Updated in March 2023

I bet every single company needed to change something in its accounting records and financial statements.

Often, the change is very small, so you just don’t worry about it and make correction on the go.

But sometimes, the change can impact companies quite hard. For example:

- You are adopting new IFRS.

- You forgot to revalue your assets last year.

- You made some capital investments and as a result, useful lives of your assets are longer than you currently use for depreciation purposes.

- You booked an impairment loss of your building, but the year later, you found a buyer for much higher price than you anticipated.

- You lost that damn court case, but the settlement you need to pay is a bit lower than your provisions for it.

And I could continue like that.

Now the question is:

How to account for the change? Should we restate previous year’s financial statements? Or can we just make a change or correction in the current year?

To approach this issue systematically, you need to decide whether you deal with the change in accounting policy, change in accounting estimate or correction of error.

Let’s take a look to IAS 8 Accounting policies, changes in accounting estimates and errors.

What is the objective of IAS 8?

The Standard IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors tells us:

- How to select and apply our accounting policies;

- How to account for the changes in accounting policies;

- How to account for changes in accounting estimates; and

- How to correct errors made in the previous reporting periods.

First, we’ll explain all three terms and basic rules, and then, we will focus on clarifying the main differences between the accounting policy and the accounting estimate.

#1 Accounting Policies

Accounting policies are anything from rules, guidelines, conventions, principles and similar norms used by entities for the preparation of the financial statements.

Here, I’d like to stress that IAS 8 specifically points out that the basis, especially measurement basis is an accounting policy rather than accounting estimate.

So careful, if you are deciding whether to use historical cost or fair value measurement, you are basically selecting your accounting policy and not assessing the accounting estimate.

How to select accounting policy?

The question here is whether there IS some IFRS or interpretation IFRIC/SIC dealing with your specific transaction or situation, or NOT.

If there is some standard or interpretation, then you simply apply it. For example, when you account for your new machines, then you obviously need to apply IAS 16 Property, plant and equipment.

When there is NO specific standard or interpretation dealing with your transaction or item, then management needs to use judgement and develop its own policy, but careful, the policy needs to provide as reliable and relevant information as possible.

Example: I wrote an article about accounting for artwork under IFRS, because it is not specifically addressed by the standards and in many cases you need to develop your own accounting policy.

How should you develop your accounting policy?

First, you need to look at IFRS and IFRIC/SIC dealing with the similar or related issues. For example, if you are selecting your accounting policy for artwork, maybe IAS 16 Property, Plant and Equipment or IAS 40 Investment Property are standards dealing with similar issues.

Second, you need to apply concepts from the Conceptual Framework for Financial Reporting.

Also, in order to help, you can look to other standard setting bodies and their own rules or standards for guidance. Many companies do it regularly.

For example, IFRS do not contain any guidance related to accounting for gold as a storage of value, so they need to develop their own accounting policy.

Let me also add that you must apply every accounting policy consistently, to all transactions within the same category or of the same type. In some cases, IFRS permit to categorize your transactions – in this case, you can apply different accounting policies to different categories.

When and how to change your accounting policy?

Life brings many twists and tweaks and sometimes, you need to change your accounting policy.

When can you change the accounting policy?

Only at 2 circumstances:

- When it is required by another IFRS. This will be the case when new IFRS is issued and you HAVE TO apply it mandatorily.

- When new accounting policy provides better, more reliable and relevant information. In this case, you apply new accounting policy voluntarily.

How can you change the accounting policy?

If you apply new IFRS and this IFRS contains some transitional guidance, then you simply follow the rules in that transition provisions. New IFRS will tell you exactly how.

However, if there’s no transitional guidance, or you change your accounting policy voluntarily, then you should apply it retrospectively (there are some exceptions).

“Retrospectively” means going back to the previous reporting periods and restating every single component of equity as if the new policy had always been in place. Be careful here because you need to restate comparatives, too!

#2 Accounting Estimates

Accounting estimate are defined as “monetary amounts in the financial statements that are subject to measurement uncertainty”.

This is a new definition that came into effect on 1 January 2023.

When you change the accounting estimate, you change either some amount of an asset or a liability, or pattern of its consumption in both current and future reporting periods.

Again a little warning:

- If these changes result from some new information or new trend, or development, then they are changes in accounting estimates.

- If these changes result from some error, such as incorrect calculation or wrong application of accounting policies – then they are NOT changes in accounting estimates, but errors and they must be accounted for as for errors.

Typical examples of changes in accounting estimates are:

- Bad debt provisions,

- Depreciation rates and useful lives of your assets,

- Provisions for warranty repairs, etc.

How can you account for change in accounting estimate?

Unlike accounting for change in accounting policy, we need to change our accounting estimates prospectively, either:

- In the current reporting period, in form of so-called „catch-up adjustment“;

- In both the current and future reporting periods, if the change affects both (for example, change in useful lives affects depreciation charges in both the current and the future reporting periods).

“Prospectively” means that you do NOT restate comparatives and equity. You do NOT touch financial statements in the previous reporting periods; you simply adjust calculations in the current and future reporting periods.

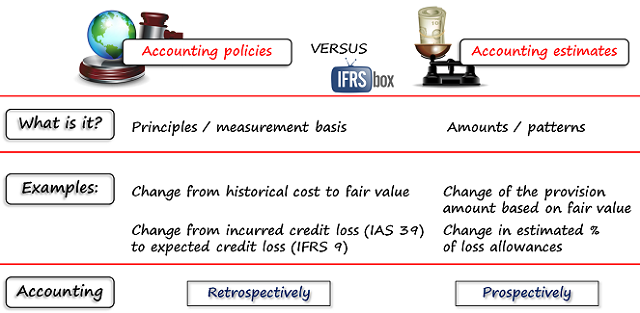

Difference between accounting policy and accounting estimate

Sometimes, it’s very difficult to assess whether we deal with an accounting policy or an accounting estimate.

What are the main differences?

- While accounting policy is a principle or rule, or a measurement basis, accounting estimate is the amount determined based on selected basis or some pattern of future consumption of the asset.For example: choice fair value vs. historical cost is a choice in accounting policy (remember, measurement basis), but updating some provision based on fair value change is a change in accounting estimate.

- While change accounting policy is accounted for retrospectively , you need to account for change in accounting estimate prospectively.

Just be very careful and realize whether it’s about principle or about calculation. If you do it wrong, well, your accounts can go wrong, too!

The standard IAS 8 says that if you cannot distinguish if your change is a change in accounting policy or a change in accounting estimate, then treat it as a change in accounting estimate.

Errors

Prior-period errors are some omissions from (that’s when you forget something) or misstatements in the financial statements as a result of ignoring or misusing the information that was available or could be reasonably obtained when preparing these financial statements.

It does not really matter why the error happened – whether it was intentional (fraud) or unintentional, you still need to correct it if it is material.

The question is:

Is the error material?

The concept of materiality is explained in IAS 1 Presentation of Financial Statements, but to simplify: anything that can affect the decisions of users of financial statements is material. In other words – anything significant.

Do not forget that something can be material not only because of its size, but also due to its nature: for example, bonuses paid to your management are always significant, whether they amounted to a few dollars or to millions.

Back to our errors:

- If the error is NOT material, then you can correct it in the current reporting period. Remember, if the error is NOT material, then your financial statements still might be reliable and relevant.

- If the error IS MATERIAL, then you always correct it retrospectively, by going back and restating your figures in the previous periods.

For the specific example with correction of error, please read here about correcting wrongly estimated useful lives of your assets.

You can watch a video with IAS 8 here:

If you liked this article or you have anything to say, please leave a comment below this video and share, thank you!