IAS 2 Cost Formulas: Weighted average, FIFO or FOFO?!

During my ACCA studies some years ago I had an amazing tutor. He was very smart, always to the point and on top of that, I simply loved his dry British sense of humor.

When we talked about inventories, he told us a story about an audit assistant performing audit in a big distribution company.

Today, I’m going to write about a few costing methods and this story perfectly fits here, so let me retell it:

This audit assistant was auditing inventories and he just got the excel file with the stock register (list of inventories with their amounts and unit costs).

He looked at the file and noted that there were actually 2 columns for “amount”, so he went straight to CFO and asked:

“Why are there 2 columns with the amount?”

CFO: “Well, the first one is theoretical amount calculated based on movements, and the other one is physical amount counted during the year-end stock count.”

Fair enough, the assistant noted this answer and went back to his room to continue.

Then he noted that indeed, there’s one more column with the differences, so he went back to CFO.

That time, CFO just finished reading the reports from his controller and wanted to get ready for another meeting, but OK, he decided to be polite and invited our assistant to come in.

“What did you do with these differences?”

CFO thought: ‘Well, isn’t that obvious from our trial balance?’, but replied:

“We recognized these differences in profit or loss statement, either as inventory count surpluses or deficits. Deficits within certain pre-determined levels went to cost of sales and remaining deficits went to other expenses.”

Hmmm, the assistant so happy that he didn’t even note that the CFO became slightly annoyed by him coming back and forth and asking simple questions.

Never mind, the assistant studied the inventory records and suddenly, another question popped up.

He immediately ran to CFO’s door, quickly knocked, rushed in and asked:

“What cost formula do you use? FIFO? Weighted average?”

CFO, interrupted at his deserved cup of coffee over another report, went all red and grunted:

“No, we use FOFO.”

“FOFO? What’s that???” puzzled assistant.

“F_CK OFF FIND OUT!!!”

When our tutor finished this story, everybody was laughing out loud. I remember cost formulas very well ever since then.

I really hope that after reading this article, you’ll remember them too!

What are cost formulas?

First, let me describe shortly what the problem is here.

Imagine a company buys 1 000 chocolates for CU 30 each. The journal entry is

-

Debit Inventories: CU 30 000 (1 000*30)

-

Credit Accounts payable: CU 30 000

Then, this company sells 200 chocolates for CU 40 each. The journal entry is:

-

Debit Accounts receivable: CU 8 000 (200*40)

-

Credit Revenues from sale of goods: CU 8 000

Also, the company must reflect the fact that some chocolates left its warehouse. The journal entry is:

-

Debit Cost of sales: CU 6 000 (200*30)

-

Credit Inventories: CU 6 000

In this very basic example, the company knew exactly what amount should have been recognized in cost of sales, because the acquisition cost (purchase price in this case) was CU 30 per chocolate.

But what happens when the company purchases chocolates in batches at different prices?

For example, imagine the company purchased 100 chocolates for CU 31 each, 150 chocolates for CU 32.50 each, then 200 chocolates for CU 29 each, etc.

What is the cost of sales in this case?

That depends on the cost formula selected by the company. So there isn’t just one correct answer.

What does IAS 2 Inventories prescribe?

In fact, the standard IAS 2 Inventories prescribes that when the inventories are:

- Not ordinarily interchangeable; and

- Goods or services are produced and segregated for specific projects,

their cost shall be assigned using specific identification.

This is rather unusual in practice, but it happens, for example when products are exclusive and unique, like jewelry, antiques or some types of automobiles.

When the goods are ordinarily interchangeable (e.g. large volumes of merchandise), then IAS 2 permits using either

- FIFO, i.e. first-in-first-out method; or

- Weighted average method.

The standard IAS 2 Inventories does not permit using LIFO (last-in-first-out). LIFO is permitted by US GAAP though, and maybe also by some other accounting rules.

Now, let’s come back to our chocolates and explain all three cost formulas on chocolate sales and purchases.

