ECL model under IFRS 9 explained: Simple walkthrough with examples

Last update: 2026

What you will find in this guide:

1. Free VIDEO lecture: IFRS 9 ECL model explained: Simple walkthrough with examples

2. What is the IFRS 9 ECL model and when does it apply

3. What does “expected credit loss” actually mean

4. What do the rules in IFRS 9 say? (general vs simplified approach)

5. Can one entity apply both models?

6. How to apply simplified approach

- 6.1 How to group the financial assets?

- 6.2 Forward-looking information: a core requirement, not an add-on

- 6.3 How to get the default rates?

7. Example: Impairment of trade receivables under IFRS 9

8. Further reading + ECL for Accountants course

1. IFRS 9 ECL model explained: Simple walkthrough with examples (free VIDEO lecture)

Before going into the calculation details below, this short video shows a simple walkthrough of the IFRS 9 ECL model and how the pieces fit together.

2. What is the IFRS 9 ECL model and when does it apply

IFRS 9 introduced the expected credit loss (ECL) model to replace the old incurred loss approach.

The core idea is simple: credit losses should be recognised based on expected defaults, not only after a default has already occurred.

The ECL model does not apply to all financial assets. It applies mainly to debt-type instruments, such as loans, trade receivables, lease receivables and certain contract assets. Equity instruments and derivatives measured at fair value are outside the scope of IFRS 9 impairment.

In this article, the focus is primarily on trade receivables and the simplified approach. However, the underlying logic of the ECL model is the same across different asset types.

3. What does “expected credit loss” actually mean

An expected credit loss is not a single worst-case scenario.

It is a probability-weighted average of possible credit losses, where each outcome is weighted by the likelihood of default.

In practice, this means that an impairment allowance can arise even if customers are currently paying on time. The model captures the risk of future default, not only losses that have already materialised.

This logic is central to understanding IFRS 9. Once it is clear, the mechanics of the model and the use of provision matrices become much easier to follow.

Return to top

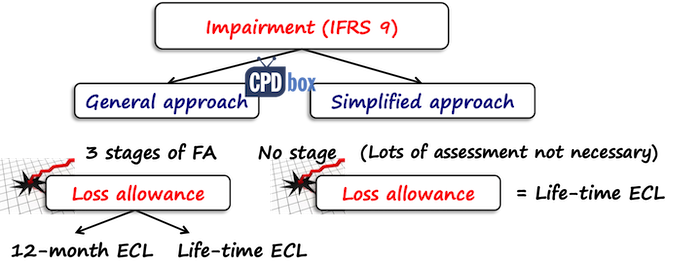

4. What do the rules in IFRS 9 say? (general vs simplified approach)

IFRS 9 requires you to recognize the impairment of financial assets in the amount of expected credit loss.

In fact, there are 2 approaches for doing so:

- General approach

In general approach, there are 3 stages of a financial asset and you should recognize the impairment loss depending on the stage of a financial asset in question.Thus, the impairment loss is either in the amount of a 12-month expected credit loss (ECL) or a lifetime expected credit loss (ECL).You can read more about the general approach here.There are a lot of implementation troubles and challenges, for example:

- How do you determine in which stage the financial asset is?

- How do you determine when the credit risk in some financial asset has significantly increased?

- How do you calculate 12-month ECL and lifetime ECL?

- How do you get and update your inputs into the ECL calculations?

Therefore, IFRS 9 permits an alternative for some type of financial assets:

- Simplified approach

In simplified approach, you don’t have to determine the stage of a financial asset because the impairment loss is measured at lifetime ECL for all assets.This is great news because lots of troubles simply disappear.

However, let me warn you that the simplified approach is not for everybody and even if it’s simplified, you still need to make some calculations and effort.

Who can apply simplified approach?

OK, that’s not the best question in the world, because everybody can apply simplified approach.

Type of financial asset is more important here.

You have to apply simplified approach for:

- Trade receivables WITHOUT significant financing component, and

- Contract assets under IFRS 15 WITHOUT significant financing component

For these two types of assets you have no choice – just apply simplified approach.

On top of that, you can make a choice for:

- Trade receivables WITH significant financing component,

- Contract assets under IFRS 15 WITH significant financing component, and

- Lease receivables (IAS 17 or IFRS 16)

For these three types of financial assets, you can apply either simplified approach or general approach.

5. Can one entity apply both models?

Yes, of course – but not to the same type of financial asset.

