IFRS 16 Leases vs. IAS 17 Leases: How the lease accounting changed

In January 2016, IASB issued another important and long-discussed standard: IFRS 16 Leases that will replace IAS 17.

Ever since then I receive lots of e-mails asking me to sum up what’s new.

OK, so here you go.

In this article, you’ll learn about the main changes that IFRS 16 introduces to the accounting for leases, illustrated on a very simple example.

Warning: this is NOT exhaustive description of the standard, and I simplify the things a lot for illustration purposes.

I will come back to it at the later stage, because I truly think that there will be lots of questions, discussions and additional guidance on how to tackle several areas of the lease accounting.

The effective date of the new IFRS 16 is 1 January 2019.

Why the new lease standard?

Short answer: To eliminate off-balance sheet financing.

Under IAS 17, lessees needed to classify the lease as either finance or operating.

If the lease was classified as operating, then the lessees did not show neither asset nor liability in their balance sheets – just the lease payments as an expense in profit or loss.

But, some operating leases were non-cancellable, and therefore, they represented a liability (and an asset) for the lessees.

This liability was hidden from the readers of the financial statements, as it was not presented anywhere.

Oh yes, some disclosures in the notes to the financial statements were mandatory, but frankly – who, except for auditors, ever reads the notes to the financial statements?

New IFRS 16 removes this discrepancy and puts most leases on balance sheet.

I’ll show you how in the next paragraphs.

Let’s see what has changed

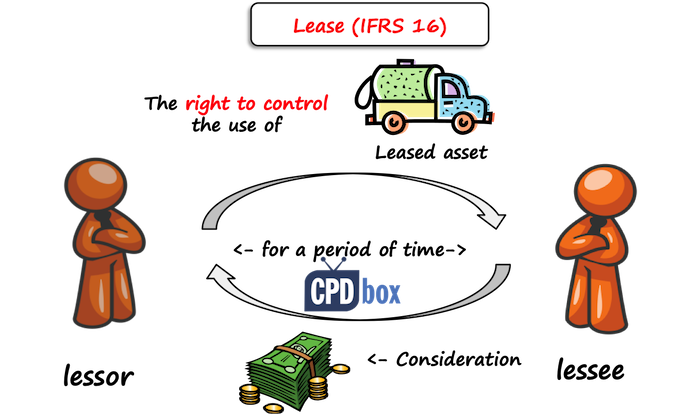

Is it a lease?

The new IFRS 16 introduces a new definition of a lease. However, it is very similar to the old definition in older IAS 17 (differences do exist).

It means that when you actually accounted for some contracts as for lease contracts under IAS 17 Leases, you will continue to do so also under the new standard (careful, methodology may change).

BUT!!!

You have to be extremely careful when it comes to some service contracts.

Why?

Because, the new standard IFRS 16 provides a detailed guidance to determine whether your contract is a lease contract or a service contract (non-lease contract).

Under old IAS 17, it did not matter so much whether you have an operating lease contract or a service contract, for a very simple reason: you probably accounted for both types of contracts in the same way (that is, as a simple expense in profit or loss).

However, as the accounting for some types of previously-called operating lease contracts dramatically changes, we need to distinguish whether we have a lease under IFRS 16 or some other service contract under different standard.

As a simple illustration, let me come up with a small example:

- You will occupy a certain area of XY cubic meters, but the specific place will be determined by the owner of the warehouse, based on actual usage of the warehouse and free storage.

- You will occupy the unit n. 13 of XY cubic meters in the sector A of that warehouse. This place is assigned to you and no one can change it during the duration of the contract.

Both contracts look like lease contracts, and indeed, in both cases, you would book the rental payments an expense in profit or loss under older IAS 17.

Under new IFRS 16, you need to assess whether these contracts contain lease as defined in IFRS 16.

The first thing you would look at is whether an underlying asset can be identified.

Long story short:

- The first contract does not contain any lease, because no asset can be identified.

The reason is that the supplier (warehouse owner) can exchange one place for another and you lease only certain capacity. Therefore, you would account for rental payments as for expenses in profit or loss. - The second contract does contain a lease, because an underlying asset can be identified– you are leasing the unit n. 13 of XY cubic meters in the sector A.

Therefore, you need to account for this contract as for the lease and it means recognizing some asset and a liability in your balance sheet.

