IAS 38: Intangible Asset or Expense?

Recently I had an argument with auditors of one company related to the customer list they bought.

The company paid significant amount of cash for the list of customers of telecommunications.

The list contained the names, addresses and phone numbers of all the clients.

And, the buyer intended to use the list to contact the potential customers and offer them their own services.

Well, if it’s ethical or not – I leave that up to you, but the auditors of the buyer said that the price paid for the customer list is an expense in profit or loss.

Is it???

I was not so sure.

To me, the customer list perfectly meets the definition of the intangible asset and in this case after asking few more questions I was sure that the buyer acquired an asset instead of expense in profit or loss.

In today’s article we will look at how to distinguish between intangible assets and expenses and you can find practical illustration in the end.

Including the customer list.

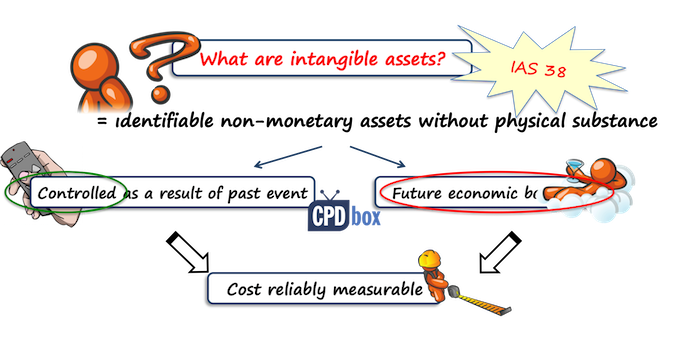

What is an intangible asset?

When I am unsure whether certain item is intangible asset or just an expense, I always look to the basic definition of an asset in IAS 38 and in Conceptual Framework, too:

An asset is a resource controlled by an entity as a result of past events, from which future economic benefits are expected to flow to the entity. (Framework, par. 4.4 (a))

And, IAS 38 expands this definition for intangible assets by specifying that on top of basic definition, an intangible asset is an identifiable non-monetary asset without physical substance.

To sum up, each intangible asset has 3 main characteristics:

- It is controlled by the entity

- No physical substance

- It is identifiable.

Just warning: it can happen that an asset has all 3 characteristics, but you cannot recognize it in your statement of financial position.

The reason is that it still may not meet the recognition criteria.

For example, let’s say you are a telecom company and you have millions of customers.

In this case, you have a customer list that is an intangible asset (please see below for reasoning), but you can’t show it in your balance sheet, because you cannot measure its cost.

Just be aware of these situations.

Now, let me explain shortly what each characteristic means.

1. Controlled by the entity

If you are able to get the future economic benefits from the use of the asset and at the same time, you can prevent others to get these benefits, then you control the asset.

In most cases, you control intangible asset when you have the legal rights to it.

For example, you may have bought the licenses or signed some contract.

Sometimes, control is achieved in a different way.

For example, you may develop some great software internally and you control its sales.

In some cases, you can’t really demonstrate sufficient control of asset and thus you can’t recognize it.

Typical example of such situation is qualified employee – human resources are rarely intangible assets, because you can’t demonstrate control.

2. No physical substance

This one is clear – if some asset has physical substance, then it’s tangible and not intangible.

However, there’s a small exception.

Sometimes, intangible asset is attached to something physical in order to carry it or store it.

In this case, the asset is still intangible because the value of the related physical asset is very small when compared to the value of intangible asset.

3. It is identifiable.

This one is crucial, I think.

The asset is identifiable in one of these 2 cases:

- It is separable – so, you can actually separate the asset and sell it, transfer it, license it or do any other action. Hypothetically.

- Arises from the legal rights – either from contract, legislation etc. In this case, the asset does not need to be separable.

For example, imagine you worked hard and you created a famous brand.

Is it identifiable?

Yes, it is, because you can (hypothetically) license it or sell it.

So, you know what the intangibles are.

From now on, always focus on these 3 characteristics to answer whether you deal with an intangible asset or not.

Can we capitalize the intangible asset?

If it is an intangible asset, then you still have 2 more questions to answer before you capitalize it:

1. Can you measure its cost reliably?

This one is straightforward.