Take a bank, for example.

Banks usually provide lots of loans and under IFRS 9, they have to apply general models to calculate impairment loss for loans.

But occasionally, banks can have other financial assets, too.

For example, they may rent redundant offices and have lease receivables.

Or, they can provide advisory services and charge fees for that – thus they can have typical trade receivables.

For these types of assets, the same bank can apply simplified approach.

6. How to apply simplified approach?

As written above, under simplified approach, you measure impairment loss as lifetime expected credit loss.

IFRS 9 permits using a few practical expedients and one of them is a provision matrix.

What is a provision matrix?

Simply said, it is a calculation of the impairment loss based on the default rate percentage applied to the group of financial assets.

Here, we have 2 important elements:

- Group of financial assets

- Default rates

Let’s break it down.

6.1 How to group the financial assets?

When you are using provision matrix for simplification, you still need to be as close to reality as possible.

Therefore, before applying any loss rates, you should group your financial assets first.

Segment them.

The reason is that all trade receivables do not necessarily share the same characteristics and therefore, it would not be reasonable to put them into the same pocket.

How to group them?

It depends on what factors affect the repayment of your receivables.

Maybe you noted that your retail customers (individuals) are less reliable and slower in payments than your business customers (companies).

Therefore, your segments or groups would naturally be retail customers and business customers.

Or, maybe you sell in a few geographical regions and you noted that customers from the capital city pay more reliably than customers in the rural areas (maybe it has something to do with unemployment rate…)

So, your segments would be customers from cities and customers from countryside.

I think you get the point – you should select the grouping of your trade receivables (or other financial assets in questions) depending on your circumstances.

Just a few suggestions for segmenting:

- By product type;

- By geographical region;

- By currency;

- By customer rating;

- By dealer type or sales channel;

etc.

The important point here is that the customers within one group should have the same or similar loss patterns.

6.2 Forward-looking information: a core requirement, not an add-on

Before looking at default rates, one important point must be stressed.

IFRS 9 requires expected credit losses to reflect reasonable and supportable forward-looking information. This requirement applies regardless of how default rates are determined.

Whether probabilities of default are derived from transactional history or from external benchmarks, entities must assess whether those rates reflect current and expected economic conditions and adjust them if necessary. Forward-looking information is therefore an integral part of the ECL model, not an optional overlay.

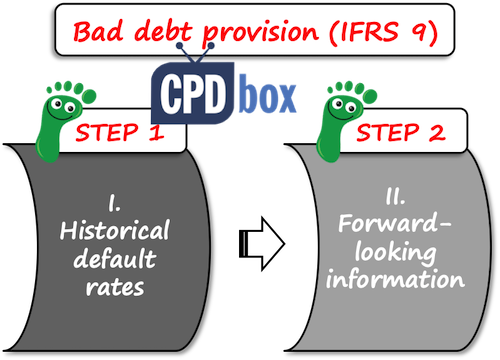

6.3 How to get the default rates?

Remember – do NOT just trump the default rates up, just like auditors from the intro of this article.

You should really calculate them based on your own data.

IFRS 9 says that you should:

- Derive the default rates from your own historical credit loss experience; and

- Adjust them for forward-looking information.

Historical default rates

First, you need to analyze the historical credit losses.

How?

You should take the appropriate period of time and analyze which portion of trade receivables created during that period went default.

Just be careful when selecting the appropriate period.

It should not be too short in order to make sense and it also should not be to long because market changes quickly and long period might incorporate market effects that are no longer valid.

I recommend selecting one or two years.

Then you are going to select the time buckets, or periods when the receivables were paid.

Finally, you would calculate the default rate for each bucket.

No worries if this seems too unclear – you can find the illustrative example below.

Forward-looking information

Once you have your historical default rates, you need to adjust them by the forward-looking information.

What is it?

They are all information that could affect the credit losses in the future, for example macroeconomic forecasts of unemployment, housing prices, etc.

You should adjust historical default rates for the information that is relevant for your financial assets.

For example, let’s say the telecom company has 2 segments of receivables:

- Retail customers, or individuals and for this group, unemployment rates are important factor affecting the payment rate.

If unemployment goes up, the credit quality of trade receivables to retail customers worsens. - Business customers: for this group, GDP (gross domestic product) and inflation rate are important factors in this particular country.

How to incorporate the forward-looking information?

When there is a linear relationship between the macroeconomic factor (i.e. unemployment rate) and the input (i.e. increase/decrease in collection of receivables), then the incorporation is quite simple.

