IAS 28 Investments in Associates and Joint Ventures

Let’s focus on associates, joint ventures, significant influence and equity method today.

You have already learned various aspects of having control over some investment: how to identify it, how to account for it and we also learned basic consolidation procedures step by step.

It was all covered by IFRS 3 Business Combinations and IFRS 10 Consolidated Financial Statements.

Another very frequent type of investment is an associate over which an entity has significant influence. It is all arranged by the standard IAS 28 Investments in Associates and Joint Ventures, so let’s take a look.

What is the objective of IAS 28?

The objective of IAS 28 Investments in Associates and Joint Ventures is:

- To prescribe the accounting for investments in associates, and

- To set out the requirements for the application of the equity method when accounting for investments in associates and joint ventures.

Let me remind you a couple of terms:

An associate is an entity over which an investor has significant influence.

A joint venture is a joint arrangement whereby the parties having joint control of the arrangement have rights to the net assets of the joint arrangement.

What is significant influence and how to detect it?

Standard IAS 28 defines significant influence as the power to participate in the financial and operating policy decisions of the investee, but is NOT a control or joint control of those policies.

Sometimes, it can be quite difficult to determine whether we deal with control or significant influence – and we can’t make a mistake, because the whole accounting treatment and reporting depends on this classification.

How can significant influence be evidenced?

The main indicator of significant influence is holding (directly or indirectly) more than 20% of the voting power of the investee.

BUT!

It’s not the rule of thumb and often, the truth is different.

Sometimes, when an investor holds more than 20% of the voting power (but less than 50), it can still control the investee.

Let me show you an illustration (taken from my IFRS Kit):

Here, CarProd does not own the majority (over 50%), but it’s still more than 20% – that would indicate significant influence.

But, as other investors own max. 1% each, the probability of outvoting CarProd in major decisions is very low, so CarProd may in fact exercise control over TyreCorp, rather than significant influence. Of course, you would need to examine it further.

The other ways of evidencing significant influence are as follows:

- Investor has a representation on the board of directors (or other equivalent governing body) of the investee.

- Investor participates in policy-making processes (including dividend decisions).

- There are material transactions between the investor and its investee.

- There’s interchange of managerial personnel.

- Provision of essential technical information.

When you assess the presence of significant influence, you should not forget to examine potential voting rights (in form of some options to buy shares, or convertible debt instruments, etc).

Apply the equity method

Once the investor acquires significant influence, or joint control of a joint venture, then it must apply equity method.

The basic principles of equity method are:

On initial recognition:

- The investment in an associate or joint venture is recognized at cost. The journal entry is:

- Debit investments in the statement of financial position,

- Credit cash (bank account, or whatever applies).

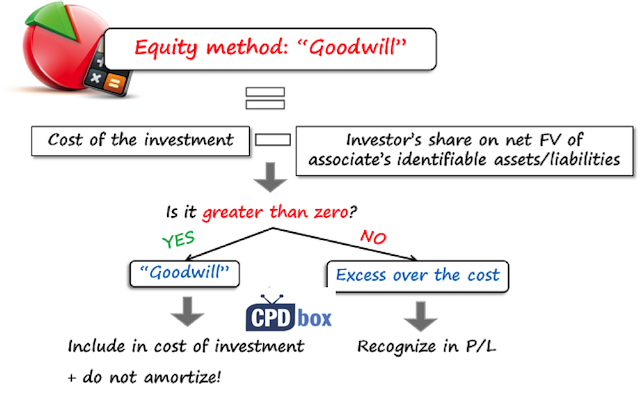

- If there’s a difference between cost and investor’s share on investee’s net fair value of identifiable assets and liabilities, then it depends, whether this difference is positive or negative:

- When the difference is positive (cost is higher than the share on net assets), then there’s a goodwill and you don’t recognize it separately. It is included in the cost of an investment and NOT amortized.

- When the difference is negative (cost is lower than the share on net assets), then it’s recognized as an income in profit or loss in the period when the investment is acquired.

Subsequently, after the initial recognition:

- The carrying amount of the investment is increased or decreased by the investor’s share on investee’s net profit or loss after the acquisition date. The journal entry is:

- Debit Investment in the statement of financial position, and

- Credit Income from associate in profit or loss.

Or vice versa when an associate made loss.

When an associate or joint venture make losses and these losses exceed the carrying amount of the investment, investor cannot bring down the carrying amount of the investment below zero. Investor simply stops bringing in further losses.