Question: Selling Amazing Chocobar

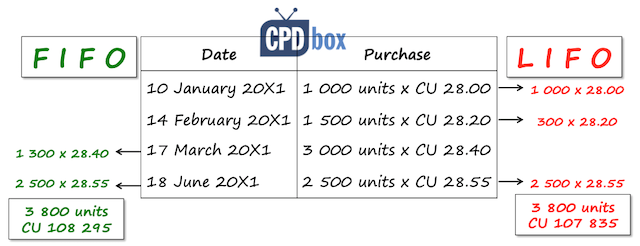

Yummie, candy and chocolate distributor, made the following purchases of new product, Amazing Chocobar during 20X1:

- 10 January 20X1: 1 000 units at CU 28.00 each;

- 14 February 20X1: 1 500 units at CU 28.20 each;

- 17 March 20X1: 3 000 units at CU 28.40 each; and

- 18 June 20X1: 2 500 units at CU 28.55 each.

As Chocobar is a new product and massive advertising campaign is planned after 1 July 20X1, Yummie sold only one batch of 4 200 units of Amazing Chocobar to its biggest customer, for total sales price of CU 159 600. This happened on 2 May 20X1.

Calculate the stock value of Amazing Chocobar in Yummie’s warehouse at 30 June 20X1 (ignore other components of acquisition cost).

Solution

As I have indicated above, the answer strongly depends on the cost formula used.

While we clearly know what amount of inventories arrived to the warehouse at purchases, the cost of inventories dispatched from warehouse at sale must be calculated using one of cost formulas mentioned above.

Also, the total sales price of CU 159 600 is here only to trick you. It is NOT relevant for calculating the value of inventories in the warehouse – it’s a sales price, not a cost.

Regardless cost formula used, we can calculate the number of units of Amazing Chocobar in the warehouse:

1 000 + 1 500 + 3 000 + 2 500 – 4 200 = 3 800 units.

Now let’s use various cost formulas to assign some value (cost) to these 3 800 units.

FIFO (First-in-first-out)

I call this method “chronological”.

The reason is that under this method, you are “selling” the goods from the warehouse in the order in which they are purchased.

In our example, when Yummie sold 4 200 units of Chocobar, we assume under FIFO that Yummie dispatched:

- All units purchased on 10 January 20X1 – 1 000 units at 28.00 each

- All units purchased on 14 February 20X1 – 1 500 units at 28.20 each, and

- 1 700 units (total sold of 4 200 – 1 000 – 1 500) from the purchase of 17 March 20X1 at 28.40 each.

You can calculate the cost of sales at the sale, but that was not a question.

The question was what the balance of Amazing Chocobar stock at 30 June 20X1 is.

When you assume that you sold from the oldest purchases, logically, the most recent purchases remain in the warehouse.

Therefore, you need to go backwards here.

There’s 3 800 units in the warehouse, thereof:

- 2 500 units from the purchase of 18 June 20X1 at CU 28.55 each – that’s CU 71 375; and

- Remaining 1 300 units must come from the purchase of 17 March 20X1 at CU 28.40 each – that’s CU 36 920;

Thus, total value of Amazing Chocobar stock under FIFO at 30 June 20X1 is CU 108 295.

LIFO (Last-in-first-out)

This method is quite similar to FIFO, with one big difference: here, you assume that you sell from the most recent purchases.

As a result, the oldest purchases remain in the warehouse until the stock is sold out.

This is closely linked to the main reason why LIFO is prohibited by IAS 2.

IFRS standards focus heavily on the balance sheet numbers. Every single amount in your balance sheet should reflect current market and economic conditions as much as possible and this is NOT what LIFO does.

Why?

Because, when you put the most recent purchases at most recent prices to cost of sales, and you keep the oldest purchases in your warehouse and your balance sheet, the value of your stock in the balance sheet dates back to your oldest purchases.

In other words, the value of inventories is outdated under LIFO – true mainly for rising prices and slowly moving stock.

Also, LIFO tends to inflate cost of sales.

However, let’s solve our chocolate case by LIFO, too.

While you look at the most recent purchases when determining year-end value of inventories under FIFO, here, you look at oldest purchases.

Plus, you have to think about the sale. At sale, the chocobars’s cost was calculated based on the last purchases available in the warehouse.

Therefore, on 2 May 20X1, 4 200 bars came from the following purchases:

- 3 000 units from the purchase of 17 March 20X1 at CU 28.40 each, and

- 1 200 units from the purchase of 14 February 20X1 at CU 28.20 each.

Thus, 3 800 units remaining in the warehouse at 30 June 20X1 come from:

- 1 000 units come from the purchase of 10 January at CU 28.00 each – which is CU 28 000;

- 300 units come from the purchase of 14 February at CU 28.20 each – which is CU 8 460. Remember, you sold 1 200 units of this purchase on 2 May 20X1;

- Remaining 2 500 units come from the purchase of 18 June 20X1 at CU 28.55 each – that’s CU 71 375.