If you can’t measure the cost, then you cannot capitalize even when it is an intangible asset.

I described the example above: you cannot capitalize internally generated customer list because you can’t really determine your cost to develop it.

2. Are the future economic benefits of the asset expected to flow to the entity?

Oh, I love this one.

Future economic benefits can be either increase in revenues or reduction in expenses.

Either way you look at them, the future economic benefits are the potential to increase your profits.

However, many people believe that you must be able to measure them – otherwise they are not the future economic benefits.

No, not at all.

In fact, it is almost impossible.

Imagine you invest in the nicer office, you buy artwork, nice furniture… can you really measure the increase of your revenues as a result of these assets?

No, you cannot, but you are quite sure that nicer office has the potential to pull more money out of the pockets of your clients.

On top of these requirements, there are still some intangible assets that are not intangible assets under IAS 38, but something else.

Important note: The above applies fully to the intangible assets that are NOT under development. If you are developing intangible assets, then you have to meet further 6 conditions to capitalize the expenditures, but let’s touch it in some of my next articles.

Let’s me show you some specific examples.

Examples of intangible assets

Licenses to trade

You operate a taxi service, but you also act as an intermediary for single private taxi drivers to get their own license.

So, as a part of your business you acquire transferrable taxi licenses from the government and you sell some of them to the private drivers who buy from you as it’s easier to get the license this way.

You acquired 1 000 number of taxi licenses.

You employ 400 taxi drivers and you plan to sell another 600 taxi licenses to private drivers.

In this case, all 1 000 taxi licenses are indeed intangible assets, because they satisfy all requirements.

However, you won’t account for all of them as for intangible assets under IAS 38.

Instead:

- 400 licenses used by your own employees are intangible assets; and

- 600 licenses to be sold are your inventories under IAS 2, because you hold them for sale in the ordinary course of business.

Internet websites

The e-shop is famous and attracts a lot of customers. There’s also a section with a company’s blog with articles about the newest fashion trends.

This website is an intangible asset, because yes, the company controls it, it has no physical substance and it is identifiable (i.e. company can sell it).

However, can you recognize it as an asset?

Yes, it brings the future economic benefits, so this one is met.

But, can you measure its cost reliably?

If it was developed externally by the third parties, then yes, you can.

If it was developed internally, then well, you have to apply the rules in IAS 38 and especially in SIC 32 Intangible assets – website costs to determine the capitalization.

Hockey team

The price you paid was derived from the quality and fame of the specific hockey players in that team.

Now, is this hockey team – or better said – contracts with players an intangible asset?

Well, I always say that no, normally you do not capitalize contracts with employees or any other expenses related to employees, because you can’t control them.

In this case, the situation can be different.

For example, hockey players might be prohibited to play in another teams by the legal rules placed by some hockey authority.

Also, the contracts with individual players might legally bind the player to stay with the same team for a number of years.

In this case, you would be able to demonstrate control and yes, recognize hockey team as your intangible asset.

Software licenses

When the computers arrived, you made an online purchase of corresponding number of licenses for Windows XY operating system to run the computers.

Also, you purchased a license to use the specific accounting software.

On top of the purchase cost you are required to pay the annual fee for upgrades of the software. You can continue using the license for accounting software also without annual upgrade fees, but you won’t receive any updates.

Here, we have 3 items:

- Operating system Windows XY

Yes, it is an intangible asset because it meets all the criteria.

However, operating system is an integral part of the computers, because the computers can’t run without the system.

Therefore, you would recognize computers together with operating system as property, plant and equipment, so no separate intangible asset.

For further reference, look to par. 4 of IAS 38.

- Accounting software license

This is an intangible asset, too.

In this case, you need to recognize the license as an intangible asset, because accounting software is NOT essential to run the computer.

- Annual upgrades

Annual upgrades do not meet the definition of an intangible asset, because they are not separable.

They are expensed in profit or loss when incurred.

You can see them as something similar to maintenance and repair costs of property, plant and equipment.

Customer lists

Is this an intangible asset?

