IFRS 18 Explained: Full Guide + Free Video Lectures + Checklist

Updated in June 2025

IFRS 18 was issued in 2024 and is mandatorily applicable for the period starting on or after 1 January 2027, with earlier application permitted.

However, please watch out because we need to apply IFRS 18 retrospectively, with the restatement of the comparative period.

It means that if you apply IFRS 18 from 2027, also the numbers for 2026 must be presented in line with the new rules.

IFRS 18 replaces the oldest standard IAS 1 Presentation of Financial Statements which will no longer applicable.

This summary splits the topics covered in IFRS 18 to the following subtopics:

1. Free VIDEO lecture: Overview of IFRS 18 Presentation and Disclosure in Financial Statements

2. Introduction: Objective, scope, definitions, separating and aggregation;

3. General requirements for financial statements;

- 3.1 Objective of financial statements

- 3.2 A complete set of financial statements

- 3.3 Primary financial statements and their roles

- 3.4 Identification of financial statements

4. Profit or loss statement – main changes here!;

- 4.1 Top 4 changes in Profit or loss statement (free VIDEO lecture)

- 4.2 Categories in the statement of profit or loss

- 4.3 Totals and subtotals in statement of profit or loss

- 4.4 Line items to be presented in profit or loss

5. Statement of other comprehensive income

6. Statement of financial position

7. Statement of changes in equity (with free VIDEO lecture)

8. Notes (with free video lecture on MPMs)

9. DOWNLOAD IFRS 18 Practical Checklist

10. Further reading&learning

1. Overview of IFRS 18 Presentation and Disclosure in Financial Statements (free VIDEO lecture)

2. Introduction to IFRS 18 Presentation and Disclosure in Financial Statements

2.1 Objective of IFRS 18

IFRS 18 establishes the requirements for the presentation and disclosure of the information in the general purpose financial statements.

The objective is to make sure that entities provide relevant information faithfully representing entity’s assets, liabilities, equity, income and expenses. (see IFRS 18.1)

2.2 How to apply IFRS 18

We need to apply IFRS 18 retrospectively, with the restatement of the comparative period.

It means that if you apply IFRS 18 from 2027, also the numbers for 2026 must be presented in line with the new rules.

2.3 Scope of IFRS 18

IFRS 18 applies to all entities preparing general-purpose financial statements under IFRS Accounting Standards.

It sets the rules for how to present and disclose information in the primary financial statements and while it includes general guidance relevant for the statement of cash flows, the details remain in IAS 7.

Also, IFRS 18 does not apply to interim financial statements under IAS 34 (with some limited exceptions).

Entities in the not-for-profit or cooperative sectors can apply IFRS 18, but they may need to adapt some labels and presentation formats to reflect their specific structures.

3. General requirements for financial statements

3.1 Objective of financial statements

The objective of financial statements is to provide financial information about a reporting entity’s:

- assets;

- liabilities;

- equity;

- income; and

- expenses,

so that the users of financial statements can assess the prospects for future net cash inflows the entity and management’s stewardship of the entity’s economic resources. (IFRS 18.9)

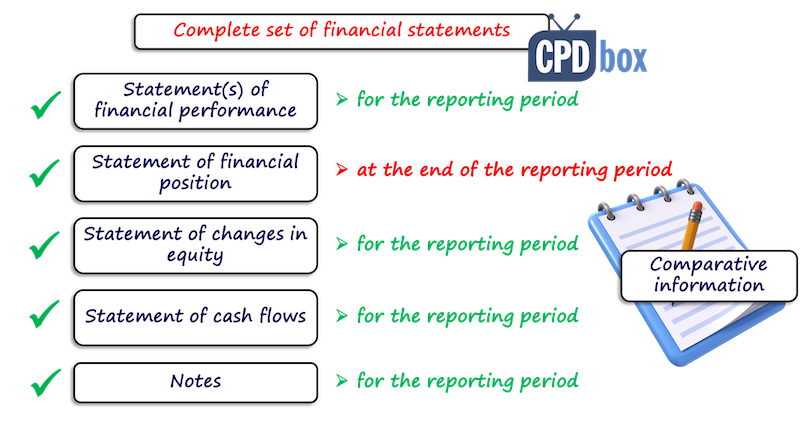

3.2 A complete set of financial statements

The components of the complete set of financial statements are (IFRS 18.10):

- a statement(s) of financial performance for the reporting period;

- a statement of financial position as at the end of the reporting period;

- a statement of changes in equity for the reporting period;

- a statement of cash flows for the reporting period; and

- notes for the reporting period;

- comparative information for the preceding period;

- a statement of financial position as at the beginning of the preceding period if required (i.e. when applying the new accounting policy retrospectively or makes material restatement retrospectively).