In this case, you need to observe what effect has the change in the parameter on your default rates and make simple adjustment (see illustration below).

However, when the relationship is not linear, then the adjustment might require some modeling using either Monte Carlo simulation or other similar methods.

Return to top

7. Example: Impairment of trade receivables under IFRS 9

ABC wants to calculate the impairment loss of its trade receivables as of 31 December 20X1. ABC’s policy is to give 30 days for the repayment of receivables.

Note: This is an important point – 30 days credit period means that these receivables have NO significant financing component and therefore, you don’t have to worry about the present values.

The aging structure of trade receivables as of 31 December 20X1 is as follows:

| Days after issuing invoice | Amount outstanding |

|---|---|

| Within maturity (0-30 days) | 800 |

| 31-60 days | 350 |

| 61-180 days | 280 |

| 180-360 days | 170 |

| > 360 days | 100 |

| Total | 1 700 |

ABC decided to apply the simplified approach in line with IFRS 9 and calculate impairment loss as lifetime expected credit loss.

As a practical expedient, ABC decided to use the provision matrix.

First, ABC needs to calculate historical default rates.

In order to have sufficient historical data, ABC selected the period of 1 year from 1 January 20X0 to 31 December 20X0.

During this period, ABC generated sales of CU 20 000, all on credit.

Then, we can split the whole analysis process into a few steps.

Step 1: Analyze the collection of receivables by the time buckets

ABC needs to analyze when the receivables were paid and sort them out into table based on number of days from creation of invoice until the collection of the receivable:

| When paid? | Paid amount | Paid amount (cumulative) | Unpaid amount |

|---|---|---|---|

| Within maturity (0-30 days) | 7 500 | 7 500 | 12 500 |

| 31-60 days | 6 800 | 14 300 | 5 700 |

| 61-180 days | 3 000 | 17 300 | 2 700 |

| 180-360 days | 2 200 | 19 500 | 500 |

| > 360 days | 500 = write-off | 19 500 | 500 = write-off |

| Total | 20 000 | n/a | n/a |

Notes:

- The amount of CU 500 in the column “Paid amount” for > 360 days represents in fact defaulted, unpaid amount.

- Paid amount cumulative is calculated as paid amount in certain time bucket plus paid amount in the previous bucket, i.e. cumulative paid amount in 31-60 days is calculated as 6 800+7 500. The exception is > 360 days – here, we can’t include CU 500 because it is not paid.

- Unpaid amount in the last column = total of 20 000 less cumulative paid amount.

Step 2: Calculate the historical loss rates

Then, ABC can calculate the historical default loss rates as the loss amount of CU 500 divided by the amount unpaid (outstanding) at the end of each time bucket:

| When paid? | Unpaid amount | Loss | Default rate |

|---|---|---|---|

| Within maturity (0-30 days) | 20 000 | 500 | 2.5% |

| 31-60 days | 12 500 | 500 | 4.0% |

| 61-180 days | 5 700 | 500 | 8.8% |

| 180-360 days | 2 700 | 500 | 18.5% |

| > 360 days | 500 | 500 | 100.0% |

Note: Default rate = loss divided by the unpaid amount.

Here you might note that data shifted a bit.

Unpaid amount for “within maturity” row amounting to CU 12 500 is now in the “31-60 days” row.

That’s OK because we are calculating amounts that fell into certain time bucket – that is, in the beginning of that bucket, not at its end.

So, in “within maturity” bucket, ABC created CU 20 000 of trade receivables; in “31-60 days” bucket, ABC created CU 12 500, etc.

Also, why did we apply the loss of CU 500 to all buckets?

The reason is that all receivables that were written off (CU 500) were in each stage over their life.

For example, all written off receivables amounting to CU 500 were current (within maturity), or within those CU 20 000 and therefore we can say that the loss generated during 20X0 (tested period) is 500/20 000.

The same applies for any other time bucket.

Now, we are not done yet.

We have only calculated the historical loss or default rates.

We still need to incorporate the forward-looking information.

Step 3: Incorporate forward-looking information

This is more difficult, but let me just outline one very simple approach.

Let’s say that ABC’s credit losses show almost linear relationship with unemployment rates.

Please note that “unemployment rate” is NOT a prescription for you – you should find your own macroeconomic factors that could affect your credit losses.

