Last update: July 2023

Have you ever heard a joke about two accountants applying for a job?

During their interview, they were given a task to calculate a net profit figure based on available data.

After some while, interviewer asked them a question: “What result did you get? What is the net profit of this company?”

The first accountant replied: the net profit is 150 mil. USD.

And the second one asked: “What would you like it to be?”

Now guess which one got the job! 🙂

In fact, manipulation of profit figure by making and releasing various provisions back and forth was very popular “creative accounting practice” in the past.

No wonder, as there were no rules for making provisions. Therefore, many companies utilized so-called “big bath provisioning” in order to smooth profits.

This situation was addressed in 1998 when the standard IAS 37 Provisions, Contingent Liabilities and Contingent Assets was issued with its effective date from 1 July 1999.

What is the objective of IAS 37?

The Standard IAS 37 Provisions, Contingent Liabilities and Contingent assets sets the criteria for recognition and measurement of

- Provisions;

- Contingent liabilities;

- Contingent assets; and

requires a number of disclosures about these items in order to understand them better.

What is a provision?

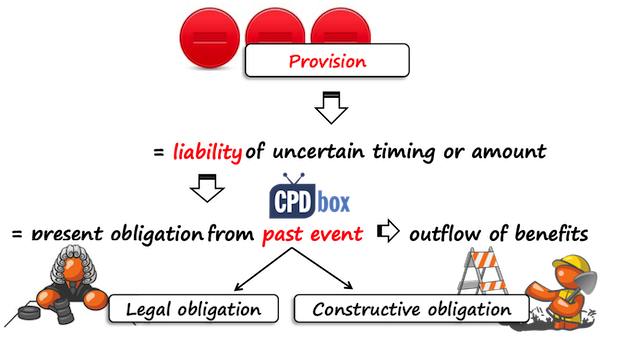

Provision is a liability of uncertain timing or amount.

The word “uncertain” is very important here, because if timing and amount are certain or almost certain, then you don’t deal with the provision but with a payable or an accrual.

To understand provisions better, let’s break down the definition of a liability in IAS 37:

A liability is a present obligation arising from past event that is expected to be settled by an outflow of economic benefits from an entity.

In other words, if there is no past event, then there is no liability and no provision should be recognized.

Past event can create 2 types of obligation:

- Legal obligation that arises from legislation, a contract or other legal act; or

- Constructive obligation that arises from some business practice or customs and created an expectation in other parties to fulfill the obligation (in other words, people simply expect some company to fulfill the obligation even if it’s not in the law or any contract).

It does not really matter what type of obligation you deal with – whichever it is, it leads to a provision. However, if you identify the obligation, it can help you to decide whether recognize a provision or not.

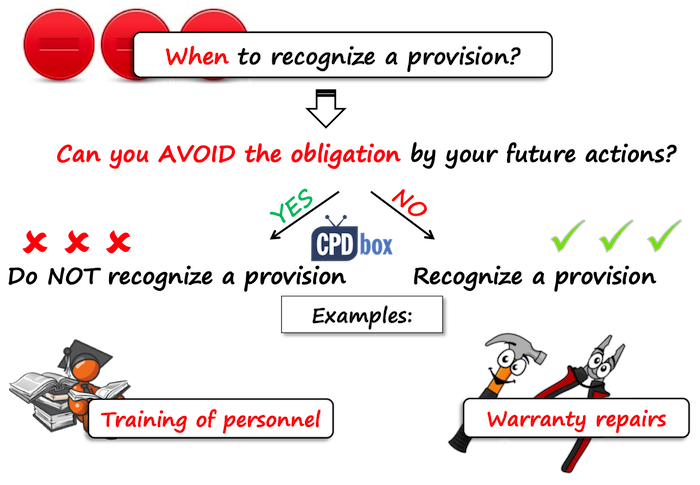

When to recognize a provision?

The standard IAS sets 3 criteria for recognizing a provision:

- There must be a present obligation as a result of a past event;

- The outflow of economic benefits to satisfy the obligation must be probable (i.e. more than 50% probable)

- The amount of economic benefits required to satisfy the obligation must be reliably estimated.