This was a very simplified illustration to make you aware of this and it’s by no means exhaustive – but you get a point.

Do we pay only for a lease, or also for some services?

This is another change we need to watch out under IFRS 16.

When you lease some assets under operating lease (as called by older IAS 17), in most cases, a lessor provides certain services to you, such as maintenance, repairs, cleaning, etc.

Under older IAS 17, you did not need to think about it too much, because you put all lease payments as some rental expense to your profit or loss.

BUT!!!

Under new IFRS 16, you need to split the rental or lease payments into lease element and non-lease element, because you need to:

- Account for a lease element as for a lease under IFRS 16 (if it meets the criteria in IFRS 16); and

- Account for a service element as before, in most cases as an expense in profit or loss.

From our example above: let’s say you took the option 2 and you pay CU 10 000 per year. This payment includes the payment for rental of the unit n. 13 and its cleaning once per week.

Therefore, you need to split the payment of CU 10 000 into lease element and cleaning element based on their relative stand-alone selling prices (i.e. for similar contracts when got separately).

You find out that you would be able to rent out similar unit in the warehouse next door for CU 9 000 per year without cleaning service, and you would need to pay CU 1 500 per year for its cleaning.

Based on this, you need to:

- Allocate CU 8 571 (CU 9 000/(CU 9 000+CU 1 500)) to the lease element and account for that as for the lease; and

- Allocate CU 1 429 (CU 1 500/(CU 9 000+CU 1 500)) to the service element and in this case, probably recognize it in profit or loss as an expense for cleaning.

Not an easy thing, especially when the stand-alone selling prices are not readily available.

The biggest change: lessee’s accounting for leases

Here’s the biggest change: lessees (those who take an asset under lease) do not need to classify the lease at its inception and determine whether it’s finance or operating.

You might say: OH YES!!!

But not so fast.

The reason is that IFRS 16 prescribes a single model of accounting for every lease for the lessees. Very shortly:

- Lessee needs to recognize a right-of-use asset and corresponding liability in its statement of financial position.

- An asset shall be depreciated and a liability amortized over the lease term.

This model is very similar to the accounting for finance leases under IAS 17.

And yes, you need to account for operating leases in the same way.

There are 2 exceptions from this rule:

- Lease of assets for less than 12 months (short-term leases), and

- Lease of assets of a low value (such as computers, furniture etc.).

Example IAS 17 vs. IFRS 16

Let me illustrate the new accounting model and put it in the contract with the treatment under IAS 17.

I will continue in the above example of a warehouse. To make it quick, I will just make up some data:

- Annual rental payments are CU 10 000, including the cleaning services, all payable in arrears (at the end of year)

- Appropriate discount rate is 5%

- The lease term is 3 years.

How would you account for this contract under IAS 17 and IFRS 16?

Accounting under IAS 17 Leases

Under IAS 17, you need to classify the lease first.

Let’s say that based on warehouse’s economic life, lease payments, etc. you assess that this lease is operating.

Therefore, accounting is very simple:

- At the commencement, you do nothing;

- At the end of each year, you simply book the rental expense of CU 10 000 in profit or loss.

Accounting under IFRS 16

Here, no classification is necessary as one accounting model applies to all leases.

You need to follow 3 steps:

- Is it a lease under IFRS 16?

Yes, here it probably is. Please see the explanation above.

- Is there some element other than lease element? Do we need to separate?

Yes, we need to separate the cleaning element from the lease element. We did it above:

- CU 8 571 relates to the lease element;

- CU 1 429 relates to the cleaning element.

- How to we recognize these elements?

- At the commencement:

- You need to recognize right to use a warehouse in the amount equal to the lease liability plus some other items like initial direct costs.

- The lease liability is calculated at present value of lease payments over the lease term. In this case you need to calculate the present value of 3 payments of CU 8 571 (only lease element) at 5%, which is CU 23 341.

- Accounting entry is then

-

Debit Right-of-use asset: EUR 23 341

-

Credit Lease Liability: EUR 23 341

-

- Subsequently, when you make a payment and/or at the end of reporting period, you need to:

- Recognize depreciation of the right-of-use asset over the lease term, in this case CU 7 780 (CU 23 341/3) per year (I took straight-line depreciation);

- Recognize remeasurement of the lease liability to include interest, exclude amounts paid and take any lease modifications into account.