And, let’s say that the statistical office in ABC’s country assumes that unemployment rate will go up from 5% to 6% in 20X2.

ABC’s experience is that when unemployment rate increases by 1%, it triggers the increase in default losses by 10% (note – you should be able to prove that).

Therefore, ABC may reasonably assume that the loss of CU 500 can increase by 10% because of the increase in the unemployment rate – that is, to CU 550.

Thus, the calculation of loss (default) rates adjusted by forward-looking information is as follows:

| When paid? | Unpaid amount | Loss | Default rate |

|---|---|---|---|

| Within maturity (0-30 days) | 20 000 | 550 | 2.75% |

| 31-60 days | 12 500 | 550 | 4.40% |

| 61-180 days | 5 700 | 550 | 9.60% |

| 180-360 days | 2 700 | 550 | 20.40% |

Step 4: Apply the loss rates to the current trade receivables portfolio

And finally, coming to the end of this exercise, let’s apply these loss rates to actual portfolio of trade receivables as of 31 December 20X1:

| Days after issuing invoice | Amounts outstanding | Loss rate | Expected credit loss |

|---|---|---|---|

| Within maturity (0-30 days) | 800 | 2.75% | 22.0 |

| 31-60 days | 350 | 4.40% | 15.4 |

| 61-180 days | 280 | 9.60% | 26.9 |

| 180-360 days | 170 | 20.40% | 34.7 |

| > 360 days | 100 | 100.00% | 100 |

| Total | 1 700 | n/a | 199.0 |

Done.

ABC can recognize the impairment loss on trade receivables as

- Debit P/L Impairment loss on trade receivables: CU 199

- Credit Trade receivables – adjustment account: CU 199

Note: this journal entry assumes that the previous balance of the loss allowance was 0. If there was a balance, then ABC recognized just a difference to bring the loss allowance to CU 199.

Return to top

8. Further reading + ECL course

If you wish to dig deeper in the topic, here are a few articles that I recommend reading:

- How new impairment rules in IFRS 9 can affect you

- Measurement of ECL: probability of default vs loss rate approach – learn about two most common methods applied when measuring ECL, their pros and cons and illustrative examples

- How to measure probability of default – this article describes a few methods of measuring probability of default (PD) and contains my personal recommendation for external help if you need (discounts for CPDbox subscribers and readers)

- Expected credit loss on intercompany loans – learn to apply the newest ECL model

- Example: ECL model on interest-free on-demand loan

- How to calculate the impairment loss on intercompany loans?

Also, I would like to point you to our course “ECL for Accountants”, where you will learn how to apply ECL on trade receivables in much greater detail.

Any questions? Please let me know in the comments below this article. Thank you!

Return to top

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

258 Comments

Leave a Reply

Hi Silvia

I do have one question in step 2 . Why is the unpaid amount within maturity (0-30days ) $20,000 as oppose to $12,500 to reflect what was done in step 1 . I saw your explanation “indicating that it is the beginning of that bucket and not the end” but I am still not sure .

Thanks in advance

Thank you madam. For your knowledge sharing. You are like Goddess Saraswathi matha for IFRS). Really I.will be grateful to you madam.

Hi Silvia, thank you would you please share me an example of general approach method. Because I am working in Microfiance

Hi Silvia

Thanks for your explanation on the bad debt provision calculation. With regards to Step 4: Expected credit loss calculation the expected credit loss calculation is 199 while the write off is 500. This means that our expected credit loss is 301 less than the previous year write-off. I thought that the expected credit loss would be closer to the actual write-off?

Please advise

Hi Silva thank you for sharing this article. would you please explane to me amortization model with effective interest rate?

Hi Silvia,

Just wondering how do you compute the % expected credit loss

I believe the above article is all about the expected credit loss and getting its percentage.

Dear Silvia, Thank you for the simple approach for calculating the Bad Debts provision. however we deal with government entities within in the region.

example 50 % of our clients are government sector do we really need to take bad debts provision for those customer while calculating bad debts provision for our business case. please let me know what IFSR 9 state about if over dues calculation pertaining to Government category customers. appreciate your response.

Hello .. very good simplified approach. the question is whether analysis should be done based on due date or invoice date. Larger portion always must be in not-due column if you calculate the ageing by due dates. Generally pattern to each industry could be different. By the invoice ageing method you may land up creating provisions for non-defaulting customers and cash sales customers (if analysis is done inclusive of cash sales). What’s your view to calculate the default rates on due dates rather invoice dates and if due dates default is calculated then what are changes to aforesaid method.

