How to account for free assets received under IFRS

The best things in life are free…

… at least that’s what Janet Jackson sang in one of her top hits.

However, when your company receives some free assets, then the question is:

Are they really received at no cost and no strings attached?

Is there something else behind?

Many years ago I attended the counting of fixed assets in one big manufacturing company.

It was a freezing December morning, huge piles of snow made it quite difficult to get around and we were sneaking in and counting various types of machines in the client’s storage.

One of my colleagues spotted some cooling units, new – still unpacked, and he could not find them in the document with the register of fixed assets, so he asked:

“ Why are these cooling units not recorded in the register?”

The boss of the warehouse, a bored grey-haired guy, murmured with the tobacco pipe between his teeth something like:

“Oh gosh. We did not buy them. We got them free when we purchased the machines.”

Sorry, I don’t remember now what machines they purchased, but I remember the discussion with the accounting manager that followed.

So what should you do in a similar situation, when you receive some free assets?

In this article I try to tackle this quite frequent issue and give you some hints.

Please note that this article is not about giving assets for free – for this purpose, please see here and here.

Before you start: Is it material?

You need to apply your judgment to assess whether your free asset received is material enough to bother.

For example – when you receive pens, lighters or other promotional materials, they might not make any difference in your books, so just don’t worry about their accounting.

The same applies in a multibillion dollar company that pays monthly telecom plans for their 100 executives and receives 100 mobile phones at no cost from the network provider.

Is their aggregate amount material?

If not, just don’t bother.

If yes, continue reading.

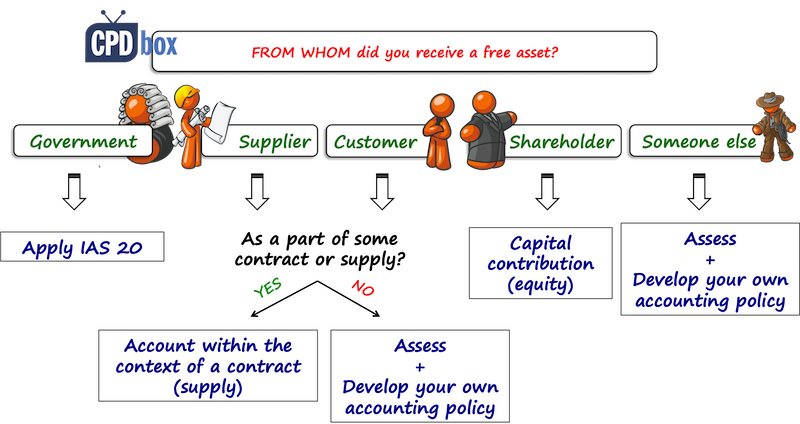

The starting point: Why did you receive your free asset?

Let’s say you received a significant asset.

For example, some piece of equipment, free land or something like that.

The first thing you need to examine is why and who the donor was.

What is the substance of this transaction?

Even more important: Whom did you receive the free asset from?

The accounting treatment will then depend on your answer.

Let me analyze a bit here.

#1: Free asset from government

What counts as “a government”?

Besides government, also government agencies and similar local, national or international bodies count as “government” for the purpose of IAS 20.

So, even if you received your grant from IMF, EU, WHO or similar organizations, you need to follow IAS 20.

#2: Free asset from your supplier

The question is: Did you receive a free asset as a part of some contract, together with the purchase of something else?

If yes, then you might need to allocate a part of total purchase price to the “free asset”.

Example: Free asset from a supplier

Let’s say you enter into a contract with a supplier to acquire 3 big pieces of machinery and the contract says that the total price is CU 3 000 for those 3 pieces (CU 1 000 each).

And, the contract says that the supplier will deliver also a cooling unit (=separate asset) at no additional cost.

A big mistake that many companies make is that they do not recognize a free asset at all.

However, the Conceptual Framework for Financial Reporting asks you to report any asset that you control.

Thus, it is a misstatement if you ignore your free asset, you use it – but you do not show it in your financial statements.

So what to do in this case?

Well, you should measure the free asset – a cooling unit in this case – at its cost.

The total cost for 3 machines and 1 cooling unit is CU 3 000, so you should allocate this total purchase price to all assets based on their fair values, or current selling prices if they are new.

Let’s say that the similar cooling unit trades for CU 300.

Then the total of selling prices is CU 3 300 (3 000 for machines and 300 for cooling unit).

Thus you allocate CU 909 to each machine (= CU 1 000/3 300 * 3 000) and CU 273 to the cooling unit (= CU 300/3 300*3 000). Total allocated cost is 909*3+273 = CU 3 000.

Now, many might think that it is not OK since the cost of one machine is CU 1 000.

Well, the standard IAS 16 says that the cost is the purchase price less discount and “free” cooling unit is a sort of a discount, don’t you think?

Another case of free assets received from suppliers is when you receive an asset as a gift for your long-term loyalty or a support of a promotional campaign.

For example, a supplier might sponsor the renovation of your shop and display area.

In this case, it would be very hard and impracticable to allocate a part of purchase price of other products to this free asset.

Therefore, you need to adopt different solution. Just go on reading.