In most cases yes, because:

- It has no physical substance,

- It is identifiable (yes, it is because you were able to buy it),

- You control it,

- You can measure its cost reliably (you paid for it) and,

- You expect the future economic benefits (increased sales as a result of new list of potential customers).

I spoke more about it in this IFRS Q&A podcast episode.

Warning: in some countries and at some circumstances such a customer list is not an intangible asset.

The reason is that some countries have legislation in place that prevents you from random contacting the potential customers on the list.

In this case you would not be able to get the future economic benefits from the list because you cannot use it (so why would you buy it anyway?). Thus you do not control the asset fully.

However, telecoms often ask their customers to agree with passing their data to third parties for advertising purposes, so in this case you would be able to use the list (hint – read the small letters in the contracts to know what you agree to!).

You have to assess all of these things to conclude whether the customer list is an asset or not.

Advertising campaign

Some companies invest heavy cash into their advertising campaigns.

Literally millions.

Imagine you plan to invest 1 mil. EUR into the advertising campaign over the next year.

Your advertising agency told you that this campaign would build and strengthen your brand and position in many years to come.

So, some people believe that yes, they should capitalize advertising campaign as it brings the future economic benefits.

No dispute on this.

The only thing is that the advertising campaign is NOT identifiable – you can’t separate it and sell it to someone else.

Therefore, you should recognize the expenditures for advertising campaign in profit or loss.

Of course, when you prepay the campaign for let’s say 2 years, then you should recognize the expenses over 2 years as the services are consumed.

Do you have questions about any other specific items? Please let m know in the comments. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

153 Comments

Leave a Reply

Hi Silvia, My company is looking at implementing a new accounting system and we’re engaging a consultant to assist with the implementation. Are the costs associated to implementing the system able to be capitalized? I know the costs to buy the actual system would be eligible to capitalize and then we’d expense the ongoing license fees billed to us annually, but I am unsure whether consultant costs to assist in implementing the actual software itself would meet the recognition requirements of IAS 38..

Hi Silvia. How does a production entity treat the production cost incurred to produce a TV show. The company retains the right to the show to distribute in the future, but the main focus of the production is only to make revenue from the initial broadcasting of the show due to sponsorship revenue received (to promote the sponsor brand via advertising it during the show broadcasting)

Hi Anelle, well that cost meets the definition of an intangible asset and can be capitalized. As for amortization – normally these TV rights, shows etc. are amortized over the period of broadcasting rights, so it depends.

Can expenses related to product registration fees or manufacturing site registration fees be capitalized? (In order to import products, you have to pay registration fees to government agencies. Can these be considered as intangible assets?)

How about a Mobile app ? Can we recognize as an intangible ?

In general yes, but it depends on the specific situation.

Dear Silvia, can mobile apps consider as indefinite useful life and don’t need to be amortised?

Our Company registered ” Nice chocolate” as a trade mark in UAE. Initially incurred cost for registration and legal fee USD 1000/= however to complete this process will be taken another 6 months and initially incurred cost (USD 1000/=) can we recognize under intangible asset or development cost in SOFP.

Hi Silvia,

Thank you for consistent sharing of your IFRS expertise.

Important note: The above applies fully to the intangible assets that are NOT under development. If you are developing intangible assets, then you have to meet further 6 conditions to capitalize the expenditures, but let’s touch it in some of my next articles.

Can I have the link to the article, please?

Hi Silvia

The design packaging task for new products are done through a third party and the cost can be identified separately. Economic benefit will be flowing once the products are sold in the market. Shall the cost be treated as intangible assets? If so, it is like a brand and we can use either finite useful life for amortization or indefinite useful life with impairment assessment at each reporting date. Please advise my understanding is right or not.

Hi Win, I have one small problem here – is the design packaging identifiable? Is it separable? Can you sell it to someone else? Transfer it? If yes, then agreed, you can capitalize it.

It can be identified and has a separate design for each product but I don’t think it can be sold or transfer to someone as a design. We can only sell products or transfer production rights.

So please read about assessing identifiability in this article and try to assess it yourself, for me it is quite difficult to conclude that this design packaging for each product is identifiable.

I understood. Thank you for your kind advice.