As for presenting the statement of financial performance, there are two options to present it as:

- a single statement of profit or loss and other comprehensive income, in two sections; or

- two separate statements.

3.3 Primary financial statements and their roles

3.3.1 What are the primary financial statements?

- a statement(s) of financial performance for the reporting period;

- a statement of financial position as at the end of the reporting period;

- a statement of changes in equity for the reporting period;

- a statement of cash flows for the reporting period; and

their comparative information.

The primary statements provide a structured summary of the key numbers.

Therefore, the notes for the reporting period are NOT a part of the primary financial statements. Instead, they support and expand on this information by offering necessary explanations and additional details.

3.3.2 What are the roles of the financial statements?

- Primary financial statements:

- to give users an understandable overview of the entity’s financial position and performance;

- to allow for comparisons between companies and between reporting periods; and

- to help users identify areas that may require deeper analysis — which is typically provided in the notes.

- Notes: They play a complementary role:

- to explain the line items presented in the primary financial statements;

- to provide further detail where necessary (including disclosures to fully understand the financial implications of transactions, events, and conditions).

3.3.3 Material information

Information included in the financial statements must be material.

Even if an IFRS standard lists certain items or calls them “minimum requirements,” an entity is not required to present or disclose immaterial information.

On the flip side, if compliance with specific requirements is not enough to give a full picture, the entity should include additional disclosures.

In practice, the primary statements are more aggregated, while the notes offer more disaggregated and detailed insights.

For example, some line items might be presented as a single figure on the face of the statement, but broken down further in the notes.

Finally, if certain items or subtotals are necessary to provide a clear and useful summary in the primary statements, they must be added — even if not explicitly required by a standard.

However, these additional items must follow IFRS measurement rules, align with the required statement structure, stay consistent over time, and not overshadow the required subtotals or totals.

3.4 Identification of financial statements

All the financial statements must be clearly identified, with the following information to disclose:

- the name of the reporting entity, and any change from the preceding reporting period;

- information about group or separate financial statements;

- date of the end of the reporting period or the period covered;

- presentation currency;

- level of rounding used.

IFRS 18 then sets the main principles, such as:

- Frequency of reporting;

- Consistency, disclosure and classification;

- Comparative information;

- Aggregation, disaggregation and offsetting

4. Profit or loss statement

IFRS 18 brings significant changes and specifications to the presentation of profit or loss, especially by introducing categories of income and expenses, and new subtotals to be presented.

4.1 Top 4 changes in Profit or loss statement (free VIDEO lecture)

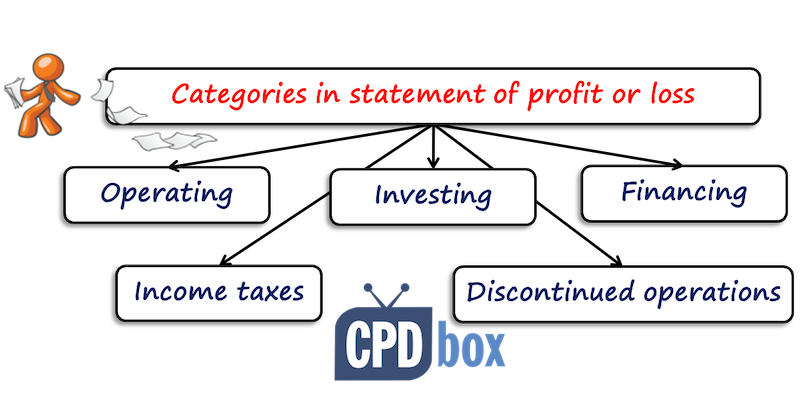

4.2 Categories in the statement of profit or loss

All income and expenses in the statement of profit or loss shall be classified into one of the five categories:

- Operating category – this is a default category and here, all items not included elsewhere are classified.

- Investing category – for example, returns on investments, rentals from investment property, etc.

- Financing category – all income and expenses related to liabilities, either from raising finance (e.g. interest expense on bonds, loans) or from other liabilities (e.g. unwinding the discount on long-term provisions).

- Income taxes

- Discontinued operations

These categories are NOT the same as categories in the statement of cash flows under IAS 7, although they may remind them.

Also, when an entity has specified main business activity, then it classifies certain items differently than other entities:

- If specified main business activity is investing in assets, then those expenses and income related to investing in assets belong to operating category (not investing);

- If specified main business activity is providing finance to customers, then those expenses and income related to providing finance to customers belong to operating category (not financing).