- At the commencement:

This simple table illustrates our example:

| Year | Lease liability b/f | Add interest at 5% | Less amounts paid | Lease liability c/f |

| 1 | 23 341 | 1 167 | – 8 571 | 15 937 |

| 2 | 15 937 | 797 | – 8 571 | 8 163 |

| 3 | 8 163 | 408 | – 8 571 | 0 |

| Total | n/a | 2 372 | – 25 713 | n/a |

Note: “b/f” means “brought forward (at the beginning of the year)”, “c/f” means “carried forward (at the end of the year)”.

Summary of accounting entries under IFRS 16:

| When | What | How much | Debit | Credit |

| At the commencement | Right-of-use asset + lease liability | 23 341 | Right-of-use asset | Lease liability |

| At the end of the year 1 | Interest | 1 167 | P/L: Interest expense | Lease liability |

| Rental payment | 10 000 | Cash (bank account) | ||

| 8 571 | Lease liability | |||

| 1 429 | P/L: Expenses for cleaning services | |||

| Depreciation | 7 780 | P/L: Depreciation | Right-of-use asset | |

Now, let’s compare.

Under IAS 17, the impact on profit or loss in the year 1 was CU 10 000, as we recognized the full rental payment in profit or loss.

Under IFRS 16, the impact on profit or loss in the year 1 was:

- Interest of CU 1 167, plus

- Depreciation of CU 7 780, plus

- Expense for cleaning services of CU 1 429.

- TOTAL of CU 10 376.

Hmmm, that’s actually more expenses in the first year under IFRS 16 than under IAS 17, isn’t it?

The reason is that thanks to the new model, the pattern of expenses has changed: we have loads of interest in the beginning of the lease, but smaller expenses at the end of the lease when the lease liability is amortized.

In total, both models have the same profit or loss impact over total lease term:

| Type of expense | IAS 17 | IFRS 16 | Note |

| Rental expense | 30 000 | – | 3*10 000 |

| Interest expense | – | 2 372 | Table above |

| Depreciation | – | 23 341 | 3*7 780 |

| Cleaning expenses | – | 4 287 | 3*1 429 |

| Total | 30 000 | 30 000 | |

Note: I am showing the cleaning expenses, too in order to show total impact of the whole contract, although technically they are not part of the lease accounting.

Also, under IFRS 16, we show more assets on the balance sheet, but also more debt or liabilities.

Please note that the cash flow does not change. You pay still the same amounts whether you apply IAS 17 or IFRS 16.

What about Lessors and accounting for leases under IFRS 16?

Good news, folks!

Accounting for leases by lessors almost does not change, so they can continue in the same way.

That’s all I need to say about it.

Final warning

The new lease standard will have significant impact on the companies heavily working with operating leases, no questions about it.

The financial indicators of these companies can substantially change, because new assets and liabilities are coming to the balance sheet.

Also, many lessees will have a hard time to set up a system of gathering and analyzing enough information to satisfy new requirements.

I will stop here, as this post is longer than I expected, but if you have some ideas or remarks on whether and how the new standard can affect your company, please let us know below in the comments. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

251 Comments

Leave a Reply

Hi Silvia

Thank you for your summarized and simple presentation in IFRS 16. i would like to know the situation when interest rate on lease amount change on semi annually. how we account for the changes in interest rate in right to use of asset because we treat interest rate as a discount factor to calculate Present Value of an asset.should we reassess asset PV semi annually when interest rate changes ?

Kind Regards,

Asif

Hi Silvia

I would like to enquire if the rented equipment is subsequently sent for repair and the owner gave some rental refund for the repair period, can the amount go directly to PL instead of affecting our initial Lease Liab calculation? thanks

Under IFRS 16 it does not affect the lease liability because the variation was not caused by change of the lease term or other circumstance. This item simply does not enter into variable lease payments.

Hi Silvia

I want to understand the concept of novated leases. In case employer has taken on lease car for specified no. of years from a finance company and given this car to employees for their personal/ official use. Would that be covered under IFRS 16 ? Currently company is recognising the amount paid to finance company under salary cost. Could you please explain how this will be treated under IFRS 16?

Hello Anjali,

currently the employer is maintaining the books according to IAS17, and charging the cost in P&L as expenses. This can be implemented through IFRS16 and for that reason employer will be the lessor and finance company will be the Lessee.

