IFRS 10 Consolidated Financial Statements

In my previous article I introduced the world of group accounts and consolidation to you.

You learned that there about 6 IFRS dealing with this topic.

Here, I’d like to summarize the first “consolidation” standard dealing with the consolidated financial statements: IFRS 10.

What is the objective of IFRS 10?

The objective of IFRS 10 Consolidated Financial Statements is to establish principles for the presentation and preparation of consolidated financial statements when an entity controls another entity.

More specifically, IFRS 10:

- Requires an entity (a parent) that controls one or more other entities (subsidiaries) to present consolidated financial statements;

- Defines the principle of control as the basis for consolidation and sets out how to identify whether the investor controls the investee;

- Sets out the accounting requirements for the preparation of consolidated financial statements, and

- Defines an investment entity and sets out an exception to consolidating particular subsidiaries of an investment entity.

Control as the basis for consolidation

Simply speaking, the basic rule is:

- If an investor controls its investee => investor must consolidate;

- If an investor does NOT control its investee =>; investor does NOT consolidate.

So what is control?

An investor controls an investee when the investor:

- Is exposed to, or has right to variable returns from its involvement with the investee;

- Has the ability to affect those returns

- Through its power over the investee.

How to assess control

Remember 3 basic elements inherent in control: power, ability to use this power and variable returns.

Power is the existing rights that give the current ability to direct the relevant activities. Let’s break it down a bit:

- The rights must be substantive, not only some minor rights;

- The ability must be current, exercisable in the present time;

- The relevant activities must be significant and related to major activities of investee.

When assessing whether an investor controls an investee, more than one factor need to be considered. IFRS 10 contains guidance in this area.

Accounting requirements of IFRS 10

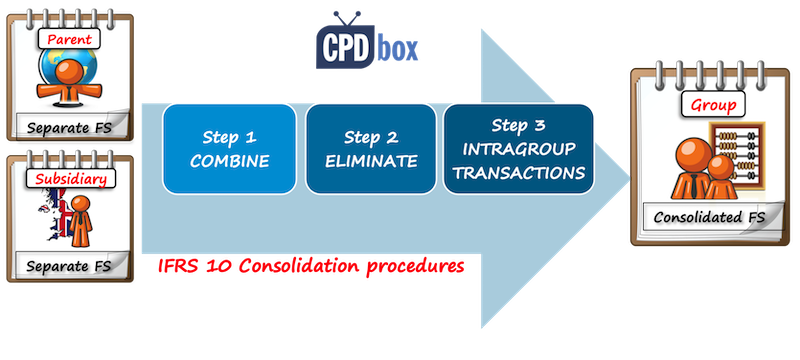

Consolidation procedures

In order to prepare consolidated financial statements, IFRS 10 prescribes the following consolidation procedures:

- Combine like items of assets, liabilities, equity, income, expenses and cash flows of the parent with those of its subsidiaries;

- Offset (eliminate):

- The carrying amount of the parent’s investment in each subsidiary; and

- The parent’s portion of equity of each subsidiary;

- Eliminate in full intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between entities of the group.

If you’d like to learn HOW to actually apply these consolidation procedures and how to prepare the consolidated financial statements on numerical examples, please check out the IFRS Kit.

Other accounting requirements

Except for basic consolidation procedures, IFRS 10 prescribes number of other rules for preparing consolidated financial statements, such as:

- Presentation of non-controlling interests: in equity, but separately from the equity of owners of the parent;

- Uniform accounting policies shall be used by both parent and subsidiary;

- The financial statements of the parent and the subsidiary shall have the same reporting date;

- How to deal when the parent loses its control over subsidiary,

and number of other rules dealing with the specific circumstances.

Exceptions in IFRS 10

As I wrote above, when a parent controls a subsidiary, then it should consolidate.

But not always. IFRS 10 sets the following exceptions from consolidation:

- A parent does not need to present consolidated financial statements if it meets all of the following conditions:

- It is a wholly-owned subsidiary or is a partially-owned subsidiary of another entity and its other owners agree;

- Its debt or equity instruments are not traded in a public market;

- It did not file, nor is it in the process of filing, its financial statements with a securities commission or other regulatory organization for the purpose of issuing any class of instruments in a public market, and

- Its ultimate or any intermediate parent of the parent produces consolidated financial statements available for public use that comply with IFRSs.