- When an investee distributes some dividends to the investor, then such a distribution decreases the carrying amount of the investment. The journal entry is:

- Debit Cash (or whatever applies here) and

- Credit Investment in the statement of financial position.

Learn the equity method procedures

The procedures in equity method are very similar to consolidation procedures under the standard IFRS 10 Consolidated Financial Statements:

- Both investor and investee shall apply uniform accounting policies for the similar transactions.

- The same reporting date shall be used, unless it’s impracticable.

- Investor’s share on gain or loss from mutual „upstream“ and „downstream“ transactions is eliminated.So here, you don’t eliminate mutual balances (receivables or payables) outstanding at the end of the reporting period, but you eliminate just investor’s share on trading profit and similar items.

Exemptions from applying the equity method

Investor does not need to apply the equity method in one of the following circumstances:

- Investor is a parent that is exempt from preparing consolidated financial statements by the scope exception of paragraph 4(a) of IFRS 10 (it’s similar as below point); OR

- All of the following applies:

- The entity is a wholly owned subsidiary; or it’s a partially-owned subsidiary of another entity and its other owners have been informed about and do not object to not applying the equity method;

- The entity’s debit or equity Instruments are not traded in a public market;

- The entity did not file, nor is in the process of filing, its financial statements with a securities commission or other body for the purpose of issuing any class of Instruments in a public market;

- The ultimate or any intermediate parent of the entity produces consolidated financial statements available for public use that comply with IFRS.

- When an investment in an associate or a joint venture is held by in entity that is a venture capital organization, mutual fund, unit trust or similar entity, then investor might opt to measure investments at fair value through profit or loss under IFRS 9 (and thus not apply equity method).The same applies for the situation when an investor has an investment in an associate a portion of which is held by these organizations.

Here, I’d like to add that when an investment meets the criteria in IFRS 5 and is classified as held for sale, then an investor shall apply IFRS 5 to that investment and not equity method (even when it relates to a portion of investment, then IFRS 5 is applied to that portion).

When to discontinue equity method

An investor stops applying the equity method when its investment ceases to be an associate or a joint venture.

The way of discontinuing depends on specific circumstances, for example if the investment becomes a subsidiary, then an investor stops equity method and starts full consolidation in line with IFRS 10/IFRS 3.

You can watch a video with the summary of IAS 28 here:

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

122 Comments

Leave a Reply

I have a doubt, Say my associate also prepares CFS and has an investment in it’s associate accounted under equity method. Now for my Consolidation purpose should I take net assets of my associate as it is for investment valuation under equity method or recompute the reserves based on fair valuation of associate’s associate. This is because associate’s associate is not my related party and such investment should be fair valued.

Hi Silvia ! Thanks for the article. But may i know reason why under equity method (MFRS 128 Investments in Associates and Joint Ventures) on the date of acquisition the investor records the initial recognition of the investment in an associate or a joint venture at cost, and after the date of acquisition the carrying amount is increased or decreased based on the investor’s share of the profit or loss of the investee (associate or a joint venture).

Hi anonymous, the standard IAS 28 prescribes this and I recommend reading basis for conclusion of IAS 28 – if there is any reasoning for that decision, the basis for conclusion is the best source to read.

Hi Silvia,

I have a question regarding initial recognition. What if the asset contributed to the joint venture is a non-cash asset, what will be the cost of the investment?

Its fair value.

Explained Perfectly covering all aspects in simplifed manner.

Congrats

IAS 27 requires entities to account for investment in subsidiaries, associates and joint ventures in separate statement to use either: cost, or IFRS9 or equity method.

This is very confusing as it does not state when cost method should be used.

I can’t find the answer anywhere !!

Hi Imad, you cannot find the answer because it is YOUR CHOICE. You can use it whenever you choose to in this situation.

How stock dividend is accounted for by an invested who uses the equity method?

Questions, 1) if you are using the equity method, but you acquire the investment, I say, in middle of the year when the investee reports its full year net income, you have to adjust your investment for the full corresponding net income (proportionally to your share) and also considering the time you have owned the investee (6 months for example)?; 2) at the end your investment should have the same value than the investee’s equity plus the goodwill? or other differences are allowed?

Dear Silvia

Where I can find more information/examples with numbers on inter company eliminations made for an associates?

Thank you

Hi Silvia,

If the method used for allocating an investee’s earnings or losses to investors, is the hypothetical liquidation at book value “HLBV” method, how the IFRSs perceive this case?

Many thanks for your relevant and sustainable coaching in IFRSs.

