What to disclose under IFRS 7 Financial Instruments: Disclosures

About 3 years ago, I was reviewing the financial statements of a medium-sized company providing consumer loans.

They needed the IFRS financial statements due to lots of loans taken from foreign banks. Usually, these banks require bigger debtors to provide the financial statements annually.

So I was checking the notes to the financial statements.

The numbers added up, everything was balanced, everything looked nice and clean.

But, I still had the strange feeling in my bones that something’s not right.

And suddenly it hit me.

The company did not present any notes about the financial instruments (loans taken and loans provided), except for the breakdowns of carrying amounts.

When I told the CFO, he immediately replied:

“I find it strange, but there are NO disclosures required by IFRS 9 Financial Instruments.”

Hmmm, that is actually true.

But the reason is that IFRS 9 is too complex and bulky and therefore standard-setters decided to put the disclosure requirements to totally different standard.

You guessed it – it’s IFRS 7 Financial Instruments: Disclosures.

Sometimes, people just don’t realize that it does not end up with IFRS 9…

So we spent additional day preparing the tables with maturity analysis, credit loss analysis, sensitivity analysis, descriptions and other things.

In this article, I want to show you what disclosures are required by IFRS 7 so that you realize that it’s additional work to do on top of your accounting records.

You should be aware of IFRS 7 also when you are NOT a financial institution, because this standard applies for everyone having financial instruments.

No exceptions.

So even if you have just trade receivables and trade payables, you should watch out.

Who should care about IFRS 7 Financial Instruments: Disclosures?

The standard IFRS 7 prescribes the disclosure requirements for all entities that have some financial instruments in their books.

It was first published in 2005 and it replaced very old standard IAS 30 Disclosures in the Financial Statements of Banks and Similar Financial Institutions.

But, while IAS 30 applied only for banks and financial institutions, IFRS 7 applies to everybody.

So even if you work for a trading company and you have some loans and lots of trade receivables, then yes, you should be familiar with IFRS 7 to know what to include in your notes to the financial statements.

There are some types of instruments that are exempt from IFRS 7 and you should provide disclosures in line with other standards, such as:

- Subsidiaries, joint ventures, associates

- Insurance contracts

- Employee benefit plans

- Share-based payments

- Equity instruments in line with IAS 32 (here, OWN equity instruments are excluded, not the equity instruments in other entities as these are your financial assets)

What disclosures are required by IFRS 7?

IFRS 7 requires certain disclosures in 2 main areas:

- Significance of financial instruments, and

- Nature and extent of risks from financial instruments and how they are managed

Let’s break it down.

Significance of financial instruments

These disclosures are necessary to understand whether the financial instruments are significant for entity’s financial position and performance.

They are divided into few subgroups and let me list a few of them here for your information:

- Disclosures for the statement of financial position:

- Carrying amounts of your financial instruments by their categories

- Financial assets or financial liabilities measured at fair value through profit or loss (FVTPL)

- Investments in equity instruments designated at fair value through other comprehensive income (FVOCI)

- Reclassifications

- Offsetting financial assets and financial liabilities

- Collaterals

- Allowance account for credit losses

- Compound financial instruments with multiple embedded derivatives

- Default and breaches

- Disclosures for the statement of comprehensive income:

You should disclose the tiems of income, expense, gains or losses (by categories), mainly:- Net gains or net losses on each category of the financial instruments

- Total interest revenue and total interest expense

- Fee income and expense

- Analysis of the gain or loss in the statement of comprehensive income from the derecognition of financial assets at amortized cost

- Other disclosures:

- Accounting policies

- Hedge accounting disclosures (risk management strategies, effect of hedge accounting…)

- Fair value (how it was determined, fair values of FA and FL, explanations when the fair value cannot be determined)

You should disclose most of the information listed above in breakdowns at least by the categories of financial instruments.

Nature and extent of risks from financial instruments

This part of the disclosures is really demanding, because it requires additional analysis and work, especially for market risk disclosures.

IFRS 7 requires qualitative and quantitative disclosures for three main risks:

- Credit risk

- Liquidity risk

- Market risk

For each type of risk, you should disclose:

- Qualitative disclosures:

Here, you would normally describe how the company is exposed to the risks, how the risks arise and how it manages these risks. - Quantitative disclosures:

You need to provide a summary of quantitative data (numbers) about the exposures to the risk.

It’s a lot of details and IFRS 7 requires specific quantitative disclosures for each type of risk (see below).

You should also provide the disclosures about the concentration of risks.

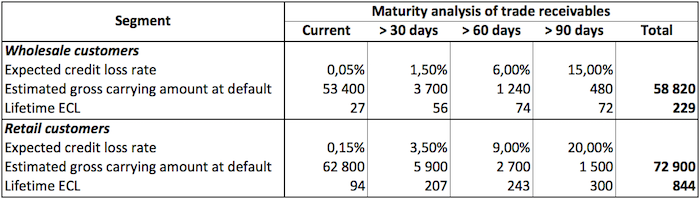

Credit risk

Credit risk relates to your financial assets and simply speaking, it is a risk that you will suffer a financial loss due to counterparty failing to pay its obligations.

If you have trade receivables or you provide loans, then you are exposed to credit risk and you should focus on this part of the standard.