- Post-employment benefit plans or other long-term employee benefit plans to which IAS 19 Employee Benefits applies – they don’t need to present consolidated financial statements;

- Investment entities. This exception applies for the periods starting on or after 1 January 2014 and I have written about this exception in the article “Top 5 2013 and 2014 IFRS Changes“.

Investment entities

Investment entity is an entity that:

- Obtains funds from one or more investors for the purpose of providing those investor(s) with investment management services;

- Commits to its investor(s) that its business purpose is to invest funds solely for returns from capital appreciation, investment income, or both, and

- Measures and evaluates the performance of substantially all of its investments on a fair value basis.

IFRS 10 sets the guidance and rules about determining whether the entity is an investment entity or not. Typical characteristics of investment entities are:

- It has more than one investment;

- It has more than one investor;

- It has investors that are not related parties of the entity;

- It has ownership interests in the form of equity or similar interests.

Most investment entities CANNOT present consolidated financial statements and instead, they need to measure an investment in a subsidiary at fair value through profit or loss in line with IFRS 9 Financial Instruments.

Please watch the following video with the summary of IFRS 10:

If you like this summary, please let me know by leaving a comment right below. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

104 Comments

Leave a Reply

In consolidated financial statements parent company show Goodwill not in separate financial statements.

Dear Silvia,

Is there any possibility either in IFRS03/IAS27/IAS28 to show goodwill in the books of parent (standalone) financial statements

Hi Silvia,

I request you to send me IFRS 10 PDF material or provide the link to download it.

Well, we don’t do this, sorry.

what happens if a parent entity does not prepare consolidated financial statements and none of the exemptions apply?

Well, that’s not an IFRS question – it depends on your legislation.

Hi Silvia,

Thank you for explaining complex matter so simply. My best wishes

Hi Silvia THANK YOU so much for your videos.I learned a lot and it helps me to understand easily Do you have a power point of your videos?

Hi Silvia;

Regarding Exceptions in IFRS 10

I don’t understand the relation of “Post-employment benefit plans or other long-term employee benefit plans” to consolidation exceptions. I know there is IAS 19 Employee Benefits.

This means any company has Post-employment benefit plans do not need to consolidate?

Thanks,,,

Yes. If you control post-employment benefit plan and that is, for example, separate legal entity, you do not need to consolidate that entity itself.

Thank you

And if the the plan is separete legal entity dealing with both post-employment and short term benefits (i.e. Heath care plan for current and former employees?

Hello Madam, I am an acciuntant of a Company. The companyinvested in a partnership firm. The firm incurred loss. How do I account for this loss in the company’s standalone financials. Investment is a non current trade investment. Please guide me.

It depends on what method of accounting for the investment in a partnership firm did the Company choose and also, how was the investment classified. You provided too few information to give you the answer.

Dear Silvia,

Company A acquire 20% shareholding in Company B. Next three investors holds 22% shareholding in Company B and remaining 58% shareholding belongs to Numerous shareholders with less than 1% each.

Whether Company A establish control which leads to consolidate financial statements if;

1) None of the shareholders have arrangements to consult each other or make collective decisions.

2)A shareholder agreement grants the largest investor the right to take operational decisions of regular matter.

Thanks

This is very useful.

I have small doubt.

company A owns 100% of Company B, Company B owns 100% of Company C.

Can company B present consolidated Financial statement ?

Yes, of course, B can present the financial statements, however, it can qualify for exemption, because if A as ultimate parent presents IFRS financial statements and other conditions apply, then B does not need to.

I have a question. What if a Bank incorporate an insurance Company holding minor shareholdings, whereas major shareholdings are by related parties of the Bank. In that case, whether:

1. Insurance company will constitute a subsidiary of the Bank?

2. Bank has direct/indirect control over Insurance Company?

3. Should Bank consolidate the Insurance Company or whether is it exempted from consolidation?

Regards

Dear Asha,

I really can’t answer that question based on the information you wrote me. First of all – the size of the share does NOT matter. CONTROL matters. The bank can exercise control over the insurance company while having 0% share. So please answer the question – does the bank have control over the insurance company? If yes, then the bank has subsidiary and needs to consolidate. S.

Hi Silvia.

Thank You for such a lovely article.

Could you please guide me on accounting entries on sale of Non-Current Assets by parent to subsidiary and vice versa on consolidation?

Thank You. 🙂

Hi Kishan, I solve these transactions in my IFRS Kit, very nicely illustrated and shown in Excel file 🙂 Kind regards S.

Respected Silvia

I am very curious to know that how De-facto Consolidation model works and whether such kind of company exists in reality which consolidate on a De -facto control basis because it is very difficult to judge the control on a de-facto basis.