Hi Silvia. Thank you for sharing the article. When calulating the default rates and subsequently general provision for bad debts on current receivables, should we first exlude the items/invoices (from the base for default rates and from current receivables) that are already covered by specific provision?

Hi Beata, yes from the calculating the provision itself (that would be double counting), but not for arriving at historical default rates – at least not in all cases. You have to look at your specific situations. Are these defaulted debtors some specific clients with different characteristics than other ones?…

Hi Silvia,

In the given example, 500 is considered as bad debt and is used for calculating Default rate. What if I already have 10000 accounted in the Bad Debts account (P&L) which is already written off during the year (this 10,000 is not a reserve for bad debts). Should I consider my 10000 for calculating the default rate or 500?

Thanks in Advance, Awaiting your reply.

Thank you for the simplest writing for us to understand better but What if the receivable is for intercompany accounts that will be eliminated when consolidating? The parent will do provision as well to follow the IFRS9? And if they write it off in the future it will be somewhat like condone and the subsidiaries will record it as income?

Hope I could have some clearance on this as im quite confused.

Jeng, of course, on consolidation everything is eliminated, including the provision. Provisions relate to separate accounts only (when it comes to intragroup items between subsidiary and parent). Careful about associates and joint ventures – here you do not eliminate. S.

excellent article

Hi Silvia

The above example of simplified approach is very useful easy to understand and apply. Can you please also share an example to compute ECL using General approach (stage 1, 2 and 3) for loan portfolios specially focusing on commercial banks? Also what is mean by other assets/ exposure in the context of general approach ?

Thanks

Hi Affan,

thank you! I showed one example of general approach inside the IFRS Kit and maybe I will cover it in the article here. S.

This is a very helpful article on new requirements for IFRS 9. Kindly explain what should be done in situation where during the calculation of historical loss rate the unpaid amount in 180-360 days is CU450 instead of CU2700. Would the default rate be calculated as 111%?

No, because this lacks the logic. If unpaid amount is only 450, then how the loss could be 500? In this case, the maximum loss would be 450.

Thank you all for the enlightenment on simplified approached to calculate impairment of receivables.Can i please get advice on treatment of provision of impairment of trade receivable and how to account for it in our account?Thanks

Noted, it should be in fact easier to do it per invoice but unfortunately the accounting software we have makes it challenging to do so, therefor i believe & since its acceptable, that we are going to do it per client and hopefully be able to justify it to our auditors.

Also, do you recommend any tool or further reading to ease our transition ?

Regards,

Amani

Dear Siliva,

Firstly, thank you for this very informing article and for taking the time to respond to queries,

Secondly, we are going to apply IFRS 9 in my company, working in retail business of automotive spare parts and i was just wondering, should we calculate the historical default rates by analyzing each invoice made on each client account and its collection period, or can we do it using the balance of each client account through the period and the collection made through the period (as a total for each client, not per invoice).

Please advise, Thank you.

Amani

Interesting question. I would do it based on individual invoices rather than based on clients. I know that the credit risk is about the same, but it would be maybe easier to categorize each invoice based on overdue days rather than categorize the client. However, your method may prove to be relevant if you can justify it. S.

Dear Silvia,

I get a great benefit from your article, My inquiry are below:

1. Can you quote some scenario/example for Trade receivables WITH/WITHOUT significant financing component?

2. Pertaining to your article, ABC can recognize the impairment loss on trade receivables as

Debit P/L Impairment loss on trade receivables: CU 199

Credit Trade receivables – adjustment account: CU 199

The latter account whether is similar to Provision?

Thank you

Hi Loong,

1. Well, I can, but not in these comments, just very shortly – if you agree to sell on invoice and your invoice is repayable within 3 months, then it’s without significant financing component. If you sell for the same price, but the invoice is repayable in 2 years – then it’s with the significant financing component.

2. Well, no, because provision under IAS 37 is a separate liability on the liability side, but the adjustment to receivables decreases your assets (i.e. it is not presented separately as liability). S.

Thanks a lot. You replied my question as well!

Well done Sylvia. I am always looking forward to your article and it never disappoints each time.

You’re helping lives with these articles. Just thought you should know.

Immanuel., Lagos.

Many thanks , dear Silvia.

A have a question: If in our analysis for previous receivables there were no unpaid/written off debt, what can we do for determining the percentages. Can it be zero for all of aging analysis??

