During my ACCA studies some years ago I had an amazing tutor. He was very smart, always to the point and on top of that, I simply loved his dry British sense of humor.

When we talked about inventories, he told us a story about an audit assistant performing audit in a big distribution company.

Today, I’m going to write about a few costing methods and this story perfectly fits here, so let me retell it:

This audit assistant was auditing inventories and he just got the excel file with the stock register (list of inventories with their amounts and unit costs).

He looked at the file and noted that there were actually 2 columns for “amount”, so he went straight to CFO and asked:

“Why are there 2 columns with the amount?”

CFO: “Well, the first one is theoretical amount calculated based on movements, and the other one is physical amount counted during the year-end stock count.”

Fair enough, the assistant noted this answer and went back to his room to continue.

Then he noted that indeed, there’s one more column with the differences, so he went back to CFO.

That time, CFO just finished reading the reports from his controller and wanted to get ready for another meeting, but OK, he decided to be polite and invited our assistant to come in.

“What did you do with these differences?”

CFO thought: ‘Well, isn’t that obvious from our trial balance?’, but replied:

“We recognized these differences in profit or loss statement, either as inventory count surpluses or deficits. Deficits within certain pre-determined levels went to cost of sales and remaining deficits went to other expenses.”

Hmmm, the assistant so happy that he didn’t even note that the CFO became slightly annoyed by him coming back and forth and asking simple questions.

Never mind, the assistant studied the inventory records and suddenly, another question popped up.

He immediately ran to CFO’s door, quickly knocked, rushed in and asked:

“What cost formula do you use? FIFO? Weighted average?”

CFO, interrupted at his deserved cup of coffee over another report, went all red and grunted:

“No, we use FOFO.”

“FOFO? What’s that???” puzzled assistant.

“F_CK OFF FIND OUT!!!”

When our tutor finished this story, everybody was laughing out loud. I remember cost formulas very well ever since then.

I really hope that after reading this article, you’ll remember them too!

What are cost formulas?

First, let me describe shortly what the problem is here.

Imagine a company buys 1 000 chocolates for CU 30 each. The journal entry is

-

Debit Inventories: CU 30 000 (1 000*30)

-

Credit Accounts payable: CU 30 000

Then, this company sells 200 chocolates for CU 40 each. The journal entry is:

-

Debit Accounts receivable: CU 8 000 (200*40)

-

Credit Revenues from sale of goods: CU 8 000

Also, the company must reflect the fact that some chocolates left its warehouse. The journal entry is:

-

Debit Cost of sales: CU 6 000 (200*30)

-

Credit Inventories: CU 6 000

In this very basic example, the company knew exactly what amount should have been recognized in cost of sales, because the acquisition cost (purchase price in this case) was CU 30 per chocolate.

But what happens when the company purchases chocolates in batches at different prices?

For example, imagine the company purchased 100 chocolates for CU 31 each, 150 chocolates for CU 32.50 each, then 200 chocolates for CU 29 each, etc.

What is the cost of sales in this case?

That depends on the cost formula selected by the company. So there isn’t just one correct answer.

What does IAS 2 Inventories prescribe?

In fact, the standard IAS 2 Inventories prescribes that when the inventories are:

- Not ordinarily interchangeable; and

- Goods or services are produced and segregated for specific projects,

their cost shall be assigned using specific identification.

This is rather unusual in practice, but it happens, for example when products are exclusive and unique, like jewelry, antiques or some types of automobiles.

When the goods are ordinarily interchangeable (e.g. large volumes of merchandise), then IAS 2 permits using either

- FIFO, i.e. first-in-first-out method; or

- Weighted average method.

The standard IAS 2 Inventories does not permit using LIFO (last-in-first-out). LIFO is permitted by US GAAP though, and maybe also by some other accounting rules.

Now, let’s come back to our chocolates and explain all three cost formulas on chocolate sales and purchases.

Question: Selling Amazing Chocobar

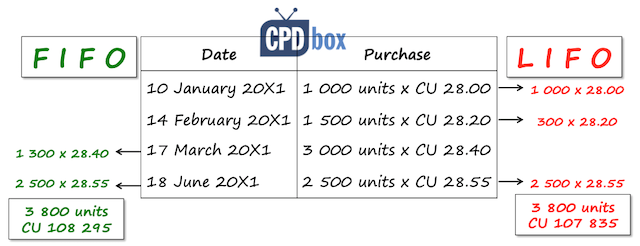

Yummie, candy and chocolate distributor, made the following purchases of new product, Amazing Chocobar during 20X1:

- 10 January 20X1: 1 000 units at CU 28.00 each;

- 14 February 20X1: 1 500 units at CU 28.20 each;

- 17 March 20X1: 3 000 units at CU 28.40 each; and

- 18 June 20X1: 2 500 units at CU 28.55 each.

As Chocobar is a new product and massive advertising campaign is planned after 1 July 20X1, Yummie sold only one batch of 4 200 units of Amazing Chocobar to its biggest customer, for total sales price of CU 159 600. This happened on 2 May 20X1.

Calculate the stock value of Amazing Chocobar in Yummie’s warehouse at 30 June 20X1 (ignore other components of acquisition cost).

Solution

As I have indicated above, the answer strongly depends on the cost formula used.

While we clearly know what amount of inventories arrived to the warehouse at purchases, the cost of inventories dispatched from warehouse at sale must be calculated using one of cost formulas mentioned above.

