When to recognize revenue? This simple question is one of the most controversial issues in today’s accounting.

Why?

Well, it’s simple and easy when you sell goods, but how about long-term contracts or some sort of services?

You need to have some rules on WHEN to recognize the revenue from all these things, because all your profits and losses, your reputation in front of the outside world and your taxes depend on this.

Revenue recognition rules have just changed and later in this article, you’ll find an example showing you the impact of this change.

Revenue Recognition: IFRS vs. US GAAP

Until now, revenue recognition was exactly one of the biggest gaps between IFRS and US GAAP.

As you know, IAS 18 Revenue contains principles for revenue recognition, but they are quite broad and as a result, many companies use their judgment to apply them in their specific situation. Some companies even developed their own IFRS policies based on the US GAAP rules.

Opposed to IFRS, US GAAP guidance about revenues is very detailed – US GAAP contains about 100 separate documents and protocols about revenue recognition in specific areas (often conflicting, by the way).

Finally, these 2 standards came closer and tried to solve all these differences on 28 May 2014.

IFRS 15 Revenue from Contracts with Customers

New revenue recognition standard was issued: IFRS 15 Revenue from Contracts with Customers and it should fill the gap between IFRS and US GAAP.

FASB (the US GAAP standard setting body) issued the new revenue recognition standard, too: Topic 606, which is almost a mirror of IFRS 15 (full text of Topic 606 is here).

Although I’ll cover this standard in one of my videos in the following months, here are the basic points for your information:

-

- You’ll need to apply IFRS 15 for reporting periods beginning on or after 1 January 2018 (early application permitted);

- IFRS 15 will replace the following standards and interpretations:

- IAS 18 Revenue,

- IAS 11 Construction Contracts

- SIC 31 Revenue – Barter Transaction Involving Advertising Services

- IFRIC 13 Customer Loyalty Programs

- IFRIC 15 Agreements for the Construction of Real Estate and

- IFRIC 18 Transfer of Assets from Customers

- The core principle of IFRS 15 is that an entity will recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration (payment) to which the entity expects to be entitled in exchange for those goods or services.

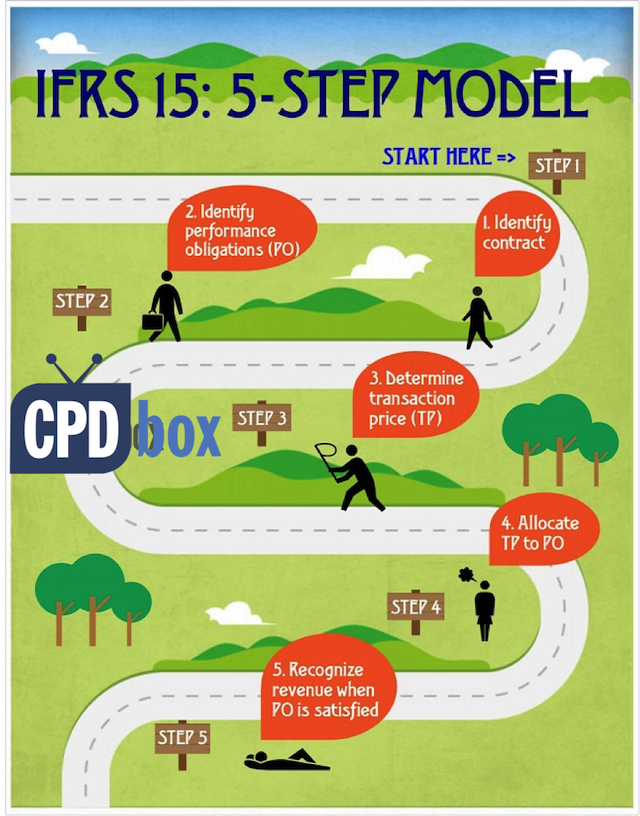

To apply this principle, you need to follow a five-step model framework described below.

- IFRS 15 contains guidance for transactions not previously addressed (service revenue, contract modifications);

- IFRS 15 improves guidance for multiple-element arrangements;

- IFRS 15 requires enhanced disclosures about revenue.

Five-Step Model Framework

Every company must follow the five-step model in order to comply with IFRS 15. We’ll not go into details, just let me brief you a bit:

- Step 1: Identify the contract(s) with a customer.

IFRS 15 defines a contract as an agreement between two or more parties that creates enforceable rights and obligations and sets out the criteria for every contract that must be met.

- Step 2: Identify the performance obligations in the contract.

A performance obligation is a promise in a contract with a customer to transfer a good or service to the customer.

- Step 3: Determine the transaction price.

The transaction price is the amount of consideration (for example, payment) to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties.

- Step 4: Allocate the transaction price to the performance obligations in the contract. For a contract that has more than one performance obligation, an entity should allocate the transaction price to each performance obligation in an amount that depicts the amount of consideration to which the entity expects to be entitled in exchange for satisfying each performance obligation.

- Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation.

Who Will Feel the Biggest Impact of IFRS 15?

The experts say that the most impacted industries are telecom, software development, real estate and other industries with long-term contracts.

If you work in an industry where bundled contracts of “product + service” are quite common, then you should pay attention.

I’m referring mainly to software development or telecommunications, where customers usually buy a prepayment plans with a handset or software development comes with implementation and post-delivery service in 1 package, or any similar arrangements.

Under the new model, companies in telecom and software will probably recognize revenue earlier than under older rules.

Why is that?

Well, because under new IFRS 15, the transaction price must be allocated to the individual performance obligations in the contract and recognized when these obligations are delivered or fulfilled.

It means that under new IFRS 15, telecom operator must allocate a part of the revenue from prepayment plan with free handset to the sale of handset, too.

Under IAS 18, the revenue is defined as a gross inflow of economic benefits arising from ordinary operating activities of an entity.

It means that if the operator gives a handset for free with the prepayment plan, then the revenue from handset is 0.

OK, if that sounds a bit confusing, we’ll better look at numbers.

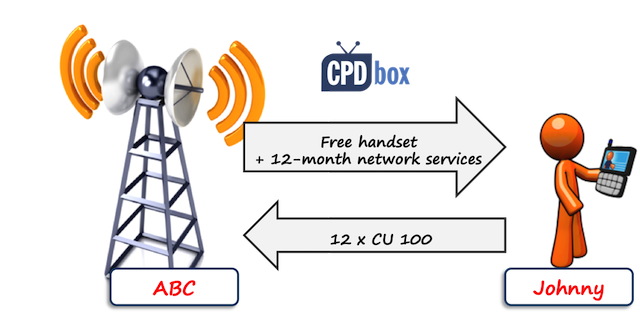

Example: IAS 18 vs. IFRS 15

Johnny enters into a 12-month telecom plan with the local mobile operator ABC. The terms of plan are as follows:

- Johnny’s monthly fixed fee is CU 100.

- Johnny receives a free handset at the inception of the plan.

ABC sells the same handsets for CU 300 and the same monthly prepayment plans without handset for CU 80/month.

How should ABC recognize the revenues from this plan in line with IAS 18 and IFRS 15?

OK, let’s ignore a couple of things here, like a price of a SIM kit, or the situations when Johnny hangs on the phone for hours and spends some minutes in excess of his plan. Let’s focus just on these 2 things.

Revenue under IAS 18

Current rules of IAS 18 say that ABC should apply the recognition criteria to the separately identifiable components of a single transaction (here: handset + monthly plan).

However, IAS 18 does not give any guidance on how to identify these components and how to allocate selling price and as a result, there were different practices applied.

For example, telecom companies recognized revenue from the sale of monthly plans in full as the service was provided, and no revenue for handset – they treated the cost of handset as the cost of acquiring the customer.

Some companies identified these components, but then limited the revenue allocated to the sale of handset to the amount received from customer (zero in this case). This is a certain form of a residual method (based on US GAAP’s cash cap method).

For the simplicity, let’s assume that ABC recognizes no revenue from the sale of handset, because ABC gives it away for free. The cost of handset is recognized to profit or loss and effectively, ABC treats that as a cost of acquiring new customer.

Revenue from monthly plan is recognized on a monthly basis. The journal entry is to debit receivables or cash and credit revenues with CU 100.

Revenue under IFRS 15

Under new rules in IFRS 15, ABC needs to identify the contract first (step 1), which is obvious here as there’s a clear 12-month plan with Johnny.

Then, ABC needs to identify all performance obligations from the contract with Johnny (step 2 in a 5-step model):

-

-

- Obligation to deliver a handset

- Obligation to deliver network services over 1 year

-

The transaction price (step 3) is CU 1 200, calculated as monthly fee of CU 100 times 12 months.

Now, ABC needs to allocate that transaction price of CU 1 200 to individual performance obligations under the contract based on their relative stand-alone selling prices (or their estimates) – this is step 4.

I made it really simple for you here, so let’s do it in the following table:

| Performance obligation | Stand-alone selling price |

% on total | Revenue (=relative selling price = 1 200*%) |

| Handset | 300.00 | 23.8% | 285.60 |

| Network services | 960.00 (=80*12) | 76.2% | 914.40 |

| Total | 1 260.00 | 100.0% | 1 200.00 |

The step 5 is to recognize the revenue when ABC satisfies the performance obligations. Therefore:

-

-

- When ABC gives a handset to Johnny, it needs to recognize the revenue of CU 285.60;

- When ABC provides network services to Johnny, it needs to recognize the total revenue of CU 914.40. It’s practical to do it once per month as the billing happens.