Hello – I work for a manufacturer that develops processes for auto part manufacture. With each product launch, we enter a development phase. What is truly difficult for us to define is where this product development phase ends. I have used “saleable and production part” and “replication” as points of defining a stop point. But what if something goes wrong and the process is not developed appropriately? How can we determine costs eligible for “reopening” development?

Hello, I would like to ask is Company App qualified for capitalized?

This seems to apply Internally generated intangible assets.

If it meets 6 criteria for capitalizing developmnent costs, then yes. You can capitalize SOME internally generated intangibles.

Hi Silvia!

I have a question regarding trademark, Our company wants to sell the the Brand name to another party (another subsidiary or Holding company). As I’ve read IAS38, because the trademark was developed internally, no asset can be recognized. I’m a bit confused regarding the treatment of selling the trademark, Can you please explain, how can it be done?

Hi Natalia,

well, you cannot recognize internally generated brands, that is true and therefore when you sell it, you simply recognize revenue and that’s it/ However another party who is a buyer can recognize this trademark, because for them it is no longer internally generated, but purchased. Be careful upon consolidation – from the group’s point of view, there is no trademark as it would still be internally generated by the group. S.

Thank you Silvia!

But still, is it possible to recognize the brand name as an asset held for sale after its valuation (IFRS 5), and afterwords make a selling deal? would it be a mistake?

Interesting question. In my opinion no, because you can classify a non-current asset as held for sale under IFRS 5 and it means that the internally generated brand should have met the conditions to be capitalized as a non-current asset first (intangible asset) and then to be classified as held for sale – but it does not.

Hi Silvia, just need a clarity on the below scenario; whether we can categorize as an intangible asset or not:

if company purchase a title sponsorship rights/license to exercise the title sponsorship rights via contract from a sports board and this rights may be transfer / sold to other entity and has a duration of more than one year. in this contract company gain marketing & branding rights / exclusive space on ground,

Hi Silvia,

I have a question. If an NGO develops a mobile application, should it be recognized as intangible asset.

If it meets 6 conditions for capitalizing development expenditure, then yes.

Dear Silvia,

Can the advertisement campaign be identifiable based on the contract we signed? and treat it as an intangible asset?

No, it is specifically said in IAS 38.

Thank you Silvia for this material on IAS 38 and in general all the other material. It is so clear and easy to understand and apply the standards.

Hi Silvia,

we have a consultant contract to build our business plane, strategy, pricing model, analysis to address key risk and challenges and support in activating and engaging with our partners, based in these items can we capitalize the cost?

Regards,

Hi Aziz, and what is the specific asset to which you can capitalize these expenses as directly attributable? I don’t think there is any. You cannot capitalize it as an intangible asset by itself, as it does not meet the identifiability criteria. S.

Hi there,

We do a lot of R&D work for our software and have recently incurred legal and professional fees associated with one of our R&D projects, which is due to go live relatively soon. Could we include these fees in the capitalisation of the overall project?

Well yes if it relates to development stage and all PIRATE criteria are met for that stage. Also, these fees must be directly attributable to the project.

Hi, Silvia very informative.

Would like to know if there is any possibility of accounting for website costs as property, plant and Equipment under IFRS?

Dear Sylvia,

A question here – Telecom companies are highly IT /Systems dependent . It is a constant argument whether or not the cost of a particular development being done on a platform/IT system can be capitalized or not . Is there any guidance on that ? . Any part of the standard I can go to.

I am talking about mini/big projects at a measurable cost, external(vendor) or internal development staff involved, in some manner changing the way the system was operating earlier

The argument that made me ask this question is a case where we have multiple legacy systems that now need to be ‘bridged’ or ‘integrated’ to enable certain efficiencies – Some costs are development of extensions to the existing systems (This does not make them better in any way but makes them ready for integration) and then there is the ‘integration’ layer development which will give us the efficiencies – Can I capitalize any or both of the costs .

Thank you for your time , its is always a pleasure to check through IFRS box when you need ‘IFRS in plain English’.

Dear Silvia,

The article is really helpful. Your website is one stop shop for all accounting related queries.

Thanks for the help.

