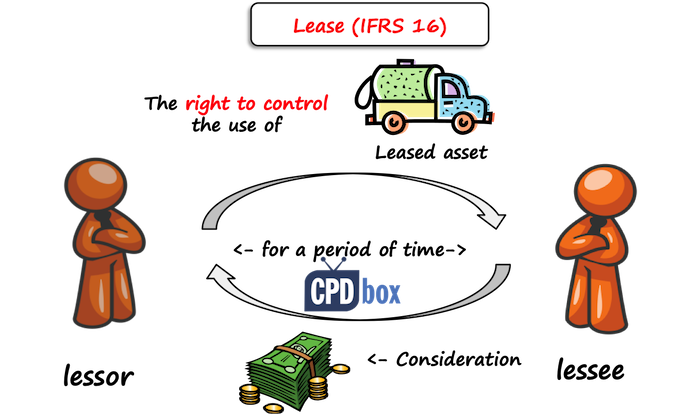

In January 2016, IASB issued another important and long-discussed standard: IFRS 16 Leases that will replace IAS 17.

Ever since then I receive lots of e-mails asking me to sum up what’s new.

OK, so here you go.

In this article, you’ll learn about the main changes that IFRS 16 introduces to the accounting for leases, illustrated on a very simple example.

Warning: this is NOT exhaustive description of the standard, and I simplify the things a lot for illustration purposes.

I will come back to it at the later stage, because I truly think that there will be lots of questions, discussions and additional guidance on how to tackle several areas of the lease accounting.

The effective date of the new IFRS 16 is 1 January 2019.

Why the new lease standard?

Short answer: To eliminate off-balance sheet financing.

Under IAS 17, lessees needed to classify the lease as either finance or operating.

If the lease was classified as operating, then the lessees did not show neither asset nor liability in their balance sheets – just the lease payments as an expense in profit or loss.

But, some operating leases were non-cancellable, and therefore, they represented a liability (and an asset) for the lessees.

This liability was hidden from the readers of the financial statements, as it was not presented anywhere.

Oh yes, some disclosures in the notes to the financial statements were mandatory, but frankly – who, except for auditors, ever reads the notes to the financial statements?

New IFRS 16 removes this discrepancy and puts most leases on balance sheet.

I’ll show you how in the next paragraphs.

Let’s see what has changed

Is it a lease?

The new IFRS 16 introduces a new definition of a lease. However, it is very similar to the old definition in older IAS 17 (differences do exist).

It means that when you actually accounted for some contracts as for lease contracts under IAS 17 Leases, you will continue to do so also under the new standard (careful, methodology may change).

BUT!!!

You have to be extremely careful when it comes to some service contracts.

Why?

Because, the new standard IFRS 16 provides a detailed guidance to determine whether your contract is a lease contract or a service contract (non-lease contract).

Under old IAS 17, it did not matter so much whether you have an operating lease contract or a service contract, for a very simple reason: you probably accounted for both types of contracts in the same way (that is, as a simple expense in profit or loss).

However, as the accounting for some types of previously-called operating lease contracts dramatically changes, we need to distinguish whether we have a lease under IFRS 16 or some other service contract under different standard.

As a simple illustration, let me come up with a small example:

- You will occupy a certain area of XY cubic meters, but the specific place will be determined by the owner of the warehouse, based on actual usage of the warehouse and free storage.

- You will occupy the unit n. 13 of XY cubic meters in the sector A of that warehouse. This place is assigned to you and no one can change it during the duration of the contract.

Both contracts look like lease contracts, and indeed, in both cases, you would book the rental payments an expense in profit or loss under older IAS 17.

Under new IFRS 16, you need to assess whether these contracts contain lease as defined in IFRS 16.

The first thing you would look at is whether an underlying asset can be identified.

Long story short:

- The first contract does not contain any lease, because no asset can be identified.

The reason is that the supplier (warehouse owner) can exchange one place for another and you lease only certain capacity. Therefore, you would account for rental payments as for expenses in profit or loss. - The second contract does contain a lease, because an underlying asset can be identified– you are leasing the unit n. 13 of XY cubic meters in the sector A.