The cost of the asset will be amortized in SLM over the life of the asset and interest will be charged on the asset on a discounting factor and this will be decreased by the lease payment as per the payment method applied.

Hope you got your answer. Let me know your feedback.

Dear Silvia,

Can you advise please, how we need to eliminate entries under IFRS 16, if lessor is a Parent company and leasee is a subsidiary?

Well, you will simply reverse everything as no lease has ever happened. Even the cash movement – since this is a full consolidation, no cash moves outside the group. S.

Hi Silvia

I have a transaction whereby a land owner has entered into a 99 year lease agreement with an individual who will occupy the land for that period and may build a residential property on it, at the end of the term the land owner may buy back that building at 50% of its fair value.

The buyer/lessor pays the whole amount (equal to the value of the land) up front.

Can the land owner recognise this as a sale; derecognise the land and recognise a profit?

Or does the land owner have to recognise a revenue over 99 years?

Please help

Hello Hamza,

Lease of a property and sale of a property is not same. If it is under a lease then the owner should be having the actual ownership of the land and if it is a sale then ownership is now in buyer hand.

According to the scenario, if it is a 99yr lease then why the buyer has paid the total value of the land ?

also after payment if the ownership has been transferred to the buyer then lessor can show it as profit and de-recognized it as a sale . but if the ownership has not been transferred then lessor can not show it as a profit rather than it will be a term payment for the 99yeras.

Hope u got your answer & please share your feedback accordingly.

Dear Silvia

I would like to ask about how to calculate the amount 23,341.

8571 per year x 3 = 25,713

Then there is an interest 5%.

Will that be 25,713 x 95%? =24,472 at the commencement day?

I am sorry, I really have no idea.

Please help.

I just want to say thank you for this clarification re IAS 17 and IFRS 16 though i’m aware some real-life situations may not be this simplified.

Dear Silvia,

As per this standard can we treat cancellable leases as short term leases.

Dear Silvia,

in some parts of your presentations regarding the application of IFRS 16, you indicate that the lease period is determined only for the non-cancellable period (+possible extension of the contract).

Does this means that contracts that do not have a specified non-cancellable period are not under the jurisdiction of IFRS 16? The lease payments are recorded in profit or loss.

Did I understand it well?

Thanks.

Hi Sanela, no, not quite, but non-cancellable period is crucial for determining the lease term. You can read more about the lease term here.

Dear Silvia,

The lesson is very useful, thank you for that.

This way I would like to kindly ask you one more question. The value of the lease liability includes all payments that are not paid at the commencement date: fixed payments, variable payments, residual value guarantees, exercise price of purchase option and penalties for terminating.

What about lease contracts that do not have an agreed fixed price? The company leases equipment, and the rental price is determined based on hours of use of this equipment. So the rental price is not fixed, it depends on the use of the equipment.

Thanks.

Hi Silvia, when i disclose operating lease commitments on the Annual Financial statements do i include VAT or exclude it . My second question is when i enter into a new contract with the lessee and pay a deposit, do i include the deposit on the straight lining ?

Thanks

Hi Silvia, is IFRS16 applicable for leasing apartments (typically 2 years contract) for expats/employees to stay as part of their employment package

Yes.

Hi,

There are some lease for offices for which the initial duration of the contract has ended and since then the contract is silently renewed every year. In this cases how do we determine the lease period which will be used for the calculation of the RoU and Lease liability? Can it be applied the exception for leases with duration less than one year and expense the rent amount instead of bringing them on BS? What is the best practise?

Many thanks,

Petros

Hi Petros, please read this. S.

Hi

I would like to know how to calculate the lease liability and right of use asset with the following conditions:

a) Annual escalation of 8%

b) 29 months left of a 5 year lease.

The escalation clause is confusing me…

And do you measure the lease liability for 5 years, and then subtract the 271 months paid so far?

Please advise

Hi Swaleha,

it is the lease modification and in the inception, you do not take this into account (simply take initial payments for full 5 years). When the lease payments change, you recalculate your lease liability with new payments and account for the adjustment. It is very simply said. I have great excel examples exactly on these issues in my IFRS Kit. S.