The total value of Amazing Chocobar stock at 30 June 20X1 under LIFO method is CU 107 835.

This graphical scheme shows the contrast between FIFO and LIFO:

Weighted average

Under weighted average method, the cost of inventories at sale is calculated as weighted average of previous purchases.

Practically, you need to recalculate weighted average at each purchase. Then, when you make a sale, you dispatch the inventories at the most recent weighted average price.

This is illustrated on our example in the following table:

| Date | Purchase | Sale | Stock | Unit cost |

| 10-Jan | 1 000*28.00 = 28 000 | – | 28 000 | 28.00 |

| 14-Feb | 1 500*28.20 = 42 300 | – | 70 300 (28 000+42 300) | 28.12 (70 300/(1 000+1 500) |

| 17-Mar | 3 000*28.40 = 85 200 | – | 155 500 (70 300+85 200) | 28.27 (155 500/5 500) |

| 2-May | – | 4 200*28.27 | 36 751 (1 300*28.27) | 28.27 (as above) |

| 18-Jun | 2 500*28.55 = 71 375 | – | 108 126 (36 751+71 375) | 28.45 (108 126/3 800) |

Please note that:

- The average cost per unit is calculated in the last column. It changes after each purchase.

- After sale on 2 May 20X1, the average cost remains the same. This is logical, as there’s no new purchase affecting average cost.

To sum it up…

We calculated 3 different balances of stock at 30 June 20X1 based on different cost formulas. The results are:

- Under FIFO: CU 108 295

- Under LIFO: CU 107 835

- Under weighted average: CU 108 126

I just remind you that IAS 2 does not permit LIFO.

Just one audit point: it’s much easier to verify the balances of stock when FIFO method is used, as compared to weighted average.

The reason is that while you are able to track latest purchases of certain stock for calculating the value of inventories under FIFO, it can be quite difficult to track all purchases for weighted average.

Do you have any interesting story about your inventories? Please share with us in the comment below. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

103 Comments

Leave a Reply

Hi Silvia,

I doubts if we can say “While you look at the most recent purchases when determining year-end value of inventories under FIFO, here (LIFO), you look at oldest purchases”. It is completely true for FIFO, but it wouldn’t be the case always in LIFO.

In the situation when the company have more than one sale transaction during the period, the delivery could be from the most recent purchase as on the date of sale, hence it does not follow an order unlike FIFO. So there are possibilities that the some part of the oldest purchases would be sold before all of the stock in the warehouse is sold out. So in those situations, it wouldn’t be appropriate to pick the oldest purchases to arrive at the value of inventory in LIFO.

However in FIFO, we can always say that the remaining inventories as on the year end would definitely be the inventories from the most latest purchases irrespective of the number of sale transactions in between.

Arun Augustine

kunnelarun6@gmail.com

Yes, you are of course right, thank you! What I meant to say was to look at oldest purchases still in stock. Best, S.

Is it possible to value finished goods as per FIFO. because we have to add the attributable fixed costs to cost of manufacturing. But if i do such apportionment, it will be weighed average cost method

Thank you for this

Thank you Silvia M. really appreciate

wonderfully explained thanks a ton

Hi Sylvia.

I’m so grateful I came across your website. its very helpful

anyways but would the decision by only FIFO and WAC restrict the possibility of presenting higher quality and more credible financial statements?

need help on that part please.

*decision by IFRS* (correction)

Dear Silva,

I am a member of your IFRSbox, but I am not an accountant. So sorry if I ask you a simple question (which may lead to a “FOFO” feedback 🙂 ). I am a property valuer and I am to give an estimation on market value of an apartments-for-sale building (or fair value of inventory in accounting language). Revenue is recognized on handover date when the construction is completed; however, the building is still under construction as at valuation date. In other words, no apartment has been handed over to the home-purchasers and no revenue has been recognized. The developer has collected cash from apartment buyers since 2014. What I am doing to arrive at fair value of the whole building are as follows:

1. Valuation date is 2018 (year 0), historical year 2014 to 2017 are labeled as Yr (-5) to Yr (-1).

2. Add back all of the collected amount of sold out apartments to reflect full value of the building since no apartment has been handed over, no COGS and revenue have been recognized.