If all 3 criteria are met, then you should recognize a provision.

If just one of them is not met, then you should either:

- Disclose a contingent liability (read more about it below), or

- Do nothing if the outflow of economic benefits is remote.

To get better understanding and guidance on provisions and contingencies, IAS 37 presents a decision tree, too.

If you are unsure whether to recognize a provision in a particular situation or not, just ask yourself a simple question:

Can the obligation be avoided by some future actions?

If yes, then you should NOT book a provision. For example, if a government introduced new tax legislation, does the tax consulting company need to spend a cash for training of its employees and thus recognize a provision for that training?

No, it does not have to. Tax consulting company can avoid the training and decide to stop its activities (OK, that’s a bit far-fetched and unlikely, but you get the point).

If you cannot avoid the obligation by some future action, then you have to recognize a provision.

For example, when you promised a free warranty service for defective products at the point of sale, then you have a present obligation. If your past statistics show that you needed to spend some cash for warranty repairs, then you need to make a provision.

How to measure a provision?

The amount of the provision should be measured at the best estimate of the expenditures required to satisfy the obligation at the end of the reporting period.

As you can see, here’s some judgement and estimates involved. Management should really incorporate all available information in their estimates and they must not forget about:

- Risks and uncertainties (like inflation),

- Time value of money (discounting when the settlement is expected in the long-term future)

- Some probable future events, etc.

There are 2 basic methods of measuring a provision:

- Expected value method: You would use this method when you have a range of possible outcomes or you measure the provision for large amount of items. In this case, you need to weight each outcome by its probability (for example, warranty repair costs for 10 000 products).

- The most likely outcome: This method is suitable in the case of a single obligation or just 1 item (for example, provision for loss in the court case).

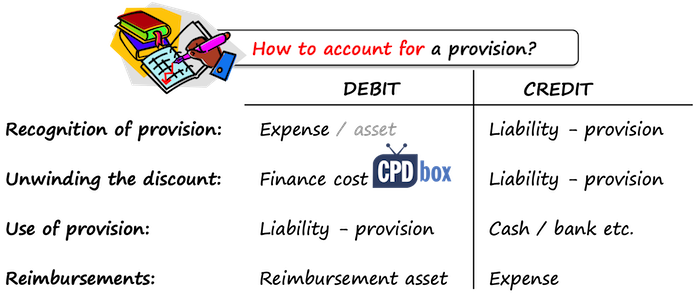

How to account for a provision?

There are several events associated with the accounting for provisions:

-

- Recognition of a provision: In most cases, you should recognize a provision in profit or loss. Sometimes, a provision is recognized in the cost of another asset, for example, provision for removing the asset and restoring the site after its use.Don’t forget to split the provision in the current and non-current part for the presentation purposes in your statement of financial position.

- Unwinding the discount: When a provision has a long-term nature (beyond 12 months), then there’s some discounting involved as you need to present it in its present value.In each reporting period, you account for an interest on the opening balance of the provision and this is called „unwinding the discount“.Special For You! Have you already checked out the IFRS Kit ? It’s a full IFRS learning package with more than 40 hours of private video tutorials, more than 140 IFRS case studies solved in Excel, more than 180 pages of handouts and many bonuses included. If you take action today and subscribe to the IFRS Kit, you’ll get it at discount! Click here to check it out!You should recognize the interest in profit or loss and it also increases the amount of a provision.

- Utilization of a provision: When you incur expenditures associated with the settlement of your obligation, you should „utilize a provision“.In most cases, you simply recognize this utilization directly with incurring the invoices from suppliers or any related payments (e.g. Debit Provision / Credit Cash).

- Reimbursement: Sometimes, entities have right to reimbursement of related expenditures by the third party (e.g. from an insurance company).In this case, a right to reimbursement is recognized as a separate asset (no netting off with the provision itself), but you can net off the expenses for provision with the income from reimbursement in the profit or loss.