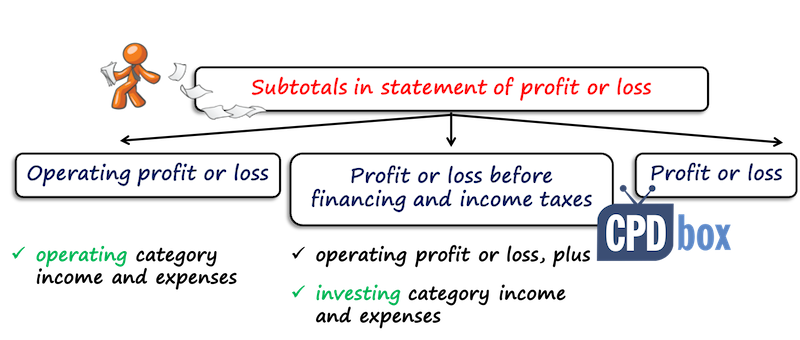

4.3 Totals and subtotals in statement of profit or loss

The mandatory subtotals are also a new requirement in IFRS 18 as compared to IAS 1.

Many entities presented those subtotals anyway, IFRS 18 just specifies how they should be determined.

There are three new mandatory subtotals:

- operating profit or loss – including all income and expenses in operating category;

- profit or loss before financing and income taxes – including operating profit or loss and all income and expenses in investing category;

- profit or loss, including all items in profit or loss.

4.4 Line items to be presented in profit or loss

As a minimum, an entity shall present the following amounts:

- Amounts required by IFRS 18:

- Revenue, with presenting interest revenue and insurance revenue separately;

- Operating expenses (by nature or by function);

- Share of the profit or loss of associates and joint ventures by equity method;

- Income tax expense or income;

- Total for discontinued operations under IFRS 5.

- Amounts required by IFRS 9 Financial Instruments;

- Amounts required by IFRS 17 Insurance Contracts.

On top of these line items, an entity should present profit or loss for the period in allocation:

- attributable to non-controlling interests and

- attributable to owners of the parent.

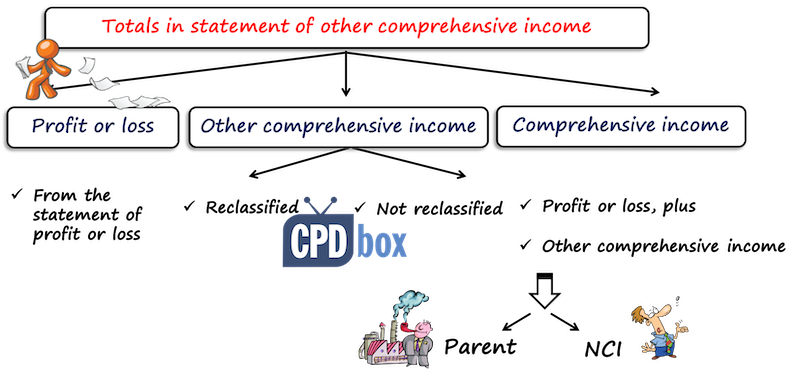

5. Statement presenting comprehensive income

In the statement presenting comprehensive income, the following totals should be shown:

- profit or loss (carried from the statement of profit or loss);

- other comprehensive income, split into two categories:

- items that will be reclassified to profit or loss after certain conditions are met; and

- items that will not be reclassified.

- comprehensive income, being the total of:

- profit or loss and

- other comprehensive income.

Similarly as with profit or loss, an entity should present comprehensive income for the period in allocation:

- attributable to non-controlling interests and

- attributable to owners of the parent.

6. Statement of financial position

IFRS 18 does not change much about the presentation of the statement of financial position (balance sheet) in comparison with IAS 1.

IFRS 18 requires presentation of classified statement of financial position where current assets or liabilities are separated from non-current assets or liabilities.

With regard to a minimum content, the following line items shall be presented:

| ASSETS | EQUITY AND LIABILITIES |

|---|---|

| Property, plant and equipment | Issued capital and reserves attributable to owners of the parent |

| Investment property | |

| Intangible assets | Non-controlling interests |

| Financial assets | Financial Liabilities |

| Investments accounted for using equity method | Provisions |

| Biological assets | |

| Inventories | |

| Trade and other receivables | Trade and other payables |

| Cash and cash equivalents | |

| Totals of assets in accordance with IFRS 5 Non-current assets Held for Sale and Discontinued Operations | Totals of liabilities in accordance with IFRS 5 Non-current assets Held for Sale and Discontinued Operations |

| Current tax assets | Current tax liabilities |

| Deferred tax assets | Deferred tax liabilities |

Further subclassifications of the line items shall be disclosed either directly in the statement of financial position or in the notes, such as disaggregation of property, plant and equipment into classes, and similar.