Dear Silvia,

During the previous years, the subsidiary was not operational and did not prepare financial statements, the parent company issued normal financial statements with a note that it did not consolidate the said subsidiary. Now tge subsidiary is operational and have prepared financials including that of previous year with material balances. Now the issue is if the parent wants to consolidate its subsidiary in the current year, how will it deal with the corresponding figures?. Really appreciate your guidance.

If holding company is revaluing its one of the assets class eg. Plant and Machinery under IAS 16, does subsidiary shall also revalue its assets.

Would appropriate your quick response.

Thanks

Prashaant Lunawatt

Hi Prashaant,

yes, if you consolidate, all consolidated companies should apply the same accounting policies. S.

Thank you for the wonderful presentation of ifrs.

Hi Silvia.

Can you please guide me whether IFRS 10 will apply of IFRS 11.

There is a joint arrangement which is created solely for the benefit of one of the two shareholders. One of the shareholders has the expertise in technology and other will get all the production. The contribution, BOD voting power and profits is 50:50. Further, one can not make the decision without the consent of the other.

However, all the production goes to one of the shareholders.

Will this be joint operation or consolidated under IFRS 10?

Also is there further guidance on variable interest entity?

Hello Silvia,

I have a question relating to disposal of Wholly owned subsidiary (and same is disposed of in full).

Questions are: Group yearend 31.12.2014 in the year 2014 at the end of April, (30.04.2014) Parent company decided to sell 100% shareholding of the subsidiary at book value as at 30.04.2014. How we will prepare consolidation statement at the yearend 31.12.2014

Is it necessary to consolidate account of disposal subsidiary in CFS till April, 14?

Or

Only 4 months’ profit of discontinued operation profit be reported in CFS?

Entry in parent books is simple as an investment accounted at cost value. So, profit will be (Net Value of Disposal – Cost value of Investment in Parent Book).

Cash/Bank …DR

Investment in Sub. Ac …Cr

Profit on disposal of investment A/c …Cr

As parent company decided to disposed of subsidiary at book value as at 30.04.2014, So what will be the entry to be posted in CFS, after considering above two question whichever is applicable, considering fact that profit on disposal of Investment already included in Parent Profit and loss account, whereas in Consolidation opening retained earning balance reflect profit of subsidiary till 31.12.2013 (that is in CFS profit of subsidiary for the year and non-distributed profit lying in retained earnings of Group CFS till 31.12.2013)

Waiting for your reply.! Many Thanks.

Regards/VM

Hi Volten, I recommend checking this article about changes in the group. Hope this helps and if still unclear, please give me the comment below that article. Thanks! S.

Hi Silvia

Do you have any article as to how to consolidate and account for complex groups featuring sub-subsidiaries,joint venture and associates where a parent entity has asubsidiary,joint venture and associate without directly owning shares in it.

Will appreciate for information on this .

Thanking you

Sonam Choeden

Bhutan

Hi Sonam, no, sorry, not yet. I’ll work something out in the future. S.

HI Sylvia – is there a definition or guidance as regards ‘available for public use” ?

I am preparing group AFS at an ultimate parent level however using IFRS10 4a exemption not to prepare consolidated AFS at each parent / holding co level in the group.

We are a private company in South Africa with ultimate shareholding in PRC who dont prepare IFRS AFS.

grateful for your assistance

Dear Silvia,

Is an associate consolidated?And if so, can it be considered a constituent entity?

Thanks a lot!

OLga

Hi Olga,

for an associate, you do NOT apply the full consolidation method as described in IFRS 10, but the equity method under IAS 28. S.

Hi, Silvia

This has helped me a lot in preparing a CPA exam.

Thank you for your time and efforts in making such great contents.

Have a great day 🙂

Glad to help 🙂

Hi, Silvia

Thank you for your great article! It was useful for me!

I have a question. We should prepare Consolidated Financial Statement. Parent company uses revaluation model for PPE but its subsidiary uses cost model. When we combine all PPE, it might be unfair. Pls, give me some advices. I need your help…

Hi Mirolim,

both parent and subsidiary need to use the same accounting policies for the consolidated financial statements. Therefore, you need to adjust subsidiary’s financial statements first – it means that you need to apply revaluation model for PPE for the purposes of consolidation and only then consolidate.

Hope this helps

S.

Hi Silvia,

I have a question about the equity method, how can I apply it if I need to close my accounts before the investee, I mean investee didnt report his income yet, and I need to audit my financial statements as soon as possible,

should I apply equity method when investee is not reporting financial statements publicaly?