Therefore, you need to account for this contract as for the lease and it means recognizing some asset and a liability in your balance sheet.

This was a very simplified illustration to make you aware of this and it’s by no means exhaustive – but you get a point.

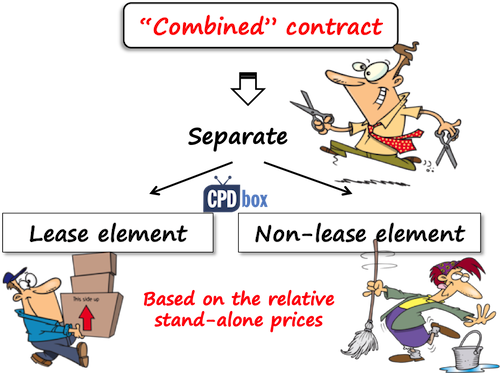

Do we pay only for a lease, or also for some services?

This is another change we need to watch out under IFRS 16.

When you lease some assets under operating lease (as called by older IAS 17), in most cases, a lessor provides certain services to you, such as maintenance, repairs, cleaning, etc.

Under older IAS 17, you did not need to think about it too much, because you put all lease payments as some rental expense to your profit or loss.

BUT!!!

Under new IFRS 16, you need to split the rental or lease payments into lease element and non-lease element, because you need to:

- Account for a lease element as for a lease under IFRS 16 (if it meets the criteria in IFRS 16); and

- Account for a service element as before, in most cases as an expense in profit or loss.

From our example above: let’s say you took the option 2 and you pay CU 10 000 per year. This payment includes the payment for rental of the unit n. 13 and its cleaning once per week.

Therefore, you need to split the payment of CU 10 000 into lease element and cleaning element based on their relative stand-alone selling prices (i.e. for similar contracts when got separately).

You find out that you would be able to rent out similar unit in the warehouse next door for CU 9 000 per year without cleaning service, and you would need to pay CU 1 500 per year for its cleaning.

Based on this, you need to:

- Allocate CU 8 571 (CU 9 000/(CU 9 000+CU 1 500)) to the lease element and account for that as for the lease; and

- Allocate CU 1 429 (CU 1 500/(CU 9 000+CU 1 500)) to the service element and in this case, probably recognize it in profit or loss as an expense for cleaning.

Not an easy thing, especially when the stand-alone selling prices are not readily available.

The biggest change: lessee’s accounting for leases

Here’s the biggest change: lessees (those who take an asset under lease) do not need to classify the lease at its inception and determine whether it’s finance or operating.

You might say: OH YES!!!

But not so fast.

The reason is that IFRS 16 prescribes a single model of accounting for every lease for the lessees. Very shortly:

- Lessee needs to recognize a right-of-use asset and corresponding liability in its statement of financial position.

- An asset shall be depreciated and a liability amortized over the lease term.

This model is very similar to the accounting for finance leases under IAS 17.

And yes, you need to account for operating leases in the same way.

There are 2 exceptions from this rule:

- Lease of assets for less than 12 months (short-term leases), and

- Lease of assets of a low value (such as computers, furniture etc.).

Example IAS 17 vs. IFRS 16

Let me illustrate the new accounting model and put it in the contract with the treatment under IAS 17.

I will continue in the above example of a warehouse. To make it quick, I will just make up some data:

- Annual rental payments are CU 10 000, including the cleaning services, all payable in arrears (at the end of year)

- Appropriate discount rate is 5%

- The lease term is 3 years.

How would you account for this contract under IAS 17 and IFRS 16?

Accounting under IAS 17 Leases

Under IAS 17, you need to classify the lease first.

Let’s say that based on warehouse’s economic life, lease payments, etc. you assess that this lease is operating.

Therefore, accounting is very simple:

- At the commencement, you do nothing;

- At the end of each year, you simply book the rental expense of CU 10 000 in profit or loss.

Accounting under IFRS 16

Here, no classification is necessary as one accounting model applies to all leases.

You need to follow 3 steps:

- Is it a lease under IFRS 16?

Yes, here it probably is. Please see the explanation above.