#3: Free asset from your customer

If yes, then you might need to apply IFRS 15 Revenue from Contracts with Customers and assess the situation carefully (IFRIC 18 applied in the past).

In this case, when you receive a free asset from your customer within some contract, is it considered as non-cash consideration.

The article IFRS 15.66 requires including the fair value of non-cash consideration in the transaction price.

Example: Free asset from customer

Let’s say that you enter into a contract with a manufacturing company to process some wood for their one-off project.

You agree that you will use the client’s wood processing machine.

The contract specifies that the price for the wood processing is CU 1 000 and you can keep the machine (since the client will not need it anymore and it is not new).

Let’s say that the fair value of a machine is CU 300.

Thus your transaction price is CU 1 300 and you will recognize the machine at its fair value of CU 300 (it then becomes machine’s cost) at the moment when you gain the full control of a machine.

When that happens?

It depends on the specifics of the contract – sometimes it may happen right in the start of executing the contract (e.g. you take the machine to your premises and work there), sometimes it may happen in a different time (e.g. when you can use the machine only at your client’s premises and take it only after the contract is executed).

If you receive a free asset from a customer outside any contract, then again, you need to find a different solution. Read on!

#4: Free asset received from your shareholder

We can regularly see big transfers of various types of assets, including machinery, lands and sometimes buildings from a parent to its subsidiary.

In this case, if you gain control of an asset, you should recognize it at fair value – which becomes its cost.

As this is a contribution from shareholder, you should NOT recognize it as an income in your profit or loss.

Conceptual Framework strictly excludes contributions from shareholders from the definition of income.

Instead, the shareholder increases its investment in a subsidiary and a subsidiary shows the receipt of a free asset directly in equity as a capital contribution from a shareholder.

#5: Free asset received from other parties

You can receive a free asset from anybody as a gift, with no strings attached.

One example comes to my mind from the past: a hospital receiving USG and other machines from a cancelled hospital at no cost.

In this case, you need to develop your own accounting policy, because IFRS do not contain any guidance on how to do it.

And, I would say that this applies also to free assets received from your suppliers or customers where it is impossible or impracticable to match these free assets with any contracts.

We need to develop the accounting policy based on the similar rules in other standards and the Framework.

What are the closest similar rules?

Yes, you guessed it – the standard IAS 20 that applies for government grants.

Let me give you a few considerations here:

- First of all – you need to show assets that you control. I have already wrote that above.

- Secondly – as you have no cost, the fair value concept applies here.

- You should not show the receipt of your free asset directly in the equity because it does not come from your shareholder.

Analogically, IAS 20 strictly prohibits accounting for grants straight in equity, so we should be consistent with this rules when forming the accounting policy in this case.

Now, this is the hardest part – how should you recognize the free asset that you received?

In other words – what is the credit entry?

Here, I would show the credit entry as income in profit or loss.

Not the revenue, because the revenue comes from ordinary course of business.

The journal entry looks something like that:

- Debit PPE – asset: fair value

- Credit Profit or loss – other income: fair value

Why not deferred income with subsequent amortization of a deferred income in profit or loss?

OK, I know that it is the treatment required by IAS 20 for government grants, however:

In this case, there are no strings attached in a sense that you do not have to hold the free asset and use it.

You do not have any conditions attached to the receipt of a free asset, right?

Therefore I believe that the receipt of your free asset indeed represents an increase in your net assets at the moment when you receive the asset and your financial statements should reflect that increase.

If you recognize your free asset in deferred income (liability in the balance sheet), then you are not showing the increase in your net assets.

Also, someone might argue that you are not in line with matching concept because you are not matching the income (receipt of a free asset) with the expenses (its depreciation).

Well, let me explain that IFRS do NOT contain anything like general matching concept – not at all.

But, IFRS tell you to recognize expenses when the relevant service or asset was consumed (thus together with the depreciation).

Also, IFRS tell you that the income “is recognized in the income statement when an increase in future economic benefits related to an increase in an asset or a decrease of a liability has arisen that can be measured reliably” (see Conceptual Framework).

Thus it is perfectly OK and in line with the Conceptual Framework to recognize an income from the receipt of a free asset when it is received and not over its useful life with amortization.

Why is it different from the treatment of government grants under IAS 20?

Well, exactly as I wrote above – government gives you grants (free assets or cash) for some purpose.

In most cases, you need to meet certain conditions to get the grant and afterwards.

Therefore receipt of a free asset from anyone else is different, especially if there are no strings attached.

BUT!!!

If you receive free asset from an entity other than government and there ARE conditions attached to it, then of course, IAS 20 treatment (via deferred income) is more suitable policy choice in this case.

Any questions or comments?

Please let me know below – thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

113 Comments

Leave a Reply

at the initial recognition the cost and the fair value most probably are equal. So recognize it at fair value.

If the assets are given for free, then there is zero cost.

Will fair value concept be applicable where the company gets Inventory of naturally growing agriculture products for which it did not incur any cost of cultivation from its own lands?

Yes. Please see IAS 41.

Hi,

I have the following queries:-

1. Company A is a subsidiary of a group, Company A had invested in securities of a Company X and then the fair value of Company was nil. Company A was terminated.

