How to calculate deferred tax with step-by-step example (IAS 12)

Deferred tax is not a new concept – however, it is the concept quite misunderstood by many.

Well, first of all – deferred tax is NOT a tax to be paid.

Instead, it is an accrual for tax, working similarly as any other accrual or even a provision.

The next confusing thing about the deferred tax is the tax base. How to determine it?

In this article, you will learn:

- Review of the rules related to deferred tax in line with IAS 12 Income Taxes

- How to understand the deferred tax: what it is and what it is NOT

- Example illustrating the basic concept of the deferred tax

- Tax base with examples

- Video lecture and further reading

Deferred tax in IAS 12 Income Taxes

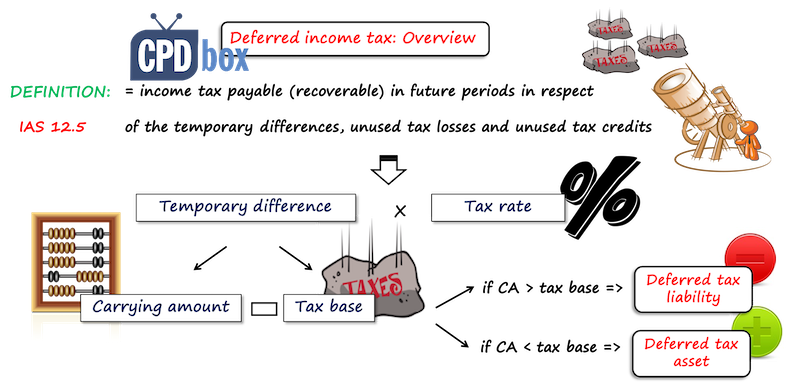

The official definition says that the deferred tax is an income tax payable (recoverable) in future periods in respect of the temporary differences, unused tax losses and unused tax credits (IAS 12.5).

Deferred tax calculation is as follows:

- Temporary difference, determined as

- Carrying amount of an asset or a liability, less

- Its tax base – more on this a bit later,

- The income tax rate

Multiplied with

Depending on the character of a temporary difference, the deferred tax asset or liability arises:

- If the carrying amount is greater than the tax base, then there is a taxable , temporary difference resulting in a deferred tax liability;

- If the carrying amount is smaller than the tax base, then there is a deductible , temporary difference resulting in a deferred tax asset.

And, this is applicable to both assets and liabilities, but only if you view a liability as an item with negative carrying amount. Just as an example: when you recognize a provision of 500 000 CU, then its carrying amount is in fact -500 000, because it is a liability.

If you need to revise the rules in IAS 12 in more detail, please see this link.

Return to top

How to understand deferred tax: what it is and what it is not

The deferred tax is NOT a tax that will be paid in the future.

Instead, it is an accrual (or a provision) for tax, because its purpose is to show the tax effect of some transaction in the same period as the related deductible expense or taxable income occur.

This is the same as in accrual principle – to recognize the expense in the period when the service was consumed, not when it was paid for.

Example: Understanding the deferred tax

On 1 January 20X2, the Company lent 100 000 CU to its subsidiary on 3% interest. The loan will be repaid on 1 January 20X3, together with interest. In 20X2, the Company recognized interest revenue of 3 000 CU, but it will pay taxes from that revenue in 20X3 when the cash arrives.

Show effects of this transaction on profit or loss in both years. Current income tax rate = 20%.

Solution: Basics deferred tax

Let’s take a look at how the interest income and the related income tax affects profit or loss:

The Company needed to make an accrual for interest revenue in 20X2, because the interest was earned for loan in 20X2. However, the same interest was taxed only in 20X3, when it was received from the borrower.