How about upon depreciation of the PPE? Since under IFRS 16 Operating lease was eliminated in Accounting for lessee. All lease shall be classified as Finance lease unless it is a low value asset and the lease term is only for 12 months, then we have to account the right of use asset under PAS 16 using either Cost model, Fair value model or revaluation model. Under Cost model, we have to recognize Depreciation Expense yet as per books of the lessor if the lease was accounted as operating lease, the PPE shall continue to be recognized in its books thus recognizing depreciation expense as well, in that case the PPE will be depreciated under the books of both lessor and lessee accounting. depreciating the same asset at different amount?

Yes. I have answered the same question multiple times. The accounting for leases is NOT symmetric anymore. And, the right-to-use asset is not the same as underlying asset itself. Yes, both lessee and lessor depreciate something.

What if the lessor is a parent entity and the lessee is its subsidiary? Upon preparation of consolidated FS both amounts will be recognized, does it makes the FS overstated?

They won’t be recognized both, because you must eliminate intragroup transactions and thus all leasing in subsidiary will be removed on consolidation (there’s no lease from the point of external user).

Thank you so much Sylvia,

Dear Sylvia,

Under IFRS 16:36 (subsequent measurement of lease liability) as stated there, Why is it that the carrying amount of lease liability is to be increased by its interest expense? Thank you so much.

Because at initial recognition, your lease liability was discounted to present value and you need to bring that present value to the future value by unwinding the discount = increasing it by its interest expense.

is this the same with the previous amortization of the lease liability under PAS 17? Im so sorry I got confused. Thank you in advance

Yes, essentially the same as IAS 17.

Dear Silvia,

Under IFRS 16 for the lessee there is no finance or operating lease its a same treatment ” right to use assets” well if the lessor is a Holding company and the lessee is a subsidiary what about elimination entry regarding a consolidation financials when we apply the operating lease ” The same assets will booked in the two entity and deprecated but in a different amounts ?

Dear Silvia,

My company currently uses a warehouse under IAS 17 operating lease where the lessor provides repairs and maintenance. My company paid the lessor for water and electricity usage. Air Condition units were installed and maintained by my company. How does this changes come January 01, 2019 under IFRS 16?

Hi Lydia, well, most probably you will need to recognize a right-of-use asset because if you are a lessee then you do NOT classify the lease as either finance or operating. You book all the leases the same way, with small exceptions.

Hi Silvia,

Could you please share the article for more details about the exception.

I am dealing with the same case. Lease warehouse for 2 years with no purchase option and economic life of the warehouse is unknown. should we charge Depreciation and interest?

Dear Silvia, I would like to first thank you for demystifying IFRSs that seemed to be complicated.

Now I want to ask if there is a circumstance where Right Of Use asset will be higher than Lease liability since we have to recognize ROU asset in the amount equal to Lease liability plus some other items like initial direct cost if any.

Thank you

Yes, of course, there can be such circumstance.

Dear Silvia,

Thank you for the insightful details and example. In the accounting entries proposed, how would you address the entries generated by the normal process of payment when you commit to the rental and then pay the invoices? In most of the ERP used, when your P2P process is automated, a commitment (contract rental) will generate an entry in the P&L (Cost of rental) balanced with Vendor account. In the table Summary of accounting entries under IFRS 16 we may therefore need to reverse these entries before proceeding to the booking of IFRS 16 postings in order to avoid recognizing twice the cost (once through depreciation, and once through invoice). Do you see any other way to avoid such reversal mechanism as it may be really complex of you have to go through different allocations process (from analytical accounting and costing point of view)

Hello Silvia,

In our group of companies (60 companies) all companies enter the lease cost into their legal books in the P/L. How do we treat that “technically” when consolidating on group level? I mean we can’t have both the lease cost and the depreciation/interest cost in the P/L. Do we “eliminate” the same amout as the total sum of depreciation and intrest ending up with just a reclassification of part of the costs or are we supposed to remove the lease costs in total (and which account should then be used as “counter part”) and only have the depreciation/interest elements left in P/L?

Br /Maria

Hi Maria,

exactly as you say. You should take 2 steps:

1) Eliminate everything NOT under IFRS, and

2) Recognize it under IFRS 16.

So you need to reverse whatever lease costs in P/L and recognize them under IFRS 16. I wrote 2-part article on this topic here and here, plus in my IFRS Kit there is a full lecture on how to do exactly these adjustments. S.

I work for a bank (Ghana) and as usual most of the banking premises are rented. As at now, we treat them as operating leases. Here in Ghana, the lessors will normally ask you to pay say 3 years rent advance. Repairs and maintenance cost are borne by the lessee.