Ahmed

Hi Silvia,

You make accounting enjoyable and easier to understand those accounting standards. Keep up your excellent work

Dear Sylvia,

First – Thank you for your time to make this “IFRS & IAS !!! ” interesting.

I have a question. Please advise …

My company (Employer) had a 30% share in a Company – Invested 150,000

The profit of the Associate is 650,000 – share of this (30%) is 195,000 .

How do I take the Credit and how do I show in the Balance Sheet ?

Dear Silvia,

I have an investment in associate at the end of the reporting period of lets say EUR 250. The share of losses apportioned to my investment equal to EUR 3,500. The standard says that I cannot create a liability for my investment in Associate so my double entry will be DR Share of loss 250 and Cr Investment in Ass. 250. My question is what happens with the rest of the amount to be apportioned as loss of EUR 3,250? And what will happen if after lets say 2 years the Investment in Associate Incurred profits?

Dear Silvia,

I have an investment in associate at the end of the reporting period of lets say EUR 250. The share of losses apportioned to my investment equal to EUR 3,500. The standard says that I cannot create a liability for my investment in Associate so my double entry will be DR Share of loss 250 and Cr Investment in Ass. 250. My question is what happens with the rest of the amount to be apportioned as loss of EUR 3,250? And what will happen if after lets say 2 years the Investment in Associate Incurred profits?

Hi,

Is there a case where dividend distributed exceeds the carrying amount of investment?

Hi, well, I can’t imagine how this can happen unless you booked the impairment previously – in this case, you would probably need to reverse it. Can you explain the other circumstance?

Dear Silvia,

Thanks for the above article!

Could you please suggest the treatment of PURP in case associates sell goods to Parent and goods are still in the Parent’s inventory?

Regards

Deepak

Hi Deepak,

you need to eliminate it in a similar manner as with subsidiary/parent. S.

Silvia, thanks for your articles. I can not understand how it will be after amendment IAS 28 from 2018. How to revalue investment to fair value? Cyrcul 2014-2016

Dear Sylvia,

Please answer to my question……

please…………

When as associate is valued using par 10 of IAS 27, at cost (Exception is used), and in the following year wants to make change in policy and value the associate under IFRS 9. My question is can he do that? And if yes changes must be made retrospectively under IAS 8 or prospectively as per IFRS 9. And if in the years after this change, fair value cannot be reliably measured can he go back at cost??

Hi Silvia,

Keep up the great work!! This is truly IFRS made simple. The question I have is this: Can an investment entity which is public (listed on a stock exchange) elect to value its investments in associates at fair value through profit or loss instead of using the equity method?

Dear Silvia,

I want to know whether Investor’s investment is always agree with the amount of associates Net assets (Investors’ portion). If there is a difference what we can do?

Dear Silvia, You are very helpful!!

I have a question. When as associate is valued using par 10 of IAS 27, at cost (Exception is used), and in the following year wants to make change in policy and value the associate under IFRS 9. My question is can he do that? And if yes changes must be made retrospectively under IAS 8 or prospectively as per IFRS 9. And if in the years after this change, fair value cannot be reliably measured can he go back at cost??

Dear Silvia,

Trust you are well,

Please advise the accounting treatment of the following statement of IAS-28

The additional losses are provided for, to the extent the investor has incurred obligations or made payments on behalf of the associate, to satisfy obligations of associate which the investor has guaranteed or to which the investor is otherwise committed.

Regards,

Well, if you guarantee that you will make some payments on behalf of your associate, you need to make a provision for that. S.

Hi Silvia 🙂

I have a confusion on double entry when there is goodwill or gain on bargain purchase of associate. Would you PLEASE assist me in double entry when the group’s share of net fair value of identifiable assets and liabilities is greater than the cost of investment in associate and vice versa. Debit Entry would be the Cost of investment in associate and what would be the credit entry?

Thank you in advance. 🙂

Hi,

Could you please explain what are the adjustments required if the investee’s reporting date is different from investor’s reporting date?

Hi Gayan, you would need to adjust the investee’s financial statements for the major events (revenues, expenses, acquisition of PPE, etc.) during these 3 months. S.

Hi, do you allow guest posting on ifrsbox.com ? 🙂 Let me know on my email

Hi Mark, yes, I do. Please contact me here. S.

Hi Silvia,

I believe equity method of investment in associate also have intra-group transactions eliminating the investor’s share on the unrealized intra-group profit. (As discussed in the kit) However, I’m not sure if this should be only in the conso fs (investor + subs)? How about in the separate fs of the investor, shall we apply it there as well?

Thank you.