The journal entries are as follows:

- In 20X2:

- To recognize an interest accrual revenue:

- Debit Deferred interest revenue: 3 000;

- Credit P/L – Interest revenue: – 3 000

- To recognize an interest accrual revenue:

- In 20X3:

- The receipt of the loan repayment with the interest:

- Debit Bank account: 103 000

- Credit Loan receivable: – 100 000

- Credit Deferred interest revenue: -3 000

- The income tax on interest revenue:

- Debit P/L Current income tax (20% of 3 000): 600;

- Credit Bank account (or as appropriate, e.g. current income tax liability): -600

- The receipt of the loan repayment with the interest:

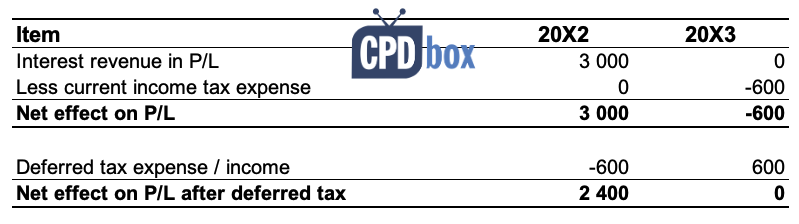

As you can see, in the year 20X2, the net effect of the transaction on profit or loss is the full 3 000 CU, and the net effect of the same transaction on 20X3 profit or loss is – 600 CU being the tax on interest.

And, that’s not right.

This is exactly the reason why we need to recognize the deferred tax.

How?

Well, as mentioned above, the deferred tax is calculated as a difference between the carrying amount of an asset/liability and its tax base, multiplied with the appropriate tax rate.

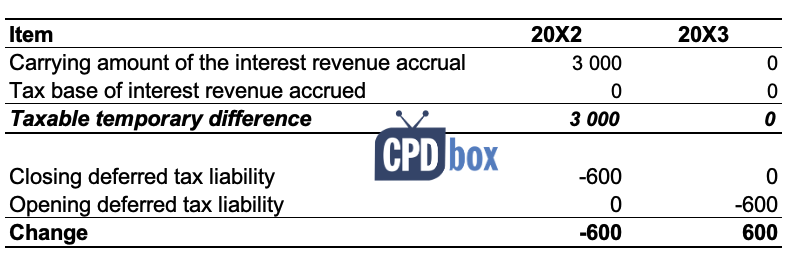

In our example, we will take a look at the interest revenue accrual, which is an asset in the statement of financial position.

Its carrying amount is 3 000 CU, its tax base is zero (please see below for further explanations).

Therefore, there is a temporary taxable difference of 3 000 CU, and if we apply the tax rate of 20%, we get the closing deferred tax liability (DTL) of 600.

The journal entry to recognize this DTL in 20X2 is:

- Debit P/L – deferred tax expense: 600;

- Credit Deferred tax liability: -600.

In 20X3, when the transaction is closed, our closing deferred tax liability is 0, because there is no interest revenue accrual, or so. Therefore, we need to recognize the change in the deferred tax in 20X3 from -600 to zero as follows:

- Debit Credit Deferred tax liability: 600;

- Credit P/L- Deferred tax income: -600.

Here’s the table summing this all up:

And, when we bring the deferred tax expense/income to the overall calculation of the effects of the transaction, it looks like this:

Here you can clearly see that the deferred tax is indeed an accrual for tax, and with the help of deferred tax, we are showing the tax effect of the transactions together with the transactions.

Without it deferred tax, the tax effect is in a different year than the transaction itself, due to different tax rules.

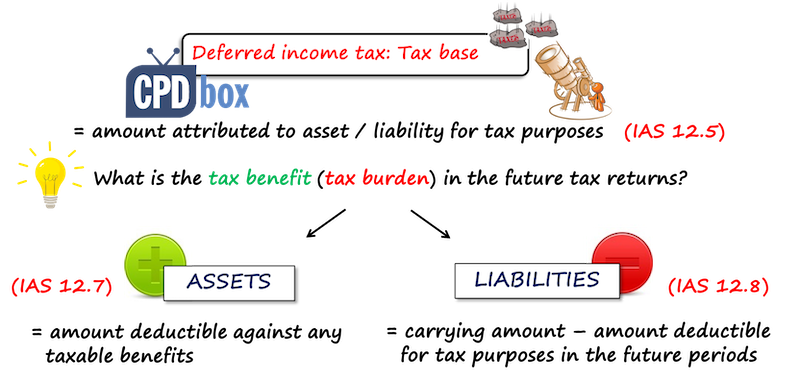

Tax base: How to determine it?