Also, certain information related to the share capital, reserves and a few others shall be included in the statement of financial position, the statement of changes in equity or in the notes.

IFRS 18 does NOT prescribe the precise format of the statement of financial position. Instead, several formats are acceptable if they fulfill all requirements outlined above.

7. Statement of changes in equity (with free video lecture)

The requirements for statement of changes in equity in IFRS 18 are carried over from IAS 1, so they remain unchanged.

As a minimum, the statement of changes in equity must contain the following items:

- total comprehensive income for the period, showing separately amounts attributable to owners of the parent and to non-controlling interests

- the effect of retrospective application or restatement for each component of equity (if applicable)

- the reconciliation between the carrying amount at the beginning and the end of the period for each

component of equity. Here, the following changes shall be disclosed separately:- those resulting from profit or loss

- resulting from other comprehensive income

- resulting from transactions with owners (contributions, distributions and changes in ownership)

For the practical example showing the preparation of the statement of changes in equity step by step, please see this article with the video and excel file.

Also, IFRS 18 prescribes to present amount of dividends recognized as distributions and the related amount per share on the face of the statement of changes in equity or in the notes.

8. Notes to the Financial Statements (with free video lecture on MPMs)

The notes are meant to be the document accompanying numerical financial statements listed above. They should provide additional information not contained in the numbers, the basis of preparation of the financial statements and some additional information that might be relevant.

IFRS 18 sets that the notes shall contain at least:

- information about the basis for preparation of the financial statements;

- accounting policies used;

- information required by IFRS that is not presented in the primary financial statements – those are all subtotals and additional disclosures as required by other standards;

- other information that is not presented in the primary financial statements – for example, information about significant events or trends or contracts that might affect the business;

.

The notes shall be prepared in the systematic manner and be cross-referenced to the financial statements.

The new requirement in IFRS 18 is the presentation of management-defined performance measures.

You can read more about the notes and how to write them in this article. Here’s the video lecture:

9. DOWNLOAD IFRS 18 Practical Checklist

10. Further reading and learning

Explore more on IFRS 18: Visit this page to access the full library of all IFRS 18-related articles, videos, and examples published by CPDbox.

Learn IFRS with real examples – not just theory.

Any questions? Please let me know below, thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

16 Comments

Leave a Reply

Thank you Silvia for this comprehensive write up.

From a proactive point of view, please what are the potential issues or challenges that companies would face in transitioning from IAS 1 to IFRS 18. What mitigations can be put in place to curb these challenges?

Hi Augustine, thank you! Well, I mention some of the challenges above in the checklist, but it’s a good idea to put down my thoughts and experiences so far related to the change.

Hello my name is Alex Kipchirchir from Kenya, I’m an accountant. I wanted to ask how I can get this notes on IFRS 18: Presentation and Disclosure in Financial Statements: summary

Please download the checklist above – I think that it can be used either to ensure your compliance, or as notes for your studies (study guide). I hope this helps.

Thank you presentation, please can you sending us consolidate Profit or Loss statements format in banking sector according to IFRS 18.

The income and expenses from cash and cash equivalents that should be included in the investing category. Would that include the monthly bank charges / admin fees levied on these accounts? Or does it only relate to the interest income/expense on the cash and cash equivalents?

Only interest income/expense on cash and cash equivalents goes in the investing category. Bank charges and admin fees are operating because they are seen as entity’s expense to manage the account. Of course, when you have an investment account set up just with the purpose of getting investment returns, then that’s a different case.

Just to mention you are amazing! Thank you.

Can explain more on presentation of management-defined performance measures? Is it have to disclose as new para on the “Notes of Financial Statement”?

That’s planned, too 🙂

Where should be FX gains/losses reported according to IFRS 18? In operating part (if they are related to operations)?

Yes, together with the underlying transaction.

Where exactly would you show this? In the same line item as the underlying transaction? Or in a seperate line item “FX losses from operating activities”?

IFRS 18 does not say precisely, so it really boils down to the general rules of materiality, aggregation and disaggregation. If those FX losses/gains represent indeed material item, then maybe it would be appropriate to show them separately, otherwise together with the underlying transaction.

Can you supply us a format of income statement according to IFRS 18

I will publish some examples soon, but there is no prescribed format.