Sometimes, the things can happen behind your back – without you even noticing.

And, these things can affect you somehow.

Let me tell you a short story.

I participated in an audit of a big insurance company and our senior asked me to look at its investments.

Not surprisingly, this insurance company held lots of shares and in some companies it exercised either control or significant influence.

I was just going through the papers and suddenly, one thing came to my attention: the investment in a medium-sized manufacturing company (let’s call it ABC).

I remembered that a few months ago, significant foreign investor acquired controlling stake in ABC. I read it in the newspapers.

The acquisition was in fact performed in 2 separate transactions:

- The investor acquired about 40% of shares by purchasing the shares from other 2 investors, and

- ABC issued additional capital to the foreign investor.

Hmmm, what does that mean?

Well, the first transaction – purchasing shares from other investors – had no impact on our client, because the other shares just changed the owner.

The problem was with the second transaction.

Why?

The reason is that ABC issued new shares and it diluted the share of my client, the insurance company.

Simply speaking – imagine you hold 20 000 shares of 1 CU each in a company with total share capital of 100 000. Thus, you have 20%.

You still have your 20 000, but as a result of issuing the new shares, you share drops to 16,67% (20 000/120 000).

This is exactly what happened. Although our client did literally nothing wrong (or nothing at all), they lost their share.

The first thing I went to examine – was the significant influence maintained?

I stress it all over my articles about the group accounts. The percentage of ownership is just indicator of significant influence (or control, you name it). You have to examine other factors – read more here.

What’s worse – as a result of this transaction, our client lost significant influence in ABC. And, it had a huge impact on the accounting, because when you lose the significant influence, you have to stop equity method.

End of the story. These things happen quite often. It is called “deemed disposal”.

In this article, we will deal with deemed disposals of an associate, but the rules and accounting methods apply with any other deemed disposal, too.

What is deemed disposal?

Deemed disposal of an associate or a joint venture is simply reduction in interest or share in an associate or a joint venture other than by actual disposal by the transfer of shares or liquidation.

In other words – deemed disposals mostly happen “behind your back”.

How the deemed disposal may happen? Let me name just three very common ones:

- You (investor) ignore the rights issue by the associate or joint venture (or you do not acquire the new shares fully).

- An associate issues warrants or options to own shares and someone else exercise them (thus new capital is issued).

- An associate issues new shares to someone else (just as in my short story above).

Hmmm, after I wrote this article, my husband looked over my shoulder and said: That reminds me Facebook a few years ago…

Well, yes, that is a great example of deemed disposal, too.

The Facebook deemed disposal

What happened?

In 2004, Mark Zuckerberg founded Facebook together with Eduardo Saverin. Saverin was responsible for funding and business development and Zuckerberg was a content guy.

However, the things did not work well and Zuckerberg decided to cut off Saverin from Facebook.

How did he do it? No, he did not purchase the Saverin’s share…

Making long story short – the company owning Facebook issued new shares and distributed them to every other shareholder, except for Saverin.

This is the very best example of deemed disposal. It reduced Saverin’s share in Facebook from 30% to below 10%.

Of course, lots of lawsuits and nasty fights followed and maybe you have seen the movie “Social network” describing this situation.

If you’re interested in the full story, you can read it here.

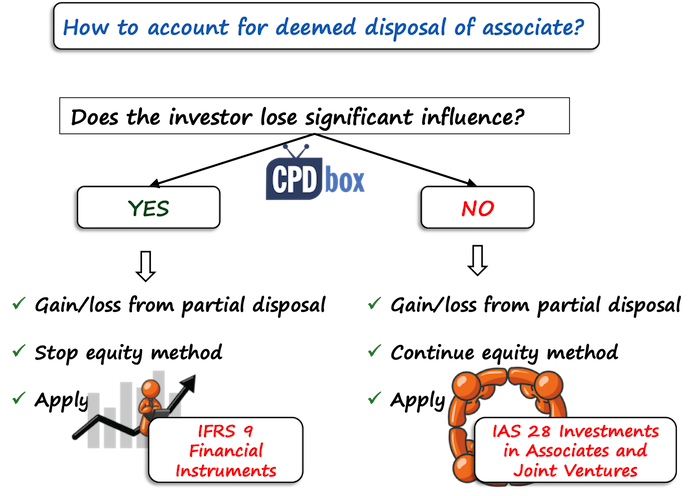

How to account for deemed disposal?