Dear Silvia,

I hope you are doing well,

I had a case while preparing the consolidated Financial statements.

The baby company invoices the parent on a monthly basis, for services she provides. However, part of those invoices are capitalized related to work done on an asset (software underdevelopment) owned by the parents. How should this be treated? Shall we eliminate the the revenue with the software?

Thank you Silvia,

Tamer

On a side note, the baby invoices the Parent with no profit, Just the cost she incurred.

Thanks

One more thing, the invoices represent the work done by the Baby company’s employee. their Salaries or part of the salaries.

Thanks

Hi Silvia,

First of all i want to thank you for your work, it brings benefits for all of us.

Tell me please, in the light of IFRS 10, it is possible for an investment entity, that doesn’t consolidate, to have the control of entities that aren’t consolidated?

Thanks!

Sorin,

yes, there is a exemption of investment entities from preparing consolidated financial statements, but there are conditions to be met first, e.g. investment entity measures its investments on a fair value basis, invests for the purpose of getting income on capital appreciation/dividends/both, etc. S.

Hi Silvia,

I studing for ACCA p2 but I do not have the skills in answering the industry questions, i.e. accounting treatment to the case study or how to treat any IFRS in a scenario question like brand, revenue recongnition, investmne property etc.

Or direct me to any of your aricles on your website.

Thanks.

David

Hi Silvia,

Thank you for the useful information.

I have a question. One of my subsidiaries is under members’ voluntary liquidation during the financial year. Is it correct to continue disclose this company as a subsidiary in the statement of financial position at year end? Or should I classify this company as Non-current asset held for disposal under current asset? How about compulsory winding up by creditors. I would have lost control once a liquidator is appointed.

How about associate?

Thank you

Hi Kelvin,

in your case, at the date control is lost, all subsidiary’s assets and liabilities are derecognized and you just keep any investment retained in the former subsidiary (i.e. stop consolidating and keep investment in 1 line). The Basis for Conclusion related to IFRS 5 says that. It also says that “being committed to a plan involving loss of control of a subsidiary should trigger classification as held for sale”. Hope it helps! S.

In case the promoters of the flagship company (46%) and the flagship company (51%) own and control 97% in a partnership firm, can the flagship company compile CFS as per IFRS 10 on line by line basis to the extent of 97% and balance 3% be shown under NCI?

Hi Silvia

As always thank you for your comments. My query is on point no 3 “Eliminate in full intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between entities of the group”.

In this connection how do i eliminate inter company transactions with following scenario.

Company A provides services to Company B worth of $100.

The transaction in the books of company A is,

Cash Dr 100

Income Cr 100

The transaction in the books of company B is,

Expense Dr 80

Asset Dr 20 (since of the $100 worth of service availed $ 20 was related to creation of assets)

Cash Cr 100

So i would appreciate if you could advise me what would be eliminated for the example above.

Thanking you

Sonam Choeden

DGPC

Bhutan

Dear Sonam,

very interesting question 🙂

From the group’s point of view, there was no external work on an asset, but the Group did it itself. Therefore, you should eliminate the entry in full, i.e. Debit Income 100, Credit Expense 80, Credit Asset 20.

However, there was some internal work done on your asset and therefore, you should capitalize the cost of internal employees (group’s employees) to the cost of an asset at the group’s level. You should do it at COST, not including any kind of a profit that might have been charged intragroup.

Let’s say the cost of employees doing the work was 18, so then you capitalize as Debit Asset 18, Credit Expenses for salaries (or as appropriate) 18.

Hope this helps, S.

Thanks Silvia and instead of eliminating from asset, could we eliminate Income Dr 100 and Expense Cr 100 (80+20) because for Group at the end of the day has to incur $ 20 for creation of assets . If company A had created that asset then $ 20 would have been charged to asset only.I hope i am making sense because i am still not exactly clear on this.

Sonam Choeden

DGPC

Bhutan

Sonam,

that’s not correct.

You should eliminate an asset, too and at the same time, you should capitalize internally incurred costs on that asset, just as I described in the above comment. S.

Though I am late, but question is so interested so jumped in.;

What if depreciation charged on the same at the rate of 10% assuming assets fully used by the company for 1 year. Depreciation charged for the yerar is 2.

How it will be eliminated ?