3. Forecast NRV (= estimated market selling price – est. cost to completion – sale & marketing expense) for the unsold apartments

4. Apply a discount rate to derive NPV of the above cashflow, also the NRV of inventories.

I am considering two cases of discount factor:

– Case A (Yr; Discount factor), apply 1.0 for all historical discount factor: (Yr-5; 1.0) to (Yr-1; 1.0), (Yr0; 1.0), (Yr1; 0.9), (Yr2; 0.8), etc.

– Case B (Yr; Discount factor), apply Future Value, >1.0 for all historical discount factor: (Yr-5; 1.5) to (Yr-1; 1.1), (Yr0; 1.0), (Yr1; 0.9), (Yr2; 0.8), etc.

A wrong discount factor approach will result in over-estimate or under-estimate the value. But I do not know which one is more accurate… I currently think Case A is more relevant since the surplus cash e.g by depositing the cash collected from home purchasers to the bank has ready been transferred to cash in balance sheet and financial income in P&L; so we do not need to reflect FV of the historical cash received?

I would be much grateful to hear your advice,

Thanh Hung,

Hi Silvia,

Thanks for the knowledgeable article.

I am working in a pharmaceutical organisation which uses FEFO (First expiry, First out) for the execution of Stock and same the inventory management system is accounting for.

so basically our organisation is valuing the inventory batch wise. is such practice acceptible under IAS 2? If we don’t use FEFO method for execution then expiry ratio will increase but note in the FS is FIFO.

Your input is required.

Thank.

Shafqat

Hi Silvia,

I am really grateful to you.

I appreciate the great help that you offered to us.

Hello! I have different types of Inventories. One of them is fuel and oil products. Can I use for this particular type of Inventories (lower of cost and NRV model) and for the rest of Inventories the cost model of measurement?

Thanks

George

Dear Silvia,

I was an international student from Japan and studied financial accounting for a bit in Northern California. I stumbled on your website, and it’s very interesting to read your articles. It’s like a real page turner that I cannot put down!

Out of inventory valuation methods, which one would be preferable to small businesses in the States? Compared with the small businesses, most of the small businesses in Japan prefer Latest Purchase Price method because it is pretty easy to use that method.

Hi Silvia, I recently faced this issue on disclosure, as the standard required us to disclose “inventories recognised as an expense”. I always thought it should be equal to cost of sales, but it doesn’t seem that’s the case all the time. Could you please enlighten me? Thank you!

Dear Silvia, thank you very much for brilliant job!

Could you clarify: what accounting treatment is for storage expenses of raw material after delivery it from suppliers? ? When we hold oil (coal/ore) for production petrol (steel) in warehouse should we post related expenses to work in progress (other fixed cost and then allocate it to cost of unit produced) or directly to P/L expenses?

And second question please.

In your article you give the example of cost formula for measurement of inventory without conversion. Could you explain using numerical example measurement technique – standard costs, if difference there is between actual and normal production value?

Thank you very much.

Dear Olena,

1) Storage expenses – in general, storage expenses are recognized in profit or loss, but there is an exception when the storing in intermediary warehouse (WIP) is inevitable in the production process. The storage of raw materials that did not enter the production process is expensed in P/L.

2) OK, I’ll try to do it, but in some of my future articles. It depends strongly on the amount of the difference. If there is no significant difference, then you do not care that much about it and possibly revise the “cost card” or the formula of calculating your standard cost. If there is a difference of a significant nature, then it depends. If the production was abnormally high, you cannot overstate inventories and therefore, you need to reduce allocation (correct your standard cost) and adjust the cost of inventories. When production is lower than planned or idle, there will be some unallocated costs – you need to expense them in profit or loss. Hope it answers the question. S.

Thanks Silvia…. you made learning very easy and fun with your descriptive and highly illuminating explanations. Profoundly grateful for this and many more.

Dear Silvia,

If I receive some free inventory (for normal sale purpose)along with normal purchase then how this has to be accounted for. My Concerns:

1. If we record the free goods at zero value then it will reduce average cost of the inventory over a period of time.

2. Sale person can offer more discount if he is not aware of the situation by seeing the big difference between Selling Price and Cost Price.