Hi Cy,

it depends on what method the investor applies for its investments in the separate financial statements under IAS 27. If at cost or as a financial instrument under IFRS 9, then no, you don’t eliminate. If using the equity method, then yes. S.

When an associate becomes a subsidiary. How do we treat the shares of profit recorded in previous years?

Do we adjust the same with our retained earnings in the seperate financials so the we are left with our cost?

Thanks for your guidance

thnq so much mam ur notes are really helping me alot.but mam can u please give me an example of how to apply equity method in joint venture practically?

the article is helpful thanks

You transform complex IFRS so simple to understand. You are great

Co A owns land. As part of plans to develop the land, Co A and Co B formed a JV co (joint control), and Co A sells the land to the JV co. The net book value of the land in Co A’s books is much lower than the market value and Co A records a gain in its books. At group level, JV Co will be equity accounted.

In this case, the land value for our share of net assets of the JV co will be at the purchase price which is at market value?

At group level, do we need to eliminate the gain on sales of land by Co A to the JV co for the 50% we owned? Or the gain is considered to be 100% realized at group level?

Have a question. What happens when an associate become a financial instrument i.e. previously held 40% equity interest reduces to 15% by selling 25%.

-Do we need to fair value the remaining investment at fair value.

-How the difference in carrying value (remaining) and fair value is treated.Does this goes to P/L or reserve (assuming the remaining investment is treated as AFS)

You are really great

HI Silvia,

Your Article and explanations are very nice and making our work very easy.

I have one doubt and revel through an example, Company A has 20% shares in its associate company B at a carrying value of 2400(investment 2000 + share of profit of Associate 400), in last date of current year Company A again acquired 60% shares in Company B for 10000. for computation of goodwill how to consider existing 20% investment value ( we Don’t know fare value of Shares). and what is the treatment for current year profits of Company B. Please explain me. Thank you very much.

Dear Kota,

in this case, investment in B stopped being an associate and became a subsidiary. It’s not an easy thing to explain this in a comment, but let me give you a few hints:

– You need to remove the investment in associate first; do it at fair value. Then you “re-acquire it” at fair value, too.

– This “disposal” gives rise to profit or loss from disposal.

– Then, you account for the acquisition of a subsidiary and its total cost is the fair value of previous investment in associate + extra cash (10 000) paid for those additional shares.

Hope it helps!

S.

HI Silvia,

Your Article and explanations are very nice and making our work very easy.

I have one doubt and revel through an example, Company A has 20% shares in its associate company B at a carrying value of 2400(investment 2000 + share of profit of Associate 400), in last date of current year Company A again acquired 60% shares in Company B for 10000. for computation of goodwill how to consider existing 20% investment value ( we Don’t know fare value of Shares). and what is the treatment for current year profits of Company B. Please explain me. Thank you very much.

Hi Silvia.

I was wondering whether a company, having investment in an associate, is liable to account for the investment under equity method in its separate financial statements?

For example, a company A has significant influence in company B, and there is no other company in the group. Will it have to present 2 separate financial statements? One in which investment is presented under IFRS 9 and one (you can call it consolidated) in which investment is presented under equity method? Or is it required to present only one set of financial statements with equity method?

AK

Hi AK,

IAS 27 permits 3 methods of accounting for investments in a separate financial statements and one of them is equity method. It was added in 2014, I think. S.

Thank you so much for this article. It is very helpful for me…. But i have a question that 1st point of exemption that.. The parent is exempted from consolidation….. What does it meant….????

hi, ms.sylvia, do you have any example of a parent who also have an investment in associate? what would be the amount of investment in associate will be presented in the consolidated financial statement? and what will be the eliminating entries for that matter, thanks a lot.

Hi Josh, there are number of examples in the IFRS Kit. But to reply: in the consolidated financial statements, you need to present associate using the equity method as written above. It means that you still present your investment in 1 line only and there are no eliminating entries as in the subsidiary/parent relationship. S.

In your video, “the loss of investee can’t below 0”. If the investment in assoicate company figure is 200, the share of loss of associate company of previous year is 150 and the loss of this year is 100, how do we do in double entries?

Using Equity Method:

Previous year

Dr PL for loss 150

Cr investment in assoicate company 150

This year

Dr PL for loss 100

Cr investment in assoicate company 100

After that two entries, the investment in assoicate company figure will be -50.

You mention that the value of investment in assoicate can be under 0. Will -50 be put as impairment of loss in long term liabilities in Balance Sheet in this year?