When we pay the rent advance (say $36000 for 36 months), we debit Rent prepaid and credit cash. After that we amortize the total rent paid over the duration of the rent agreement. In this example, we debit p/l $1000 and credit rent prepaid $1000 every month.

Please I will like to know how will IFRS 16 affect us

Thank you

Hi Efface,

yes, IFRS 16 affects you, because instead of accounting for prepaid rent, you have a right-of-use asset here, so you need to account for Debit ROU asset/Credit Cash (or lease liability, but if the full rent is prepaid, then just cash). And then you need to depreciate ROU asset.

Hi Silvia,

I think if we separate the payment CU 8.571 equal Interest CU 1.167 + Principal (asset) CU 7.403 (end of first year), and then we make accounting treatment base on this; that will make its easier.

Ex. for that:

Debit P/L interest 1.167

Credit Cash 1.167

Debit Lease liability 7.403

Credit cash 7.403

Debit P/L Depreciation 7.780

Credit Right-to-use-asset 7.780

Hi Silvia.

your efforts to simplify IFRS is very appreciated and considered.

Please, I want to ask if we pay the rental fees at the beginning of each year not in the end,

1- I will record the assets and liabilities only or there are any other accounts.

2- The asset and the liabilities will be 0 (zero) at the end of the year.

Thanks in advance.

Hi Silvia,

Thanks for the article!

It is a little bit mindblowing for me.

I remember attending one of the seminar in my country. The speaker was senior auditor in KPMG. He brought this topic, and in the end I ask him question, whether rent office treatment will be impacted by this IFRS 16 or not. He was a little bit hesitant but in the end confirmed that rent office should be out of scope since there is no option to purchase the office.

But I think that is false, moreover after read you article, I am pretty sure that rent office should be recorded under IFRS 16.

But some question that is still confuse me:

1. In notes to financial statement we need to disclose long term commitment. Usually lease office contract will be described in here. Stated how long until the contract expired and how much the residual contract value that need to be paid. In this case, we do not need this anymore? Since in the first place we have already record as long term lease payable.

2. also in lease contract usually do not mentioned any interest. Not like car lease contract. How do we determine the discount rate?

Hi Ridwan,

I beg to disagree with your speaker – yes, rent of offices can be affected by IFRS 16, depending on the specific conditions in the contract. For your other questions, it is too long to respond in the comment, but please check this article and also this one, they will help. S.

Hi Ms. Sylvia!

Great article, thank you! What about security deposits? I’ve been googling a while and still can’t find the right IFRS, so I’d really appreciate your help.

1. security deposit – nonrefundable. do I recognize this like a lease incentive and offset from commencement date?

2. security deposit – refundable. so as this is a financial liability, I should amortize. however, where do I charge the amortization? one article says to charge the difference to lease liability?

so:

dr. cash 1000

cr. xxx

cr. lease liability 900

and every month

dr. xxx

cr. lease liability

Hi Silvia,

A few questions below:

1) My company leased out shop space to inter-company over a fixed lease term but on a variable component of the sales (10% of nett sales for the month). In this case, what will be the base of the rent that we should use to PV? Can we use the average of 12 months sales over 5 years?

2) Since this is an inter-company transaction, there will be no implicit interest rate that has been included in the rental agreement. In such a case, what kind of similar incremental borrowing rate should be used? There are also no borrowings for the company so I cannot use any comparative to determine the incremental borrowing rates to use. Can you please advise what rate should be used?

Appreciate your kind advice.

Thanks.

Hi Lyn,

1) No. Please see this IFRS Q&A session, it will help.

2) Yes, that’s difficult to determine, but you can start looking to the banks and the rates that they offer on similar loans to similar clients. I will make another Q&A session on this topic.

S.

This is the best article/summary I’ve read anywhere on the internet, thank you!

Hi Silvia,

We are a wind power company, we have an agreement with an electric company to provide them with all output generated by the wind farm, the contract is for 20 years and the electric company has an option to purchase the power plant after 20 years (two other choices are available: extend the project or decommissioning), there are no fixed monthly charges (it depends on the monthly actual output multiplied by the tariff). The expected useful life for the wind turbines is 20 years. In this case, which accounting treatment shall be applied? IAS 16 or IFRS 16?