In the year 2, the asset’s carrying amount is 16 (cost of 20 less 2 years depr. of 2). You eliminate it as debit Accumulated profit 18 Credit P/L Depreciation charge 2 Credit Asset 16. The accumulated profit part comes from the adjustments made in previous year – they were made in profit or loss, but profit os loss went to accumulated profit this year. You must repeat the entry and then update it by depreciation charge in the current year. S.

we love you so much Silvia!You are a Star!

Reply

Wow. Never meant to be! But thank you, sometimes it’s good to read something absolutely flattering! 🙂

It is really usefull for professional accountants and students.

Very useful indeed!!

Hi, for companies with first year consolidation are they required to include and restate comparatives?

Hi Kayley,

yes, the comparatives are included, but there is nothing to restate, because in the previous period, there was no subsidiary or so. Therefore, in the consolidated FS:

– consolidated balance sheet in the current reporting period contains aggregated amounts of a parent and a subsidiary

– consolidated balance sheet in the previous reporting period contains just the amounts of a parent and no subsidiary. S.

Hi Kayley,

Can you tell me basis for the same. Can’t there be an argument that since there was no group in the earlier period comparative disclosure is not required.

This is a good work,it’s value added.Thank.

Dear Silvia,

I would like to check if the parent wholly owned subsidiary, so do not have NCI, what should I count for the goodwill?

Thank you.

Best Regards,

Wei Ping

Hi,

even when a parent acquires 100% share in a subsidiary, there can be some goodwill – basically, it’s a difference of what parent has paid for the share (fair value of consideration) and its share on the net assets of investee – but that’s not precise definition, please look above. Sure, when there’s 100% share, there’s no NCI. S.

Dear Silvia, Good day. I am senior lecturer in one of the college in Klang, Malaysia. I saw your notes and presentation and I wish to buy your IFRS kit. My accounts department needs an invoice so that they can prepare the payment. Can you email me the invoice so that they can process the payment.

TQ

Dear Sir, I have sent you an e-mail. S.

many thanks silvia you are helping me to understand

Thanks for your articles that helped to qualify. Pls, i want to do IFRS course online to have ‘IFRS Cert’. Pls, help! Thanks

Dear Ogunrinde,

thank you for your interest and comment.

There is a few of online IFRS courses, but it depends on the type of certificate you want to get.

If you would like to obtain a formal IFRS diploma, then I would recommend taking DipIFR exam with ACCA. For this exam, you can do online course (including my IFRS Kit).

If you’d like to get a certificate for your own CPD purposes, you can simply sign up for any online course that fits your needs and is relevant for you (again – including my IFRS Kit).

If you need further assistance, please write me an e-mail and I’ll get back to you.

Have a nice day!

Silvia

this is excellent

Great article and keep it up. Easy for beginners.

hi silvia i need ifrs 11 and ifrs 12 plz thank you

you are the best

I’ll come to that, don’t worry! 🙂 S.

Hi Silvia,

you are helping accounting people to understand the IFRS concept very easily. Thanks.

mam silvia,

write article on the new standard that has been included in this attempt of p2 IAS 41

I will, certainly 🙂 S.

This is very nice and useful materials for accountants. Its brief and easily understandable. Hope it could cover more ifrs in the future. Thank you so much miss silvia

Dear Silvia,

Thank you for the great job you are doing, i sincerely treasure your work and enjoy reading your articles on IFRS. Please kindly update me on the latest changes, I have only come across one in your notes (Investment entity exempted from consolidating). What are the rest.

Regards

Martin

Hi Martin, thank you for your feedback. Well, when there is a change, I always try to update relevant article. For example, when the newest revenue standard IFRS 15 was issued, I immediately wrote an article here: http://www.cpdbox.com/ifrs-15-vs-ias-18/

Also, when IFRS 9 was adopted, I updated my summary: http://www.cpdbox.com/ifrs-9-financial-instruments/

Once per year, I do wrap up of all significant changes made in the previous year. Kind regards, S.

we love you so much Silvia!You are a Star!

WOW 🙂

Hi Silvia,

I want to purchase membership to your website however the exchange rate for euro/rand in South Africa is 1:16.69 and I simply cannot afford that, could you please give me a third world discount as I would really use your content to advance my career.

Kind regards

Wojtek Sokolowski

Wojtek,

please contact me via contact form. Thank you! Silvia

very useful ,

Thanks for sharing. It is eaasier to understand by having such a good illustration.

Silvia,

Thanks for putting this together and for posting/sharing it. It explains the consolidation so simply.

This is a very useful website and I encourage all professuional Accountants to check it on.