You should disclose:

- Credit risk management practices

- Information about amounts arising from expected credit losses

- Credit risk exposure

- Collateral and other credit enhancements obtained

This is one example of how your quantitative credit risk disclosure can look like for trade receivables:

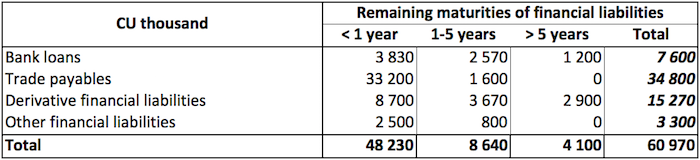

Liquidity risk

Liquidity risk relates to your financial liabilities and it is a kind of “opposite” to the credit risk.

It is the risk that YOU will not meet your obligations from financial liabilities to be settled with cash or another financial asset.

You should disclose:

- Maturity analysis of financial liabilities with remaining contractual maturities (separately for non-derivative and derivative)

- How you manage the liquidity risk

Here, there’s an illustration of quantitative risk disclosure for liquidity risk:

Market risk

Market risk is the risk that either the fair value or future cash flows from your financial assets or financial liabilities will fluctuate due to changes in market prices.

Market risk has a few components, based on what causes the change in future cash flows or fair value:

- Currency risk: the risk that foreign exchange rate changes cause the fluctuations in cash flows or fair values;

- Interest rate risk: : fluctuations are caused by the changes in interest rates;

- Other price risk: Fluctuations are caused by the changes in other market prices, such as commodity prices, equity prices, etc.

The disclosures for market risk are quite demanding and require some work, because you need to produce sensitivity analysis.

There are two types of sensitivity analysis and you can choose the one that’s the best in your situation:

- ”Basic” sensitivity analysis:Here, you need to simulate the changes in certain variable (interest rate, foreign exchange rate, etc.) and show how profit or loss and equity would have been affected.

- Value-at-risk analysis:Here, you need to analyze interdependencies between variables, for example between interest rates and exchange rates.

Other disclosures

Except for these 2 big groups of IFRS 7 disclosures (significance and nature of risk), there is few more information required about:

- Transfers of financial assets, and

- Information required on initial application of IFRS 9

How to present the disclosures?

As you can see from the above summary, IFRS 7 requires loads and loads of information to be presented.

So, if you want your disclosures to be useful for the readers, please bear a few rules in mind:

- Lots of disclosures are required by the classes of financial instruments (for example, credit risk disclosures or liquidity risk disclosures).

Classes are not the same as categories of financial instruments and here, you should group your financial instruments into classes according to your judgment, what’s the best for your readers to understand.Also, you don’t need to use the same classes for different risks. - You can provide the disclosures in an integrated package.

Thus, one disclosure can satisfy more requirements. - Find the right balance between the level of detail and materiality.

Make sure you include all material information, but don’t include excessive details about items not significant that much, because otherwise the users will be confused and the disclosures would be useless.

Further reading and video

If you’d like to read more about the risk disclosures as required by IFRS 7, here’s an article by our guest author John Orford published some time ago (it still applies!): The Quick Guide to IFRS 7 Risk Disclosures

Here’s the video with the summary of IFRS 7:

Any comments or questions? Please let me know below. Thank you!

[addtoany]JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

20 Comments

Leave a Reply

Dear Silivia,

Under IFRS for sme’s, how to treat the following issue:

There is a reduction in net assets due to net deficit made during the financial year. And it continues to reduce over a number of years until there is nothing postive to record. Is there any standard under IFRS which can guide me on the treatment and disclourses. Please advise. Thanks

Hi. I am just dropping a comment to say that you’re doing a quality discussion. No questions, I am only appreciating your hard work.

Good day Silvia,

Am actually doing a paper work on the effect of IFRS7 on financial reporting quality of deposit money banks.

I will be glad if you can help me out.

Thanks so much Dr. Silivia .

Hi Silvia, It is great contribution towards knowledge sharing of recent developments and helps everyone in the carrier. Would like to know specific doubt, do Fair value / Amortized Cost is applicable to Financial Liability as well?

Hi Lakhsminaraynan, yes, to some extent it is similar – you either keep financial liabilities at fair value or at amortized cost. But, recognition of gains/losses is different in some cases. S.

Silvia, thanks so much for the post.Much thanks again. Really Cool.

If there is a bank had financial instruments in past year, but in current year there are none as the bank is moving towards dissolution, then is it required to give a financial instrument note?

Hi Apoorv,

yes, because it needs explanation of the movement in financial instruments. Of course, the extent of disclosures would be different and note about liquidation would explain a lot. S.

Wow!! I’m now seeing this. Thanks alot Silvia. This was extremely helpul. God bless you?

Thank you Silvia for sharing this insightful article,could you show us by example calculation of these two types of sensitivity analysis.

1.Basic sensitivity analysis,and

2.Value-at-risk analysis.

Hi Peter,

great question and suggestion, I will try to cover that in some future article. S.

Thank you Silvia, you’re simply the best!.

Thank you Silvia for this quality materials. However, how do we download it so as to revise this guidance at any time you want to revisit it offline.

Hi Edmund,

you can download the video from YouTube, I guess. As for this text, just save the page as html to your computer and you can read it offline, too. S.

Awesome, God bless you, i always love your new vedios

Great, enjoy 🙂

thank you, Silvia, this was very useful, I am studying for my P2 and it will help!

I am very happy to help, good luck!

Thanks, you are the best