If you experience the deemed disposal of some share in your associate, then there are 2 different scenarios:

- You lose significant influence.In this case, you have to:

- Discontinue equity method and recognize gain or loss on deemed disposal;

- Recognize your remaining investment as a financial asset under IFRS 9

- You keep significant influence, just the percentage of ownership is lower.In this case, you have to:

- Recognize gain or loss on partial disposal;

- Continue equity method.

Let’s illustrate what happens in both scenarios.

Example: Deemed disposal of an associate

Question:

Angelo plc. held 25% share in Investee ltd. On 1 January 20X1, Investee issued 40 000 new shares of 1 CU each to Giovanni, plc. at par. You have the following information:

- Investee’s share capital before its increase was CU 150 000 (each share of 1 CU)

- Investee’s net asset on 31 December 20X0 were CU 200 000.

How should Angelo account for the deemed disposal of share, if:

- Significant influence is lost;

- Significant influence is maintained?

Solution

Before I outline the solution for both scenarios, let’s calculate a few very useful things (needed for both cases):

- Carrying amount of Angelo’s investment before deemed disposal = 25%*Investee’s net assets of CU 200 000 = CU 50 000

- Number of shares held by Angelo: 25%*150 000 = 37 500 (1 CU each)

- Angelo’s share after deemed disposal = 37 500/(150 000+40 000) = 37 500/190 000 = 19,7%

Now, let’s calculate the new carrying amount of Angelo’s investment in Investee:

- Carrying amount before disposal (see above): CU 50 000

- Less cost of deemed disposal = – CU 50 000 x (25%-19,7%)/25% = – 10 600

- Plus share on the new contribution = 19,7%*CU 40 000 = 7 880

New carrying amount after disposal = 47 280

Here, the loss on deemed disposal of CU 2 720 arose (difference between carrying amounts before and after disposal, that is CU 50 000 less CU 47 280).

Solution #1: Significant influence is lost

As I wrote about, you MUST discontinue the equity method if significant influence is lost.

Yes, maybe it’s unfair, especially if that happened without you even knowing, but that’s what you should do.

We have calculated all the necessary numbers above so let’s draft journal entries:

- Loss on disposal:

-

Profit or loss – loss on disposal of an associate: CU 2 720

-

Investment in associates: CU 2 720

-

- Discontinuing the equity method and recognizing a financial instrument:

-

Debit Other financial investments – CU 47 280

-

Credit Investments in associates – CU 47 280

-

Angelo needs to classify the investment in Investee in line with IFRS 9 and as equity stakes never meet conditions for amortized cost method, it’s clear that this asset would be at fair value either through profit or loss, or through other comprehensive income (more on that here).

Solution #2: Significant influence is kept

Please let me remind you here that although the share of Angelo on Investee’s net assets fell below 20%, it does NOT mean that significant influence was automatically lost.

In fact, you could hold 1% and still have significant influence or even control (but let’s not talk about special purpose entities here).

If Angelo maintained significant influence, then it continues using equity method.

The problem here is that IAS 28 does not say anything about gains or losses on partial disposals when equity method is kept. However, I’ve seen it a few times and the practice is that yes, gains or losses are recognized.

The journal entry is:

-

Debit Profit or loss – loss on partial disposal of shares: CU 2 720

-

Investment in associates: CU 2 720

And then, Angelo continues with equity method, but the new percentage of ownership must be applied.

In these short examples, I ignored other possible complications, such as foreign currency translations or items reclassified from other comprehensive income – just make sure you take them into account.

Have your eyes open and watch your back!