According to IAS 12.5, the tax base in the amount attributed to an asset or a liability for tax purposes.

The following question helps you understand it: “What is the tax benefit or the tax burden of an asset or a liability in the future tax returns?”

Let’s break this down.

Tax base of assets

For assets, the tax base is the amount deductible against any taxable benefits – please refer to IAS 12.7.

However, we need to ask: “What’s left in the pocket for the future tax deductions?”

It’s always better to illustrate those concepts on examples:

Example 1: Capitalized software development

In 20X2, Company paid 30 000 CU for the development of software (all included in intangible assets, not yet amortized). The tax law permits to deduct these expenses when paid.

So, what’s left in the pocket for future tax deductions in relation to the capitalized software development?

The cost of capitalized development is 30 000, and we need to deduct the amount that we have already claimed in tax return when paid – which was the full 30 000.

As a result, there is nothing left for future tax deductions, and the tax base is zero.

(for full calculation of the deferred tax, please see the video below).

Example 2: Depreciated car

Acquisition cost of a car was 20 000 CU in 20X1. The Company uses straight-line depreciation method, useful life is 5 years. The tax law permits to deduct 25% of car’s cost per year (over 4 years in total). Calculate the tax base at the end of 20X2.

The car’s tax base at the end of 20X2 is:

- The cost of 20 000;

- Less the amount already deducted in tax returns in 2 years of 20X1 and 20X2: 2*25%*20 000 = 10 000

So, the tax base of that car at the end of 20X2 is 10 000 – this is exactly the amount left for the future tax deductions.

(for full calculation of the deferred tax, please see the video below).

Tax base of liabilities

The tax base of a liability is its carrying amount less amount deductible for tax purposes in the future – please refer to IAS 12.8.

The easy question to ask: What can you NOT deduct in the future for tax purposes?

Example: A provision

In 20X2, Company recognized a provision of 500 000 CU for the warranty repairs. The tax law permits deducting the expenses for warranty repairs only when they are paid. No repairs have been made in 20X2. Calculate the tax base at the end of 20X2.

The provision’s tax base at the end of 20X2 is:

- Carrying amount of the provision: -500 000; less

- Amount deductible for the tax purposes in the future: -500 000

The difference between those two amounts is the amount that you can NOT deduct in the future for tax purposes – in this case zero, because we can deduct it all.

Therefore, the tax base of this provision is zero.

(for full calculation of the deferred tax, please see the video below).

Further reading and the video

If you wish to dig deeper in this topic, here’s the list of recommended articles:

- Deferred tax – the only way to learn it

- Unconventional guide to tax base

- Summary of all free lectures on IAS 12 Income taxes here on CPDbox

You can watch the video lecture on How to calculate deferred tax here:

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

10 Comments

Leave a Reply

Thank you for the understandable explanation. The examples were clear making it easier to understand

Very well presented

Thanks This is very useful

Very informative…Thank you

Thank You

Could you help me with a particular item in P&L (loss or gain on exchange )

For Parent Company it is taxable on realized bases

For the Subsidiary abroad it is taxable on non realized bases

For Consolidation purposes, Should the Subsidiary book a deferred tax

Hi Lino,

I don’t know the specifics of this item, but in general – if it is not eliminated upon consolidation, then yes, book a deferred tax and keep it there in consolidation, because those deferred taxes are usually settled separately by the subsidiary from the parent.

Hi Silvia – this is so enlightening

Quick question – why is the tax base for liabilities different to assets? I can’t clearly see it

it appears to be: asset fair value less the allowance already claim for tax purposes while liabilities are: liabilities fair value less what is left to be claim for tax purposes (so the opposite of asset). I can’t see why it would be liability carrying amount less what is left to be claimed for tax

Well, those are the rules in IAS 12.7 and 8. – and, they are quite logical, since the assets and liabilities do not work the same way. Please refer here for more details about the tax base, this article is very detailed.

Thanks Silvia