Superb article ! Really like it. I have a question, when there are multiple macroeconomic factors so what should be the approach

Aamir, in this case, you would need to apply some simulation techniques like described above. S.

HI Silvia,

Wonderful practical insights, which my auditors hold the same view! Just wanted to ask further, for the forward looking rate, can it be a different rate for each reporting period, e.g one period Inflation rate and the other Interest rates? Reason is to minimise unnecessary large fluctuations in ECL’s to be provide for each reporting period – meaning to say taking the lowest possible rate every quarter that impacts the business and receivables. Thnxs!

Dear Mark,

No, because as I wrote above, you should identify the factor affecting the behaviour of your receivables and I doubt it would change period to period. I mean – it can sometimes change, but the reason for the change should be justified with the change of various factors in environment really affecting your receivables, and NOT by the “avoiding large fluctuations in ECL”. S.

Good Morning Dear Silvia, I am trying to apply your above mentioned Example: Impairment of trade receivables under IFRS 9. where i am not in a position to arrive the unpaid amount, if i take a cut of date 31 Dec 2017. For ex: total Revenue 4million for the period Jan to Dec 2017 and the corresponding receipts 3million and the balance 1 million is not yet due for collection, the same is due in subsequent period and received. now do i need to take all the receipts including for the period years to arrive unpaid amount? Please advise, and thank in advance for your Help.

Hi Neelakantam,

yes, of course. You should not trace total receipts of cash in 2017 – you should trace the receipts of the receivables generated in 2017. It means that sure, you have to take subsequent repayment of 1 mil. into account. S.

Dear Silvia,

For trade receivables with credit terms of almost 90 days. wouldn’t the historical trends and current situation enough to calculated ECL? Forward looking can be done if information is available without undue cost or effort. But for servicing business or trading business an effort and cost will be for incorporating forward looking factors, especially if modeling those factors would be more suitable.

Please give us your thoughts in this regard

Silvia madam made me to remember her name whenever I hear about IFRS. It’s like she made me to think IFRS is International Financial Reporting by Silvia(IFRS). Hahaha..

Thank you so much madam.

LOL 🙂

Thanks to you Maam Sylvia and thanks to your website. It’s so user friendly.. More power to you.. 🙂

Hi Silvia,

i’m working at telecom company and we have huge trade receivables account with other operators, also banking interest rate is 10 % for one year. and based on historical data they paid their debt after 21 months from issued invoices, so that my question is about net present value (NPV), do i calculate NPV for current receivable balance as credit loss and illustrate in balance sheet or not? if yes with which rate? what is the IFRS 9 opinion abot net present value and net future value?

Very neatly explained and simple to understand. Awesome work.

Very amazing, simplified, and wonderful , but here you considered the amount of CU 500 >360 Days is written-off, suppose if i have A/R balance over 360 days and i don’t have bad debts ( written-off), shall i consider that balance over 360 days as the written-off and shall i divide it to the total credit sales over the year to get the credit loss ?

Hi Salah, well, please see my response to Serghei above – with some minor modification, I would write you the same. S.

Hello Silvia, thank you for such a wonderful article. You said on ‘how to group the financial assets’ that not all trade receivables share the same characteristics and therefore should not be placed into the same bucket. And on grouping them it depends on the factors affecting the repayment of those receivables for example ‘Geographical region’ in such a case does it mean the rates/percentages for customers from cities and customers from countryside within the same business will be different or a single average rate/percentage should be used?

Hi Emmanuel,

if your groups or segments of receivables have different characteristics affecting the collection of cash, then you should perform the same analysis for each group separately and it means that yes, they will have different loss default percentages. S.

Dear Silvia,

First of all, I would like to thank you for your interesting and practical article.

I have just one question for you: Can we still compute the default rates if there are no written off receivables during the analyzed period? Thank you!

Hi Serghei,

excellent question. Let me tell you this: the credit loss is simply the present value of difference between the amount of the receivable per contract and the amount expected to receive. The amount expected to receive is what matters here. In the above example, it was clear that we expect to receive everything less write-off. The same applies to any other situation – you don’t have to take write-offs into account, instead you should take the difference between the contractual amount and expected receipt. Of course, if you expect to receive everything (and there’s no significant financing component), then you have no credit loss. Anyway, for large portfolios, I would perform analysis in more years separately to see how the loss rates develop. S.