Not at all. You simply stop bringing futher losses into consolidated financial statements and keep the investment in associate at 0. It cannot be a liability. S.

You are Wonderful Silvia. I was looking for this answer.

Silvia, is it the same applicable for both IFRS and IFRS for SMEs?

Hi Sylvia,

a question please, on the consolidated level you stop recognizing loss once investment in associate reaches 0, but what happens on the stand alone level of the investor statements if subsidiaries losses exceeded the investment, is an entry recognized by crediting investment till it becomes 0 debiting loss on investment in associate for the same value and for the excess of the loss, creating a liability in F/P and debiting p&L??

Thank Silvia

Now Islamic Finance is developing very fast and Musharakah investment is quite similar to such investment. Can we adopt the same principles?

Regards

Hi Silvia,

Thank you very much for this article. Very informative. Wondering whether this standard applies to accounting for a not-for-profit associate as well?

Hi Ahamed, yes, sure – as soon as the parent or the investor follows IFRS.

Many thanks

Kindly, let me know how the associated company of a subsidiary is consolidated in the books of a parent? For Example, if a Company A Co. has 52% shares in B Co. and B Co. has 30% shares in C Co.

Hi MH

A very late reply

I stand corrected, you first equity account the associate into the subsidiary and then you consolidate the subsidiary(including its share in the associate) into the parent

Very nice. But I had a query. Before using equity method both the investor and invested companies need to have uniform accounting policies. So if the accounting policies are different then necessary adjustments have to be made in investee books before applying equity method?

Hello, vidya,

yes, that’s right, mainly when the differences resulting from different accounting methods are material.

S.

hi Silvia

thank you for your wonderful presentation if you can assist me on IFRS4 and the IAS 39 the different on it thankz

Hi Silivia,

Thanks for yet another article.

I have a query on Joint Venture/ Associate. By what name we call the statement of financial position and Statement of comprehensive income of a publicly listed company with a JV and have no subsidiary?

My understanding is that we cannot add the term “consolidated” to the financial statement as there is no subsidiary company; however we have to follow the equity method for accounting the investment in JV.

Regards,

John

Hi,

You are really great on issues related to IFRS! I always wanted to ask for your time on Derivatives especially, recognition and measurement.

Regards

Hi Silvia,

With start-up expenses axed by IFRS and given that before the advent of IFRS we used to prepare “Statement of Affairs” as opening statement of Balance Sheet necessary to open the books of a new business where we capitalize start-up expenses, is Statement of affairs still relevant? And what happens to start-up costs? I need industry wide practice.

Meanwhile, I want to say your intervention on IFRS issues has truly demystified it and made it user friendly. Please keep it up.

Many thanks and kind regards.

Ibe Nwankwo

Hi Ibe, thank you for your comment. Well, I wrote an article about the similar issue including capitalizing start-up expenses, it’s here: http://www.cpdbox.com/capitalize-ppe-ias16/

The thing is that start-up expenses do not meet the definition of intangible asset (as they are not identifiable, i.e. separable), so they should not be capitalized separately as an asset.

In some cases, they can be added to the cost of PPE (if they relate to the acquisition of that PPE).

Hope it helps!

S.

Wow…. it gives an excellent understanding about IAS 28. Thank you madam 🙂

As excellent as usual , easy to understand and practical

Hi Kachana

Excellent stuff Kachana, thank you

Hi Rich, but it’s my website, article and responses – however, Kachana will be happy 🙂 Silvia

This article is very helpful. I wish i could know you early enough with your articles! Thank you so much

How do we treat unrealised profit in an associate arrangement

Good work silvia I really appreciate your articles.I have a question for you though ,can a Not for Profit organization consolidate the results of a profit making subsidiary.

Regards

Kachana

Hi Kachana, thank you!

To your question: yes, why not? There might be some specifics, like for example, maybe you’ll need to report results by segments in line with IFRS 8. But if you are required to prepare consolidated financial statements under IFRS, this is doable even in your situation. S.

Hi Silvia, I want to know where associate companies come in balance sheet?

Hi Silvia, your work is great! Keep it going.

I would gladly welcome an article on Derivatives, especially classification and subsequent measurement.The issue around when a derivative instrument is net settled and when it is gross settled. I have serious trouble understanding this.

Hi Aubrey,

thank you for your feedback 🙂

Well, there’s no big fuss around the classification and subsequent measurement of derivatives. They are always at FVTPL (OK, some of them are a part of hedge accounting and it’s a little bit different then, but just a little bit).

So they are always measured at FV subsequently.

Thanx and thank you for making IFRS interesting.