3. In case I want to sale my business I can not claim more than average price. Or in case of loss I will be compensated only for the average cost (reduced average cost due to zero value goods)

Keeping in view is it correct to show the zero value goods at last purchase price and adjust the amount in cost of goods sold.

Thanks

Hi Rohit, I replied that question below an article about discounts. S.

Thanks useful lesson my prof. And easy to understand.

Hi Silvia

Very good explanation about the inventory valuation.

Please let me know how is the provision for obsolete items in inventory.

Thanks

Roshan

Thankx For Explanation

Thank you for explanation with story.

Very well said. Thanks for the story. Really got both knowledge and fun. Thanks again.

Thanks very much mom for your help,may God bless you

Super funny story, had an excellent time ready your lectures as always !

Keep on !

Hi!Silvia

very good explanation about the inventory valuation. thanks you..

what if a company use standard price for issuing stock for manufacturing and how do we adjust the stock to reflect the correct value in balance sheet?

Madam,

The incident was really fun of professionals. However, the beginners everybody should understand.

The inventory presentation here of you is straight and clear.

Thank you.

High regards

Truly speaking I am ACCA finalist but still IAS 2 was confusing for me and the reason is I was absent that day when the tutor was teaching IAS 2. Thanks alot Silvia.

Dear Silvia,

Thanks for the simplified explanation. You have just helped a soul down here.

Appreciate

Hi Silvia, Thank you for the great article on inventory. Coudl you kindly tell us what is meant by ” Cost of inventory recognised as expenses” in the Standard, and how to account for this if there is provison for impairment in inventory?

Thank you Silvia – very interesting reading.

Would you have similar “boxes” for Business Analysis which I am undertaking next June (ACCA P3)?

I used your subscription for the P2 ACCA exam and found it extremely useful.

Thank you.

Thanks for sharing your knowlegde!

I Really like IFRSBox.

The story made me laugh!

good ideas,, thks

Dear Salivia,

Thanks for the Simplified explanation, I would heartily like to write an article relates to the bank reconciliation; banks in general and Nostro & Vostro Accounts in particular,

Thanks

What about the case of periodic inventory or perpetual inventory

Yes, Helal, there are small differences. The above illustrations are more for perpetual inventory system, as periodic inventory systems are not really used by bigger companies, but are OK for smaller ones. S.

thanks for the story and knowledge

Thanks so much since I started reading your articles that you sent to me am now appreciating the IFRS.

i like your name. And sure Silvia’s been good.

Awesome, focused on the key points. Thanks a lot

Great article , thanks for the knowledge and story illustration.

Thank you for this beautiful article

Hi Silvia, Would you mind telling us what accounting treatments and journal entries should be there if a write down in the value of the inventories is to be made?

Hi Hamilton,

Debit Profit or loss / Credit Inventories (maybe some valuation adjustment account).

In some companies, write down within certain limit can enter the cost of sales, but everything else is reported in some separate account. S.

Hi Silvia, With the write down in the inventory charged to profit or loss as you advised, shall such amount be included in the ” Cost of sales” or simply in the “Adminstrative & other operating expenses?

The write down of inventories to NRV should ideally be posted to cost of sales.

Good job in deed silvia. With your dedicated good job on ifrs ; I keep growing firm to understand the practical applications of the standard . Keep it up

good article well done#####

Lot of thanks for the useful article.

Hi,Many Thanks for the useful article.I highly appreciate your commitments to deliver your effort to all who are wish to earn about IFRS.

Hi Silvia, sometimes a simple standard may have a lot of unknown/unclear areas. Thanks for this article.

I am bit confused about use of standard or retail cost Vs FIFO and WAC. Standard costing or retail are some alternative methods for FIFO or WAC? Could you clarify their relevance? Thanks

powerful…..the story just absorbed me and the knowledge flush in….. keep it coming through

cheers

Emmanuel

Very interesting. Thanks always for sharing knowledge

it is excellent story and helpful topic

Awesome, the presentation is quite appreciated, keep up the good job silvia

This was indeed an eye opener. Thanks for refreshing our memory.

This is great! Great story and good knowledge. Thanks Silvia. 🙂

Thanks for the useful article. Can you please explain me more on inventory provisioning. Is it ok to use general provision for inventory

Awesome! Thanks for both the story and the knowledge

Thanks for your efforts.

Thanks, Youssef, for your article

I thought that I am the author, but thank you, Youssef! 🙂

lol haha. Thank you Silvia for the article 🙂