Wow, as an American accounting professional, this is fascinating. I knew just a little bit about the rules governing intangible assets and expenses, but it never occurred to me how many different examples there were for this type of tax filing classification. Thanks for the read.

Dear Silvia, just to reconfirm what I read in your article, In case if our company purchases licenses for which ownership is still with Original Company and we cannot sell them and only have right to use them during more than 1 year, can we capitalize such licenses as Intangible assets? thank you

Dear SILVIA,

We purchased user licences to enable our staff access the cloud accounting software. The user licences are a one off lifetime fee. Should this be capitalized or expensed?

Dear Silvia,

my question is somewhat related to the question of Syed.

My company buys hosting services and domains (the third party provider hosts the hardware, storage and other components). We pay an annual renewal fee, and if we do not pay the fee, we loose the access to the domains.

What is the accounting treatment for these cloud computing arrangements?

Thanks!

Hi,

Scenario:

Company buys 2 domains, lets say for $1000 each.

Company pays renewal fees ($100 each) to keep domains active.

Renewal fees for 1 domain is for an year and renewal fees for 2nd domain is for two years.

If company doesn’t pay renewal fees, domain will remain exist for additional 1 month and then it will be auctioned and company will loose it.

Questions:

1. Should domain cost (Not renewal cost) be recorded as Intangible Asset?

2. If yes, then considering its life is indefinite so we shouldn’t amortize it instead it will be impaired, yes ?

3. Renewal fees which are paid for 2 years validity, how should we record them?

Thank you.

my employer has developed a software which is leased to several insurance companies and they annual licences and maintenance fee, from the above summary i understand that i should recognise it as intagible asset but am not clear on whether i should amortize it, whether i should present it separately in the balance sheet, and the kind of policy/dicloure i should incorporate in the financials.

Hi Daniel, yes, you should recognize this software in the balance sheet, in the amount of capitalized cost for development – see more here. Of course, you should amortize, revise its useful life etc. S.

Hi sylvia. I needed to ask that will you classify the feasibility study cost for upgrading a website as intangible or not?

Why face book ?

Will Cost paid to consultants for developing strategic analysis be intangible assets

I don’t understand this question… “why facebook?”??? It depends on whether the strategic analysis is an asset or not (mostly not), and what is it about.

Hi slivia .

Can we capitalize the expense incurred on Facebook advertisement as brand exp ???

No. That’s prohibited by IAS 38.

Hello Silvia!

I would really appreciate your dedication to enhance our knowledge regarding IFRS. I would like to ask you if I can capitalize costs incurred for the development of strategic plan running for five or more years on an outsource basis(by hiring consultants) as an intangible asset?

Regards,

If it meets all 6 PIRATE criteria, then yes. Please see more here.

Hi Silvia

I have maintenance fees for 7 months on intangible(software),Is this going to be amortized to PL for 7 months or I can out it as intangible asset?

Secondly,Is system ehancement an intangible asset?

Well, maintenance fees are maintenance – expense in profit or loss. Of course, if you prepay for some period, then maybe you will have deferred prepayments in the balance sheet.

System enhancement – it depends on what it is, but in general yes.

Thanks Silvia, good insight of IAS38. I have one question.

Que – Will Land use right be considered as intangible asset. Say Land use right is for 50 years which was received from Government. we can construct on land and use it for the 50 years.

Thanks!

I have the same concern as you. I’m very confusing that someone treats as intangible FA under IAS 38, and someone treats as an operating lease under IFRS 16 ^^

Good job

Dear Silva,

Greetings,

Please could you share us Conversion process from GAAP to IFRS

Hi Feleke,

I have the full conversion videos inside my IFRS Kit, but this article describes it step by step. I wrote it a few years ago, but it’s still valid.

Best

S.

Dear Silvia,

Thank you a lot for such a huge information about intangibles.

But I have some doubt regarding an accounting software. If we buy it and use it, actually we can`t resell it to someone else due to absence of “rights”. That is why, in my opinion it should be booked as an expenditure in profit or loss.

You can’t resell it, but you are going to use it to produce your own goods/services. That’s basically sufficient economic benefit to recognize an asset.

