These days people use about 180 currencies world wide!

The truth is that we, people, don’t want to stay isolated. We love to sell, buy, import, export, trade together and do many other things, all in foreign currencies!

When you look at the business world, you’ll see that business go global in two ways: they either have individual transactions in foreign currencies, or when they grow bigger, they often set up foreign operations (separate business abroad).

Moreover, the exchange rates change every minute. So how to bring a bit of organization into this currency mix-up? That’s why there is the standard IAS 21 The Effects of Changes in Foreign Exchange Rates.

What is the objective of IAS 21?

The objective of IAS 21 The Effects of Changes in Foreign Exchange Rates is to prescribe:

- How to include foreign currency transactions and foreign operations in the financial statements of an entity; and

- How to translate financial statements into a presentation currency.

In other words, IAS 21 answers 2 basic questions:

- What exchange rates shall we use?

- How to report gains or losses from foreign exchange rates in the financial statements?

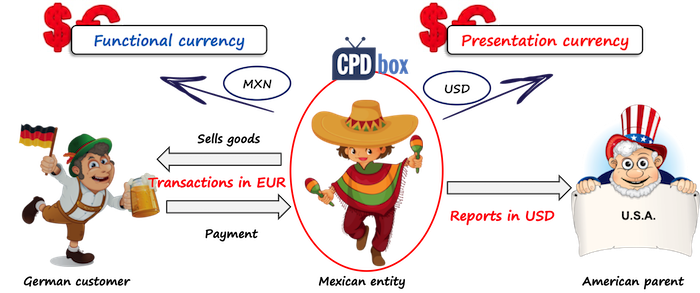

Functional vs. Presentation Currency

IAS 21 defines both functional and presentation currency and it’s crucial to understand the difference:

Functional currency is the currency of the primary economic environment in which the entity operates. It is the own entity’s currency and all other currencies are “foreign currencies”.

Presentation currency is the currency in which the financial statements are presented.

In most cases, functional and presentation currencies are the same.

Also, while an entity has only 1 functional currency, it can have 1 or more presentation currencies, if an entity decides to present its financial statements in more currencies.

You also need to realize that an entity can actually choose its presentation currency, but it CANNOT choose its functional currency. The functional currency needs to be determined by assessing several factors.

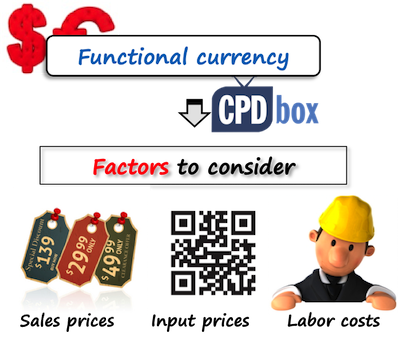

How to determine functional currency

The most important factor in determining the functional currency is the entity’s primary economic environment in which it operates. In most cases, it will be the country where an entity operates, but this is not necessarily true.

The primary economic environment is normally the one in which the entity primarily generates and expends the cash. The following factors can be considered:

- What currency does mainly influence sales prices for goods and services?

- In what currency are the labor, material and other costs denominated and settled?

- In what currency are funds from financing activities generated (loans, issued equity instruments)?

- And other factors, too.

Sometimes, sales prices, labor and material costs and other items might be denominated in various currencies and therefore, the functional currency is not obvious.

In this case, management must use its judgment to determine the functional currency that most faithfully represents the economic effects of the underlying transactions, events and conditions.

How to report transactions in Functional Currency

Initial recognition

Initially, all foreign currency transactions shall be translated to functional currency by applying the spot exchange rate between the functional currency and the foreign currency at the date of the transaction.

The date of transaction is the date when the conditions for the initial recognition of an asset or liability are met in line with IFRS.

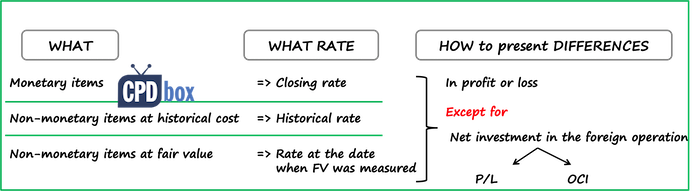

Subsequent reporting

Subsequently, at the end of each reporting period, you should translate:

- All monetary items in foreign currency using the closing rate;

- All non-monetary items measured in terms of historical cost using the exchange rate at the date of transaction (historical rate);

- All non-monetary items measured at fair value using the exchange rate at the date when the fair value was measured.

How to report foreign exchange differences

All exchange rate differences shall be recognized in profit or loss, with the following exceptions:

- Exchange rate gains or losses on non-monetary items are recognized consistently with the recognition of gains or losses on an item itself.For example, when an item is revalued with the changes recognized in other comprehensive income, then also exchange rate component of that gain or loss is recognized in OCI, too.

- Exchange rate gain or loss on a monetary item that forms a part of a reporting entity’s net investment in a foreign operation shall be recognized:

- In the separate entity’s or foreign operation’s financial statements: in profit or loss;

- In the consolidated financial statements: initially in other comprehensive income and subsequently, on disposal of net investment in the foreign operation, they shall be reclassified to profit or loss.

Change in functional currency

When there is a change in a functional currency, then the entity applies the translation procedures related to the new functional currency prospectively from the date of the change.

How to translate financial statements into a Presentation Currency

When an entity presents its financial in the presentation currency different from its functional currency, then the rules depend on whether the entity operates in a non-hyperinflationary economy or not.

Non-hyperinflationary economy

When an entity’s functional currency is NOT the currency of a hyperinflationary economy, then an entity should translate:

- All assets and liabilities for each statement of financial position presented (including comparatives) using the closing rate at the date of that statement of financial position.

Here, this rule applies for goodwill and fair value adjustments, too. - All income and expenses and other comprehensive income items (including comparatives) using the exchange rates at the date of transactions.

Standard IAS 21 permits using some period average rates for the practical reasons, but if the exchange rates fluctuate a lot during the reporting period, then the use of averages is not appropriate.

All resulting exchange differences shall be recognized in other comprehensive income as a separate component of equity.

However, when an entity disposes the foreign operation, then the cumulative amount of exchange differences relating to that foreign operation shall be reclassified from equity to profit or loss when the gain or loss on disposal is recognized.

Hyperinflationary economy

When an entity’s functional currency IS the currency of a hyperinflationary economy, then the approach slightly changes:

- The entity’s current year’s financial statements are restated first, as required by IAS 29 Financial Reporting in Hyperinflationary Economies. Comparative figures are used the same as current year’s figures in the financial statements from previous reporting period.

- Only then, the same procedures as described above are applied.

IAS 21 prescribes the number of disclosures, too. Please watch the following video with the summary of IAS 21 here:

Have you ever been unsure what foreign exchange rate to use? Please comment below this video and don’t forget to share it with your friends by clicking HERE. Thank you!