Hi Silvia, in accordance with IFRS9. p5.5.17 we have to take into account the time value of money. If entity expects to collect the full amount of invoiced revenue but in a later period than per contract date, should it to recognise impairment loss on trade receivable balance in amount of difference between the cash flow per contract and present value of expected cash flow? Expected cash flow = Cash flow per contract. Thanks&

Yes, sure – but 1) you can ignore time value of money if the difference is < 1 year, 2) this is about the application of the simplified model, more specifically provisioning matrix as per IFRS 9 implementation guidance. S.

I have been reading multiple articles on the topic and yours was really the most clear and understandable explanation that I have come across. I always felt that the simplified approach was not simple. Thank you for simplifying it. 🙂

Many Thanks!

Hello Silvia,

I am Fredrick from Ghana, that was a very useful article. But if i can ask, what happens to forward-Looking when from experience the macroeconomic factors those not have a liner relationship with the historic loss rate?.

As I wrote above, you have to do some modelling and simulations, it’s not very easy to describe it in the article. Best, S.

I have checked this article and illustrated example, However it doesnt talk on the use of collaterals to arrive at Impairement charges, I thot i heared somewea IFRS 9 provide such oppurtunity, ”To include collaterals on computation of Loan Loss Provision”

I am curious about this. For example A Strata has legal right to sell an apartment if the proprietor does not pay his/her maintenance fee. Should the strata still provide for bad debts?

Thank you for the absolutely amazing article, Silvia

A short question: can the simplified approach be applied to calculate the ECL for NPLs?

Hi Ivaila,

thank you! For non-performing loans, you still need to apply general approach, but as the loan is non-performing, it would be in stage 3 in most cases and you would calculate impairment loss equal to life-time ECL – which is very similar to simplified approach. S.

Thank you Silvia. Appreciated!

Amazing work. Very informative. Keep the good work going.

Great article as always Silvia ! This is so informative, gonna share that with my colleagues asap ! 🙂

Hi Silvia,

Marvellous job . I could only say that your work is great.

Thanks for sharing.

Hi! silvia TANZANIA We are not back,Thank you very much keep it up you made my day

Hi thank you ….it is really a helpful article to get a practical touch of ifrs 9, just one quick question – I noticed that one company was calculation ecl impairment on their net debtors (ie after deduction of current provision ) , so is it a right way to calculate or we should calculate it on gross debtors ???

Hi Varun, well, I would say that you should calculate it on gross debtors because it is more difficult to set the default rates for a part of a receivable. Then, you can just make a difference between the existing ECL provision and the new one. S.

Silvia consistently amazes me. Your simplicity is incredible. Thanks for this. Keep up the good work. Cheers.

Dear Silvia,

This is really a very good Article explaining and giving further guidance on the application IFRS 9 on setting Bad Debt with illustrative examples. It will assist Finance and Accounting teams. I appreciate your relentless efforts,

Thanks, Shimellis 🙂

Hi Silvia,

After our point of Write off we still get significant post write off recoveries. How do you identify the best point of write off according to IFRS9 such that post write off recoveries are not material?

How about using your past historical information? IFRS 9 does not define any “point of write-off”. However, if your historical recoveries say that you recover certain amount even after 365 days (just as an example), then making 100% provision is not reasonable.

Hi Silvia,

As usual, you are at your best. we need more practical oriented articles like this.

Live long.

Aaaa, thank you 🙂 Maybe if you can give me a hint what other practical topics you would like me to cover, that would be fantastic! S.

This a powerful yet simple illustration! Even the ‘idiot on the street’ would have understood easily, I guess. Thank you!

Hi Charles,

OMG, I don’t think my readers are idiots on the street 🙂 Thank you! 🙂

Hi Sylvia ,

I am from Canada. I am from the Real Estate industry dealing mainly in Residential leases. I found your article so insightful and easy to follow in the application of the calculation of the impairment provision for trade receivables. To my surprise the auditors in the current year audit that was just completed a few days back did not question our method of bad debts provision that we have been using since.

Certainly a lot of learning for me here that I will pass on to my staff.

Thank you very much for sharing.

Hi Ravi,

great, I am very happy that this article has a practical sense for you. In relation to auditors – well, sometimes they just accept whatever clients give them, as soon as it looks elaborate enough… I don’t want to be too critical, because I was the auditor, too! Take care! S.