- Is there some element other than lease element? Do we need to separate?

Yes, we need to separate the cleaning element from the lease element. We did it above:

- CU 8 571 relates to the lease element;

- CU 1 429 relates to the cleaning element.

- How to we recognize these elements?

- At the commencement:

- You need to recognize right to use a warehouse in the amount equal to the lease liability plus some other items like initial direct costs.

- The lease liability is calculated at present value of lease payments over the lease term. In this case you need to calculate the present value of 3 payments of CU 8 571 (only lease element) at 5%, which is CU 23 341.

- Accounting entry is then

-

Debit Right-of-use asset: EUR 23 341

-

Credit Lease Liability: EUR 23 341

-

- Subsequently, when you make a payment and/or at the end of reporting period, you need to:

- Recognize depreciation of the right-of-use asset over the lease term, in this case CU 7 780 (CU 23 341/3) per year (I took straight-line depreciation);

- Recognize remeasurement of the lease liability to include interest, exclude amounts paid and take any lease modifications into account.

- At the commencement:

This simple table illustrates our example:

| Year | Lease liability b/f | Add interest at 5% | Less amounts paid | Lease liability c/f |

| 1 | 23 341 | 1 167 | – 8 571 | 15 937 |

| 2 | 15 937 | 797 | – 8 571 | 8 163 |

| 3 | 8 163 | 408 | – 8 571 | 0 |

| Total | n/a | 2 372 | – 25 713 | n/a |

Note: “b/f” means “brought forward (at the beginning of the year)”, “c/f” means “carried forward (at the end of the year)”.

Summary of accounting entries under IFRS 16:

| When | What | How much | Debit | Credit |

| At the commencement | Right-of-use asset + lease liability | 23 341 | Right-of-use asset | Lease liability |

| At the end of the year 1 | Interest | 1 167 | P/L: Interest expense | Lease liability |

| Rental payment | 10 000 | Cash (bank account) | ||

| 8 571 | Lease liability | |||

| 1 429 | P/L: Expenses for cleaning services | |||

| Depreciation | 7 780 | P/L: Depreciation | Right-of-use asset | |

Now, let’s compare.

Under IAS 17, the impact on profit or loss in the year 1 was CU 10 000, as we recognized the full rental payment in profit or loss.

Under IFRS 16, the impact on profit or loss in the year 1 was:

- Interest of CU 1 167, plus

- Depreciation of CU 7 780, plus

- Expense for cleaning services of CU 1 429.

- TOTAL of CU 10 376.

Hmmm, that’s actually more expenses in the first year under IFRS 16 than under IAS 17, isn’t it?

The reason is that thanks to the new model, the pattern of expenses has changed: we have loads of interest in the beginning of the lease, but smaller expenses at the end of the lease when the lease liability is amortized.

In total, both models have the same profit or loss impact over total lease term:

| Type of expense | IAS 17 | IFRS 16 | Note |

| Rental expense | 30 000 | – | 3*10 000 |

| Interest expense | – | 2 372 | Table above |

| Depreciation | – | 23 341 | 3*7 780 |

| Cleaning expenses | – | 4 287 | 3*1 429 |

| Total | 30 000 | 30 000 | |

Note: I am showing the cleaning expenses, too in order to show total impact of the whole contract, although technically they are not part of the lease accounting.

Also, under IFRS 16, we show more assets on the balance sheet, but also more debt or liabilities.

Please note that the cash flow does not change. You pay still the same amounts whether you apply IAS 17 or IFRS 16.

What about Lessors and accounting for leases under IFRS 16?

Good news, folks!

Accounting for leases by lessors almost does not change, so they can continue in the same way.

That’s all I need to say about it.

Final warning

The new lease standard will have significant impact on the companies heavily working with operating leases, no questions about it.

The financial indicators of these companies can substantially change, because new assets and liabilities are coming to the balance sheet.

Also, many lessees will have a hard time to set up a system of gathering and analyzing enough information to satisfy new requirements.

I will stop here, as this post is longer than I expected, but if you have some ideas or remarks on whether and how the new standard can affect your company, please let us know below in the comments. Thank you!