Hi Silvia,

I really enjoy reading your article. I have a question for you. Many telecom companies use frequency band to forward traffic. These frequencies are granted by the regulator for an annual fees on the duration of existence of the operator.

These frequencies meet the three criteria of control, identifiability, with no physical substance.

The recognition of the frequencies as an intangible is complicated by the following difficulties : the reliable evaluation of the amount to be immobilized because of the possibility of change of fees amount in the future as well as the difficulty determining an amortization period of this asset because sometimes these frequencies can be used with licenses having different durations (2G, 3G, 4G).

Can we use those arguments to prove that these frequencies cannot be recognized by the balance sheet as intangible asset.

Hi Pedro,

telecom licenses for certain frequencies are accounted for mostly as intangible assets, but in some cases as leases under IAS 17/IFRS 16.

As for reliable measurement of cost: it seems that if you are paying the annual payments, then you rather have a lease here, not intangible asset. S.

Hi Silvia,

I have one question, How to treat the accounting manual prepared/ developed by the company? is that an intangible asset or expense?

Hi Tse,

I will still repeat my previous answers – if the company develops the accounting manual itself, then on top of 3+2 criteria it must meet further 6 criteria for development expenses to be capitalized. So, you have to assess.

Amazing article, thank you.

And finally I’ve understood why we can’t capitalize advertising costs but we must capitalize software licences: the contract makes the licence a separate asset while there isn’t a lasting contract for the advertising expense.

I have a question on customer list.

Let’s say the company didn’t by the list outrightly but contracted a consultant to generate the list. From the projection of the consultant showing the breakdown for billing there are expenses meeting definition of PPE, some meeting intangible asset and some are P or L items. All of these assets (PPE AND intangibles) will be owned by the company not the consultant at the end of the project. How will these be recognised.

For example, see below for a draft bill:

Computer hardwares 30%

Computer software licences 20%

Wages to field staffs. 10%

Consultancy fee. 40%

How will these be recognised on the financial statement?

NB, all of the computer hardware will be owned by the company at the end of the project. Also, the project might span for a period of more than one year but the percentage completed list becomes use able upon completion of that part

How do I recognize and measure Intangible assets with Indefinite life.

It is awesome, more than what we get from the lecture room. Thanks a bunch

This is a marvelous public sevice towards enhancing the quality of accounting practice world wide.

Continue the good work.

Hi Silvia,

Well-written topic with easily understandable explanations.

One questions in regards of below wording:

“For example, imagine you worked hard and you created a famous brand.

Is it identifiable?

Yes, it is, because you can (hypothetically) license it or sell it.”

Could you please clarify, whether internally-generated brand names may be recognized as an intangible asset or not?

Thanks.

Hi Babayev,

no, you cannot. IAS 38 explicitly prohibits it, mainly because you cannot measure the internal costs to generate the brand.

Good morning Silvia,

Assuming you have an internally know-how to make equipment that you sell under your internally brand name. However, before you sell the equipment you have to subsequently adapts the equipment to fit the market.

How would you treat the cost of the know-how to develop the equipment and the subsequent adaptation cost of each equipment sold.

Hi Joseph,

well, it’s difficult with internally generated intangibles because you cannot really measure their costs in many cases. S.

Very educative material. Keep on posting such. I really enjoy your articles. Shall share with others.

Thank you very much,

So helpful

Hi Silvia,

I really enjoy reading your publication and I did leant a lot! I always have a question in my mind when coming across with this topic, Intangible Asset – how should I classify this kind of payment as “Intangible Asset” or “Prepaid Expenses”?

Great, that’s what I wanted 🙂

Hello Silvia First of All I am really thankful for your valuable contributions towards IFRS.It helps me lot in learning IFRS and in crack the exam of DIPFRS.Secondly I have one doubt in mind that how to classify between intangible asset and prepaid exp.

Just back to the customer list the ability to sell or the intention to sell would impact my decision to capitalize , and what about a company which develops a school curriculum for its own future schools and does not want to sell it , and currently the company expenses are all towards this project only and this company was setup to achieve this curriculum only.