Hello Silvia,

I have gone through your articles, it is really enlightening. Now, my client operates in a condition where it is difficult to group them in debt age structure. So as far as I can get from them is the total receivables during the year. How can I apply this ECL to them? Thank you

Well, I don’t get it – you cannot say when each receivable is/was due? I have never heard of this situation and I am sure this info exists – so you need to make analysis.

Yes the model of operation is such that they don’t have a grace period.it means that all service becomes payable immediately.it is then difficult to group as highlighted in your example. So how best can this be done. Can it be applied on total receivable as a sum.

But the above calculation actually takes days AFTER the due date. If the due date is immediate when the service is provided, then you can still calculate the number of days that passed between the provision of service and the reporting date.

Thank you once again. I wish I can talk to you better on mail

Thanks as always for the supper document. Regarding LGD and PD do you have any documents or workings like the above. How to determine PD and LGD is very important to get in to the loan provision. kindly do share if you have one.

Hi Gadissa,

thank you! Well, there are some materials available on the net if you look for some Big 4 guidance. Anyway, I can write an article in the future about more practicalities. Take care!

Sincerely speaking, you are amazing..

Well done Silvia for putting theory into practice.

Dear Silvia,

Thank you so much for making IFRS so easy for us.

I have a question regarding individual receivables. What I mean is, if we take a debtor’s card and want to check the receivable by the end of a period, how can we extract to portion of the total impairment (and hence accrued provision).

Also its interesting, how do we treat the provision when the receivables get paid after some time (fully, of partially).

Thank you in advance!

Hi Natalia,

you can always exclude individual debtors from the group assessment – as a part of your segmentation strategy. Then you can assess the debtors individually and apply the above principles to the remaining receivables assessed in the group. If the receivable is paid, then there’s no impairment anymore, is there? 🙂

What I mean is after the impairment has occurred as a result of applying the provision matrix, and in the future periods some of the receivables (impaired) are collected. Probably we recognize profit, is it correct?

Yes, of course, that would be reversal of impairment loss. Anyway, you would do these calculation at each reporting date and you are just booking the change in provision (either increase or decrease) in comparison with the previously recognized amount. S.

Thank you Silvia. Your web site is the best finding for me in IFRS issues so far!!

Hi Silvia – on a similar note, say in January I use the matrix and calculate $20,000 in provision (Debit: Provision $20k, Credit: Bad debt expense $20k). What is the entry if in the next month using the matrix I calculate only $18,000 in provision? Would I credit the Provision (Balance sheet) $2k and debit bad debt expense $2k?

Sorry I just realized I had the debits and credits backward in my example. The first month would be a debit to impairment loss ($20k) and credit to trade receivables – adj acct. Then the following month (assuming a calculation of $18k) would it be a credit to impairment loss P/L ($2k), debit trade rec. – adj acct ($2k).

Really happy for all your efforts in this IFRS issues.

Please continue sharing your great knowledge in this regard.

Thank you, mussie 🙂

How you doing Silvia,

Thanks for your efforts which support us to understand IFRS.

I think we need an example for adoption ifrs9 for trade receivables since more changes happend between 2018 and 2021.

For emaple:-

– Do we need to use the flow rate?

Do we need to use the provision matrix?

….. and so many methods we read it or hear about.

Dear Silvia,

As a financing company, our loans receivable are of the same product type, i.e.,consumer loans. The terms of the loan are not more than 2 years, aging structures are the same as your examples, collections are analyzed by the loan system by time buckets, historical loss rates can be calculated, and forward-looking information is not hard to identify. With these data, can we apply the simplified approach in calculating the loan loss provision instead of the general approach?

Dear Dante,

I dont think you can use the simplified approach in this regards as these are interest bearing financial assets….. kindly refer to the General approach……my opinion

Dear Oladele,

Thank you very much for your opinion.

can i still use general provision even we dont have any history of bad debts in past?

Hi Dante,

I agree with Oladele in this point. Consumer loans are loans – they were created as a result of providing financing to the clients, not as a result of selling goods/rendering services on credit. Therefore as such, they can’t be considered trade receivables. Anyway, you can still apply portfolio approach to these loans – just the percentages will be different. S.

Hi Silvia,

Thank you very much for your reply.

Hi Silvia,

Nice explanation. I have a question based on what Dante asked. What if we only recognize interest receivable against performing loans . Still we cant use simplified approach?

Regards,

Faris

It is very useful overview of IFRS 9

Excellent article on PBD.Thanq Silvia.

For retail rental car company how to calaculate ECL for standing contract. Thank you