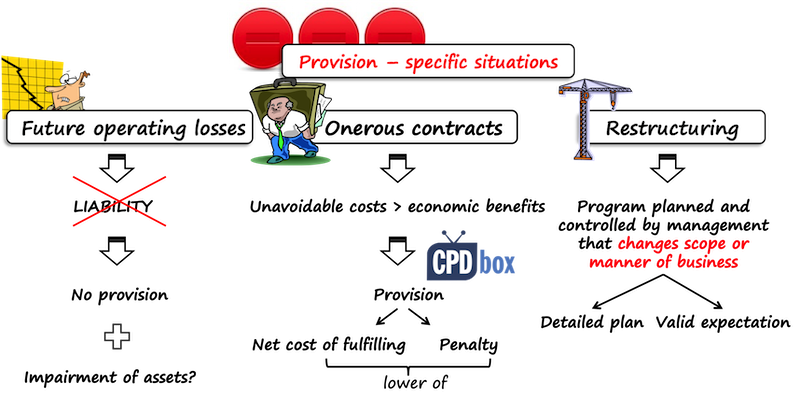

Provisions in specific circumstances

Standard IAS 37 specifies the treatment of provisions in a few specific situations:

Future operating losses

You should not make a provision for future operating loss.

Why?

Because there is no past event. The future operating losses can be avoided by some future actions, for example – by selling a business.

However, you should test your assets for impairment under IAS 36 Impairment of Assets.

Onerous contracts

Onerous contract is a contract in which unavoidable costs of fulfilling exceed the benefits from the contract.

In other words, it is a loss contract that cannot be avoided.

You should make a provision in the amount lower of:

- Unavoidable costs of fulfilling the contract and

- Penalty for not meeting your obligations from the contract

Restructuring

Restructuring is a plan of management to change the scope of business or a manner of conducting a business.

You should recognize a provision for restructuring only when the general criteria for recognizing provisions are met.

In the case of restructuring, an obligation to restructure arises only if:

- There is a detailed formal plan for restructuring with relevant information in it (about business, location, employees, time schedule and expenditures)

- A valid expectation related to restructuring has been raised in the affected parties.

IAS 37 also clarifies which type of expenses can / cannot be included in the provision.

What are contingencies?

Except for provisions, we can deal both with contingent liabilities and contingent assets.

Contingent liabilities

A contingent liability is either:

- A possible obligation (not present) from past event that will be confirmed by some future event; or

- A present obligation from past event, but either:

- The ouflow of economic benefits to satisfy this obligation is not probable (less than 50%), or

- The amount of obligation cannot be reliably measured (this is very rare, in fact).

For example, you might face a lawsuit, but your lawyers estimate the probability of losing the case at 30% – in this case, it’s not probable that you will have to incur any expenditures to settle the claim and you should not book a provision. It’s typical contingent liability.

If you identify you have a contingent liability, you do NOT recognize it – no journal entry. You should only make appropriate disclosures in the notes to the financial statements.

Contingent assets

A contingent asset is a possible asset arising from past events that will be confirmed by some future events not fully under the entity’s control.

Similarly as with contingent liabilities, you should not book anything in relation to contingent assets, but you make appropriate disclosures.

Provisions and further specific guidance

Standard IAS 37 gives further guidance for certain situations in its appendix and also, several interpretations clarify the accounting for provisions in some specific cases:

- IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities deals with the provision for removing the asset and restoring the site after the end of its useful life;

- IFRIC 5 Rights to Interests Arising from Decommissioning, Restoration and Environmental Rehabilitation Funds is related to IFRIC 1 and it applies when a company contributes to a fund for reimbursement of these expenses.

- IFRIC 6 Liabilities Arising from Participating in a Specific Market – Waste Electrical and Electronic Equipment: this IFRIC specifies when the producers of electrical and similar appliances sold to household are liable for decommissioning of electrical waste

- IFRIC 17 Distributions of Non-cash Assets to Owners

- IFRIC 21 Levies

Here’s the list of articles published on CPDbox related to the standard IAS 37:

- How to account for decommissioning provision under IFRS

- Practical questions about accounting for provisions

You can watch a video with IAS 37 here:

If you liked this article or you have anything to say, please leave a comment below this video and share, thank you!