2. The parent Company of Company A had filed a case against Company X, regarding the fair valuation and had incurred some legal expenses.

3. After 2 years the Parent company won the case and received additional shares in Company X.

My Question is that, since Company A has been terminated the investment will go to the Parent Company, if this is the case what amount will be recognised in the books of the parent company? and what will be the double entries.?

Please help..

When the machinery is a gift from a shareholder, we assess the fair value, debit the fair value and credit the equity. Please let me know how the depreciation will be accounted for in this case?

We are a company that has a series of points of sale. The activity is pharmacies. We receive free goods from suppliers. Do you record this goods at cost or not, knowing that the invoice is zero, knowing that we use periodic inventory

We purchase some Air condition, 1st year we totally expenses it out but now 3rd year they are still in good condition we want to make it asset. any body help me how we can valuate it as asset. and how we will record it in books .? what accounting entry we will pass?

Hi Silvia, can u advice how to treat cash receive from third party for the replacement of existing asset. Example: Tower relocation requested by third party. We need to relocate our tower, third party will pay cost to build new tower and they will get the route.

Can you advise on how to account for complimentary cellphones received from a supplier as part of a contract. I was thinking the entries would be DR: Asset A/c (with the fair value of the phones) but I seem to be stuck as to what the CR entry should be. This is for a non profit organisation, so I am thinking to CR the Accumulated Fund account.

Thanks for sharing.

My company, telecom company in Somalia, received Internet bandwidth IRU worth in the market USD4.5 Million for free basis. The duration of the IRU is 15 years. My company shall only pay USD15K yearly for the maintenance of the IRU. The 20GB IRU could be sold in the market for more than USD20Million through the years of IRU life being 15 years. Therefore, I would be grateful if you assist how to treat this almost free internet bandwidth IRU in my company financial books.

Hi Silvia, assuming an entity converts from being limited by guarantee and gives free shares to its existing shareholders, how would these shareholders account for the free shares in their books

Hello,

Silvia, thanks for your article,.

Can you supple reference from IFRS on the 4th case? #4: Free asset received from your shareholder.

Can entity recognize contributed ppe on with nominal value at he initial recognition? Or is it must to make valuation?

Hi Silvia. We are a utility company with complex underground water distribution systems. When a developer needs to move some of our structures in order to develop their land, create roadways etc., they pay for the relocation/rebuild of our wells and structures, thereby increasing the value of our systems. There are no strings attached, and we do not owe them anything in return. Is this considered a capital contribution? How would that be recorded?

What in case? Customer is providing materials to supplier at free cost which are being used in manufacturing and being re-supplied to Customer as a finished good? Should I account for it in COGS and what will be the basis as per IFRS; as I have NO visibility on the price.

Hi Silvia,

Regarding a donation from another party, would it be wrong if I recognized my asset in PPE and then recognised income over time equivalent to the depreciation of the asset.

Hello silvia,

Got a bit tingled up in this if you could help would greatly appreciate it. So in a situation when free asset is received from your shareholder, the shareholder increases its investment in a associate, however how does the investment increase in

1) Separate financial statement when cost method is used (Increase by the cost of PPE in parents book or FV of PPE and parent recognises Gain/Loss)

2) In consolidates statement when Equity method is used, is the cost portion any different from when using cost less impairment method.

Many thanks in advance,

P.S i couldn’t find any direct references in IFRS’s if you could reference me the standard as well it would be a huge help.

Hi Ray, couldn’t find IFRS reference as well.

can you share with me if you found anything?

Hi Silvia, Great article! What if the company receives the asset from the government, but there are no strings attached? Would you still apply IAS 20? i.e. the credit goes to deferred income, rather than P&L.

Hi Fraser, yes, IAS 20 applies. If its is a long-term asset (i.e. PPE), then credit = deferred income and you “amortize” it in P/L together with depreciation.

Hi,

What would be the entries if the approach of ‘deducting the grant in arriving at the carrying amount of the asset’ is taken?

Thank you Silvia!

What would be the accounting method if we use capital approach .

Do we need to depreciate the fee assets that we received from government after using the method of capital approach? Ie. credit capital receive and after do the normal depreciation is it right ?

Hi Silvia, Further to Fraser’s comment, what if the government is also your shareholder? Do you still credit deferred income or should you credit contributed equity? Thank you!

Hi Barbara, it depends on the specific circumstances in what capacity the government is acting. If there are some documents substantiating the grant (i.e. conditions or “strings attached”), then in most cases this is the government grant. So always examine the substance.

hi Silvia, thanks for your article. If the Company received PPE (like $1,000,000 or sth) as compensation from insurance due to loss from disaster, how should the Company record these PPE into accounts ?

The same way as you would have accounted for the compensation from the insurance company if received in cash. The only difference is that here, you recognize PPE at its fair value.

Hi Silvia! Thank you for the article. If there is a fixed asset as share capital contribution (initially recognized at market value) and its tax value is much less than the market value. Should deferred tax liability be recognized?

Very helpful article. Thank you Silvia

Water Filter Purchase on the account.

How can I account it Please Help me.