Hi Silvia,

could you please clarify the different in the sale & lease back under IAS 17 and IFRS 16?

Hi Silvia

Paragraph 4 mentions that “a lessee may, but is not required to, apply this Standard to leases of intangible assets…”, does this mean we can decided whether or not these contracts are included as a lease asset/liability or expensed?

Yes 🙂

Hi Silvia,

It was a simple and a good read.

I have a question, Can you help me in understanding whether Asset & liability recorded under IFRS 16 requires re-statement as per IAS 21 – “The effects of changes in Foreign Currency”” ? .

Your earliest response will be helpful.

It’s a non-monetary asset, similarly as PPE or intangible asset and no, you do not revalue it at the year-end.

Hi Silvia,

Thanks for your explanation in simple terms. I have a query in terms of both IAS 17 and IFRS 16.

Example- A bank has opened a branch at a building, by signing a rental agreement with the landlord of the building on which branch is situated. The cost of the structural works in that building for setting up bank is 100,000, which will be borne by the bank. The terms of the agreement are as follows: The initial agreement will be for 10 years amounting 10000 per month and price will increase by 10% every 2 years. Either party can terminate the agreement at any time by giving two month’s notice. The tenure of the agreement can be extended at both parties consent.The bank has no intention to discontinue the branch operations in near future. However, loss making branches may be subject to relocation or closure in the future.

In this case, is the lease agreement non-cancellable in nature as per IAS 17,IFRS 16? And how should the accounting and disclosure be done as per IAS 17 and IFRS 16?

Hi Shiva,

no. In this case, the lease is non-cancellable only for 2 months, especially when each party can terminate with 2 months notice without any significant penalty. The reason is that the lease is non-cancellable as long is it is enforceable and it is not enforceable beyond 2 months. I recommend reading the paragraph IFRS16.B34 for the reference. As for accounting – you just book rentals as an expense. You can capitalize the structural works as “leasehold improvements” and depreciate them over the useful life.

Would you mind if I use this question with your first name in my podcast (as for example here)? I think more people would appreciate the answer. S.

Of course and thanks for the answer.

Thanks for the answer. Regarding accounting treatment, should the rental expenses be booked as per actual rental cost payable or should it be on a straight line basis over the term of the lease by taking into account 10% increment on rent amount every 2 years.

And for podcast, of course , yes and thanks.

Hi Silvia,

Thank you for great article.

In IAS17 definition of interest rate implicit in the lease clearly states that it should be determined at the lease lease inception (based on the fair value of asset on inception date and discounted to present value to inception date). But in IFRS16 definition of interest rate implicit in the lease does not clarify this, it seems IASB guys remove this intentionally.

Please share your opinion – should we calculate implicit rate at lease inception or commencement?

Thank you

Hi Silvia

Your article is very helpful.

I was just wondering what will happen to corporation tax position. Will we be adding the asset to capital allowances and claiming AIA?

Dear Raja,

in fact, this is good question and I don’t have the same answer for everyone, because it really depends on the tax rules of your own country. In our country, the tax legislation does not know the term “right-of-use asset” and operating lease expenses are fully deductible – which gives rise to the deferred tax. S.

Wowda! Good article da! I like it da!

How did you reach to the result of 23,341 as a lease liability b/f in the first year? Can someone explain as to how this was calculated.

Dear Bander,

this is clearly written above in the article: “The lease liability is calculated at present value of lease payments over the lease term. In this case you need to calculate the present value of 3 payments of CU 8 571 (only lease element) at 5%, which is CU 23 341”. S.

Thank you. I am sorry, the present value of three payment is 8571*3=25871*5%=1285.65 I know it is wrong but could you please guide me on how can I reach to 23,341

Yes, Bander, that’s wrong – I have no idea what you have calculated. The present value is calculated as 8571*1/(1,05^3)+8571*1/(1,05^2)+8571*1/1,05 – these 1/(1,05^3) etc. are discount factors for 3 years and 5%… etc. S.

Thanks for the great article! I have a question about lease of land. Lease of land will still be reported as operating, aren’t I right? It should not be reported in balance sheet as long as it is not appreciable. So reporting of land will stay according to IAS 17?

Thank you

I meant depreciated of course instead of appreciable :))

No, Alex. Under IFRS 16, if you are a lessee, you do NOT classify the lease anymore and every single lease is reported in the same way. However, let me remind you that you will NOT show the land itself in your balance sheet. Instead, you will show the right to use that land. S.