Also, the total sales price of CU 159 600 is here only to trick you. It is NOT relevant for calculating the value of inventories in the warehouse – it’s a sales price, not a cost.

Regardless cost formula used, we can calculate the number of units of Amazing Chocobar in the warehouse:

1 000 + 1 500 + 3 000 + 2 500 – 4 200 = 3 800 units.

Now let’s use various cost formulas to assign some value (cost) to these 3 800 units.

FIFO (First-in-first-out)

I call this method “chronological”.

The reason is that under this method, you are “selling” the goods from the warehouse in the order in which they are purchased.

In our example, when Yummie sold 4 200 units of Chocobar, we assume under FIFO that Yummie dispatched:

- All units purchased on 10 January 20X1 – 1 000 units at 28.00 each

- All units purchased on 14 February 20X1 – 1 500 units at 28.20 each, and

- 1 700 units (total sold of 4 200 – 1 000 – 1 500) from the purchase of 17 March 20X1 at 28.40 each.

You can calculate the cost of sales at the sale, but that was not a question.

The question was what the balance of Amazing Chocobar stock at 30 June 20X1 is.

When you assume that you sold from the oldest purchases, logically, the most recent purchases remain in the warehouse.

Therefore, you need to go backwards here.

There’s 3 800 units in the warehouse, thereof:

- 2 500 units from the purchase of 18 June 20X1 at CU 28.55 each – that’s CU 71 375; and

- Remaining 1 300 units must come from the purchase of 17 March 20X1 at CU 28.40 each – that’s CU 36 920;

Thus, total value of Amazing Chocobar stock under FIFO at 30 June 20X1 is CU 108 295.

LIFO (Last-in-first-out)

This method is quite similar to FIFO, with one big difference: here, you assume that you sell from the most recent purchases.

As a result, the oldest purchases remain in the warehouse until the stock is sold out.

This is closely linked to the main reason why LIFO is prohibited by IAS 2.

IFRS standards focus heavily on the balance sheet numbers. Every single amount in your balance sheet should reflect current market and economic conditions as much as possible and this is NOT what LIFO does.

Why?

Because, when you put the most recent purchases at most recent prices to cost of sales, and you keep the oldest purchases in your warehouse and your balance sheet, the value of your stock in the balance sheet dates back to your oldest purchases.

In other words, the value of inventories is outdated under LIFO – true mainly for rising prices and slowly moving stock.

Also, LIFO tends to inflate cost of sales.

However, let’s solve our chocolate case by LIFO, too.

While you look at the most recent purchases when determining year-end value of inventories under FIFO, here, you look at oldest purchases.

Plus, you have to think about the sale. At sale, the chocobars’s cost was calculated based on the last purchases available in the warehouse.

Therefore, on 2 May 20X1, 4 200 bars came from the following purchases:

- 3 000 units from the purchase of 17 March 20X1 at CU 28.40 each, and

- 1 200 units from the purchase of 14 February 20X1 at CU 28.20 each.

Thus, 3 800 units remaining in the warehouse at 30 June 20X1 come from:

- 1 000 units come from the purchase of 10 January at CU 28.00 each – which is CU 28 000;

- 300 units come from the purchase of 14 February at CU 28.20 each – which is CU 8 460. Remember, you sold 1 200 units of this purchase on 2 May 20X1;

- Remaining 2 500 units come from the purchase of 18 June 20X1 at CU 28.55 each – that’s CU 71 375.

The total value of Amazing Chocobar stock at 30 June 20X1 under LIFO method is CU 107 835.

This graphical scheme shows the contrast between FIFO and LIFO:

Weighted average

Under weighted average method, the cost of inventories at sale is calculated as weighted average of previous purchases.

Practically, you need to recalculate weighted average at each purchase. Then, when you make a sale, you dispatch the inventories at the most recent weighted average price.

This is illustrated on our example in the following table:

| Date | Purchase | Sale | Stock | Unit cost |

| 10-Jan | 1 000*28.00 = 28 000 | – | 28 000 | 28.00 |

| 14-Feb | 1 500*28.20 = 42 300 | – | 70 300 (28 000+42 300) | 28.12 (70 300/(1 000+1 500) |

| 17-Mar | 3 000*28.40 = 85 200 | – | 155 500 (70 300+85 200) | 28.27 (155 500/5 500) |

| 2-May | – | 4 200*28.27 | 36 751 (1 300*28.27) | 28.27 (as above) |

| 18-Jun | 2 500*28.55 = 71 375 | – | 108 126 (36 751+71 375) | 28.45 (108 126/3 800) |

Please note that:

- The average cost per unit is calculated in the last column. It changes after each purchase.

- After sale on 2 May 20X1, the average cost remains the same. This is logical, as there’s no new purchase affecting average cost.

To sum it up…

We calculated 3 different balances of stock at 30 June 20X1 based on different cost formulas. The results are:

- Under FIFO: CU 108 295

- Under LIFO: CU 107 835

- Under weighted average: CU 108 126

I just remind you that IAS 2 does not permit LIFO.

Just one audit point: it’s much easier to verify the balances of stock when FIFO method is used, as compared to weighted average.

The reason is that while you are able to track latest purchases of certain stock for calculating the value of inventories under FIFO, it can be quite difficult to track all purchases for weighted average.

Do you have any interesting story about your inventories? Please share with us in the comment below. Thank you!