As I wrote above – the assets internally developed must meet further 6 criteria to be capitalized (see my response above). Also, it’s questionable whether the school can measure the expenditures to develop the curriculum reliably.

Dear Silvia,

i trust your thought process and would like to confirm my understanding, My view that the school curriculum should not be capitalized because the future benefits of this curriculum is under question and i can not from now judge whether it will increase revenues and gets attention and plus the company does not have the intentions to sell it outside, it is developing it for own schools. it meets all other conditions except i am challenging the future benefits. They have been for a couple of years developing it and the previous auditor has accepted its capitalization.

regards,

Dear Rabih,

the school does not necessarily need to be able to sell it – the demonstration that that the school will use the curriculum for its own use would be sufficient. I would say that the future economic benefits are not in question, especially if they plan to abandon the older curriculum and attract the new (more) students to the new one. Therefore I would not refuse capitalization. However, especially with intangibles under development, you need to be very careful and question all aspects and conditions, because companies like to present the true expenses in balance sheet as intangibles just to look better.

Best, S.

Can you give ecample for advertising campaign what capitalized and what not ?

In fact, you can only capitalize some tangible assets within advertising campaign like stands, signs, etc. – but as property, plant and equipment. Why not – that’s stated in the article.

What its not tangible can´t be capitalized because its not identifiable, cant be separated or transfered . And as long as it is imposible that it arises from legal rights

When you prepay a campaign for let say 2 years.Is not that prepayment affect both the profit and loss statement and balance sheet.or there are other prepayments that can only affect the p/l statements.

How should that advertising campaign prepayment be treated according to IAS 1 and 38?

If you prepay the campaign for 2 years, then you need to defer the expenses, but it’s not presented as intangible asset, but as other asset.

Hello Silvia, can you please explain further on what you mean by “defer the expense”?

You would book it as some deferral account in balance sheet and then recognize it in profit or loss in the later period when the service is consumed.

Thank you Silvia for the explanation

ah do you mean like prepaid expense when we pay in advance?

Dear Silvia,

What if a client is sponsoring a player for his development / training and is expecting once he joined/selected by any league in future or start generating revenue amount in future as mentioned in the agreement, the revenue (salary, price money + Bonus) he earned will share with his sponsor.

Q. Can he (Sponsor) accumulate the cost of sponsorship in his books as an Capital Work in Progress under the classification of “intangible assets” until the last payment and subsequently capitalize as “sponsorship contract or sponsorship contract rights”?

For clarity purpose – There is proper agreement between the player (including his parents) and sponsor. The agreement meet the 3 + 2 rules as explained by you.

Hi Raheel, this is very interesting question, thank you.

I should have added in the article that this mainly applies to ready-to-use intangible assets; not to intangible assets at the development stage. So, I will add up the note – thanks again for bringing this up – and to respond to your question: if you believe that all 3+2 are met, then you should check further 6 conditions stated by IAS 38 for capitalizing development cost, because your intangible asset is under development and not ready to use. Please see par. 57 of IAS 38, but in short: technical feasibility, intention to complete, ability to use/sell, how the future economic benefits are generated, availability of resources to complete, ability to measure expenditure reliably. However, in this case, I’m not sure whether you can meet all these 6 criteria… S.

Thank you Silvia

“…some countries have legislation in place that prevents you from random contacting the potential customers on the list.”

Interesting. Could you share examples?

Well, Maria, for example – in the European Union, there’s a new regulation “GDPR” (General Data Protection Rights) in place since 25 May 2018 – here, companies must make sure they can contact potential customers from the purchased list by securing their consent, etc. – it’s quite difficult.

Hi Silvia! Thank you for amazing article! I have a question for you. Many companies use accounting program as known 1C in our country, I think not only in my country but across the world especially “СНГ” countries. After setting this program, setted company presents license for right of use. Is this intangible asset or not? This program license, in my opinion, is not according with IFRS because It is not separable – so, you can not actually separate the asset and sell it, transfer it, license it or do any other action. What do you think?

Mirolim, this is the intangible asset as far as the license is for more than 1 year. The asset does not need to be separable – but identifiable, and this is reached by 2 ways: 1) separability 2) contract= that’s this case. Very simply said.