantee but let ignore this and stick to the accounting issue). The counterparty has been in default and the bank has classified the loan as impaired. For purpose of the impairment assessment and provisioning, the bank anticipates a minimum loss as they have a counter-guarantee.

For accounting purposes, can the counter-guarantee be netted off against the loss (provision for impairment) or should these two (loss and recognition of an income/asset) be accounted seperately ie. the loss recognised in the profit and loss and other-income (sort of reimbursement) credited to the profit and loss. Thanks for your helping out and for quoting the relevant paragraphs of the applicable IFRS/IAS.

Thanks again

Dear Kam,

I think it’s highly unlikely you can net off, because when 3 parties are involved, it’s hard to say that the conditions for the net presentation would be met. But you need to assess yourself, based on your legislation, intention to net off simultaneously etc. I would point you to IAS 32 paragraphs 42-50. S.

Dear Silvia;

I have been going through your articles in IFRS. As a matter of fact in my country, Ethiopia it is a new phenomena in financial reporting and the government has already instructed all commercial Banks to adopt this system, IFRS. And i am one of the committee members who has given the assignment to transform the prevailing financial reporting system to the IFRS. Thus, i am glad to get your articles on IFRS Box and i believe i will get a lot from this in transforming my Bank to the newly devised reporting system.

Really i got so much from your presentation and I Thank you very much for what you have shared!

Dear Kibrom,

thank you very much for your kind words. I think Ethiopia has a tough challenge to do, but many countries adopted IFRS successfully. I wish you good luck and of course, browse my web and use as needed 🙂 S.

Ya you are right Dear Silvia;

In our context the implementation seems too tough for there is no relevant educational background and qualification of performers in place. As a result we are planning to transform the new reporting platform but unable to know where to start and then where to go. Its simply confusing…………!

Great article Silvia!!!! Was very useful 🙂

Thank you very much! i’m doing financial statement analysis project for two banks, so i think that will help a lot specially that both banks uses IFRS. so, thank you again :D.

A very insightful article! Thank you Silvia! 😀

I WOULD TO KNOW IMPACT ON BANK INDUSTRIES, SO PLEASE SEND ME THE IMPACT ON MY E MAIL

which IFRS standard governs the process of Revenue recognition for Banks or financial instruments. I want to read about it so from where to start. I know for example IAS18 or IFRS 15 is revenue recognition standards for Revenue recognition but for banks/financial institutions/financial instruments, is there any particular standard?

Hi, Silvia

Despite of been a new here, I really liked your articles.

Please keep going on.

Thanks.

Dear Sylivia,

Thank you for sharing with us this interesting topic. Kindly help to understand well the treatment of loan originating fees(Can we recognise it at once or be deferred as per loan maturity).

Hi Ziade,

loan origination fees shall be treated as a part of cash flows and adjust the amortized cost, so neither one-time recognition nor deferral. S.

Great insights!

It would be awesome if you could add a comprehensive course of finantial instruments & hedge accounting to your IFRS courses.

Hi Alvaro, thank you! By the way, this comprehensive course on financial instruments and hedge accounting has already been in the IFRS Kit for some time, just check it out 😉

Its a fantastic article, well arranged and explained

I am unable to find IAS 33 Eran9ng Per Share notes……. Anyone can help??

Hi Behzad,

I haven’t published them yet, but I’m planning to do so in the near future! S.

great silvia ,there are so many accountants doing only product based company financials having no idea how it will be presented for bank ,thank you very much.

Silvia….I really appreciate you insightful and yet compendium article. Keep it up!

Thank you Silvia for sharing God bless..I am an Accounting stuedent from South Africa

Excellent presentation. To the point. Thank you very much.

Thanks very much Silvia reylay

i attempted to reach the same level or even close to you, but every time I read the subject of IFRS I feel I am still a student or less and you’re a professor of genius

So I decided to participate in ypur live seminars shortly after rearranging some related private matters

(( my time and money ))

Dear Khalil, thank you for your kind words!

I don’t feel like a genius, not even close – but it will be my pleasure to welcome you! However, my last live seminar is in Kuala Lumpur in April – http://www.cpdbox.com/live-ifrs-update-2015/

Kind regards, S.

This article is very informative and important for a revision on the subject matter. Thanks very much Silvia.

your Presentation is highly Educative, informative. Thanks for sharing your knowledge Silvia

This is great and insightful

A presentation in its simplest form for easy understanding. thank you very much.

Most creative method of learning I have ever seen. Thank you very much Silvia

Your explanation is very precise and to the point.

I would like to attend one of your live seminars and presentation.

Nice presentation for understanding the whole matter so easily and i am waiting for your valuable upcoming lesson. Hopefully that would be so much attractive as like present one.

Your presentation is simple and straightforward. Certainly, it brings out the salient issues subtly for easy understanding. I hope one day, I will have an opportunity to attend a seminar where you are a resource person.

Thumbs up Silvia for yet another insightful article.

your presentation is very attractive in that it is concise, to the point and very practical. Hence I am very happy to receive your articles always.

Good practical presentation