Great explanation and much appreciated. I have a question though:

If the lease payments (on a lessees CF statement) appear under financing activities, doesn’t that impact Free-cashflows to the Firm and hence impact NPV, project IRR…etc?

If I’m not mistaken, the definition of Free-cashflows will have to be revised to include the lease payments as an operating outflow.

Hi Silvia,

One small detail, I was wondering if the right of use asset could go under current assets, for example the amount of lease liability that is due in the next 12 months. Can I account this amount as a current asset? I am asking because of performance ratios, such as current assets/current liabilities, that may be impacted for the worse.

No, that’s under non-current assets if the lease term is longer than 1 year. S.

Thank you. Well explained.

As per IAS 17, We have recognized advance payment lease as an non current asset and lease rent equivocations (deferred lease rent. What are the effects under IFRS 16 for above two balances?

Hai Silvia,

I have this issue on Operating lease on the book entries for lease premium paid in advance.

1. Do we amortize the lease premium over the period of the lease agreement?

2. Or do we expense the total lease premium to P&L?

Many thanks,

Andrew

Hi, you should amortize it, because it’s a prepayment. S.

Hai Silvia, many thanks. Cheers. Andrew

Hi Silvia,

Your explanation and illustration is very simple and easy to understand. Appreciate your efforts in making it simple for users. I take it that under IFRS16, both lease and asset will be classified as long term assets since it will over 12 months anyways. Thanks again.

Hi Silvia,

I would like to seek your view on revenue recognition – operating lease rental on investment properties.

I have a tenancy agreement with a lessee at monthly rent of $10,000, payable in advance on the 1st day of each month, for 24 months from 1 January 2016 to 31 December 2018. The tenant has been paying rent promptly from January to September 2016. However, the tenant did not pay the rental from 1 October to December 2016 but continue to occupy the premises. The tenant has moved out in January 2017.

My question is it appropriate to recognise the rental income from October to December 2016 ($30,000) and then make full allowance for the rental receivable?.

Thank you.

Kelvin

Hi Silvia:

I must commend your simple writing style devoid of all confusing technical jargons!

I was sondering if you have any plans to write on the IFRS16 disclosure requirements – or if you can explains the same briefly here.

Thanks in advance for your response!

Really a nice article and very informative, keep up the good work.

You are truly helping the students.

Dear Silvia, Thank you for the brilliant easily understandable article on IFRS 16. I have a question on Lessor Accounting. While the lessor continues to classify leases as under IAS 17 (Operating of Finance) the lessee is required by IFRS 16 to recognize an asset (provided that all conditions are met). There is a little confusion, if the lesser identifies an asset as a finance lease (and therefore the asset remains in its accounts) and the lessee has identified the same asset as a right-to-use asset, will there not be the case where the same asset is recognized twice (once in the lessee’s accounts and also in the lessors’ accounts)?

Hi Silvia,

Thank you so much for the awesome job on these new IFRSs.

I have a question on the calculation of the PV. How did you get CU23,341? when PV (8571×3, 3 yrs @ 5% I am getting CU22,211.86.

Thanks

Hmhmhm, how are you getting CU 22 211,86? 🙂

PV = 8571*1/1,05+8571*1/(1,05*1,05)+8571*1/(1,05*1,05*1,05)

Dear Silvia,

Thank you for your detail explanation in an understandable way. I am bit confused by your point that is, IFRS16 does not affect Lessors books, however i need to clarify following points:

a. Whether separation of elements is applicable for both lessor and lessee?

b. How to ensure the element cost is fairly measured comparing to market prices?

c. Should I consider a one year contract with non-cancellable period of two months with option to continue/terminate as lease contract?

d. All the leases will be in one line item in SFP?

Please reply

Thank you

Hi Silvia,

How would I account for leases of land with a life of 99 years? Debit Right of use of asset discounted at 99 years? This would be impractical and surely the rental value will likely change at every 5-10 year period. Appreciate your view. Thanks.

Dear John,

yes, exactly as you write. Debit ROU asset Credit Lease liability, where ROU asset = all lease payments in 99 years discounted to present value. And if there’s a change in payments, then you would need to account for the lease remeasurement. I covered all of this in my IFRS Kit with very detailed explanations. S.