-

The journal entries are summarized in the following table:

| Description | Amount | Debit | Credit | When |

| 285.60 | FP – Unbilled revenue | P/L – Revenue from sale of goods | When handset is given to Johnny | |

| Network services | 100.00 (= monthly billing to Johnny) | FP – Receivable to Johnny | When network services are provided; on a monthly basis according to contract with Johnny | |

| 76.20 (=914.40/12) | P/L – Revenue from network services | |||

| 23.80 (=285.60/12) | FP – Unbilled revenue | |||

So as you can see, Johnny effectively pays not only for network services, but also for his handset.

What’s the Impact of the IFRS 15?

The biggest impact of the new standard is that the companies will report profits in a different way and profit reporting patterns will change.

In our telecom example, ABC reported loss in the beginning of the contract and then steady profits under IAS 18, because they recognized the revenue in line with the invoicing to customers.

Under IFRS 15, ABC’s reported profits are the same in total, but their pattern over time is different.

Why does it matter?

Well, because some contracts surpass one accounting period. They are long-term and reporting revenues in incorrect accounting periods might cause wrong taxation, different reporting to stock exchange and other things, too.

Don’t believe me?

Just look at ABC. Let’s say that contract started on 1 July 20X1 and ABC’s financial year-end is 31 December 20X1. Just look how much profits ABC reports from the same contract with Johnny under IAS 18 and IFRS 15 in the year 20X1:

| Performance obligation | Under IAS 18 | Under IFRS 15 |

| Handset | 0.00 | 285.60 |

| Network services | 600.00 (=100*6) | 457.20 (=76.2*6) |

| Total | 600.00 | 742.80 |

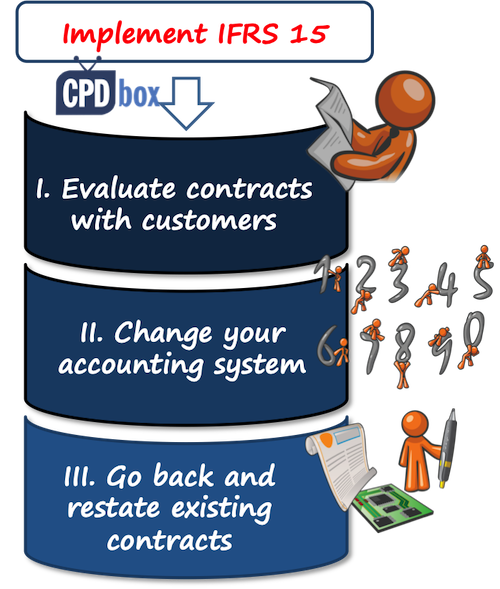

How to Prepare for IFRS 15

I really do think that IFRS 15 is a huge change and it requires a massive amount of work not only from accountants, but also from IT departments, tax people and maybe other departments in your company, too.

A few ideas for your future steps:

- Go through your contracts and evaluate

Your profit reporting will depend on the specific contract terms. If your company has a number of different types of contracts, you need to assess each type separately and decide how to deal with that type in line with IFRS 15.

- Change your accounting system

OK, how many customers does the “average” telecom company have?How many contracts are there?

Thousands. Millions. Tens of millions.

And once you decide how to recognize revenue for each type of contract that you have, then you need to implement this accounting process into your accounting software or system.

Whether you realize it or not, the implementation of IFRS 15 will cost affected companies significant amount of money for system upgrades, consultants, training the employees and other related activities.

That’s why IFRS 15 must be implemented starting 1 January 2018 – some time is left for making these changes.

- Go back and restate existing contracts

I did not want to scare you in my previous point, but this is going to be a bit scary:All companies need to look back and recalculate profits and revenue reporting from all contracts.

When you apply IFRS 15, you need to apply it as the new rules have always been in place, that is retrospectively.

Let’s say that Johnny and ABC enter into 2-year plan on 1 July 2015 and IFRS 15 has not applied yet; thus ABC recognized zero revenue for handset and monthly revenues from network services in line with the billing.

On 1 January 2017, ABC will apply IFRS 15 and contract with Johnny is still open (it expires on 30 June 2017). ABC needs to perform all the calculations as shown above and adjust opening balances related to the contract.

What does it mean?

Companies will need to gather lots of numbers, fair values, estimates, stand-alone selling prices and other things and then perform lots of recalculations and adjustments.

Just imagine you work in a construction of real estate and you’re affected by IFRS 15. Some contracts run for 10 or 15 years … OK, I finish here and leave it to your imagination.

UPDATE 2018: I have written few articles about IFRS 15 and you can check them out here:

- IFRS 15 Examples: How IFRS 15 affects your company

- Accounting for discounts under IFRS

- How to account for customer incentives under IFRS

- Principal or agent – revenue or liability?

- Short summary of IFRS 15 Revenue from Contracts with Customers (with video)

Now, I’d really love to hear your view. Do you think IFRS 15 will hit you hard? Are you making your plans to adopt or implement it? Please leave a comment below and if you liked reading this article, share it with your friends here.