A financial guarantee is a specific type of a financial liability defined in IFRS 9.

It arises when an entity backs up a loan or debt taken by another entity and it often happens among the companies within one group.

And, as it is intra-group, there is often no premium paid by the debtor to the party issuing the guarantee.

I received a following question related to this topic:

“Hi Silvia, we have a subsidiary in a foreign country and the subsidiary needed to take a loan.

The bank provided a loan, but we, the parent company, had to guarantee that we would pay the debt in case if our subsidiary fails to pay.

Our auditors say that we have a financial guarantee under IFRS 9 and we should account for it. But how?

Also, we issued a general guarantee to support our subsidiary in case of the negative equity – should we also account for this guarantee?”

IFRS Answer: What is a financial guarantee?

IFRS 9 Financial Instruments defines the financial guarantee as a contract that requires the issuer to make specified payments to reimburse the holder for a loss it incurs because a specified debtor fails to make payments when due in accordance with the terms of a debt instrument.

Therefore yes, you have an issued financial guarantee contract here because you as a parent agreed to reimburse lending bank just in case your subsidiary cannot pay.

And yes, your auditors are right – you have to account for this guarantee somehow.

Before I explain how, let’s take a look at the general guarantee to support your subsidiary in case of negative equity.

This is NOT a financial guarantee under IFRS 9, because it is NOT specific, you have no specific payments to make and this type of guarantee can cover pretty much anything on top of the debts.

Financial guarantees: Initial recognition and measurement

Initially, you need to recognize an issued financial guarantee at fair value.

That’s the basic measurement rule in IFRS 9.

What’s the fair value of such a guarantee?

It depends so let me give you a few hints.

Normally, when you issue a financial guarantee to the third party, not intragroup, then you would charge some premium for the guarantee, some fee for issuing that guarantee – and in this case, that would be the fair value of it.

Often, the guarantee is issued intragroup at no fee, like in today’s question.

In this case, we have to apply some alternative methods in line with IFRS 13 Fair value measurement.

For example, you can measure the benefit for the debtor as a result of that guarantee.

What interest rate does the debtor pay with the guarantee?

And, what interest rate would the debtor pay without the guarantee?

If the debtor pays 5% with the guarantee and the market interest rate on unguaranteed loans is 6%, then the fair value of the guarantee is the present value of the difference in interests charged on guaranteed and unguaranteed loans.

What are the journal entries?

Just as a short illustration, let’s say that you received a premium of CU 1 000 for issuing a financial guarantee for 5-year loan. The journal entry is:

- Debit Cash: CU 1 000;

- Credit Liabilities from financial guarantees: CU 1 000.

If you haven’t received any premium, then you:

- Debit Profit or loss: The fair value of your guarantee;

- Credit Liabilities from financial guarantees: The fair value of your guarantee

.

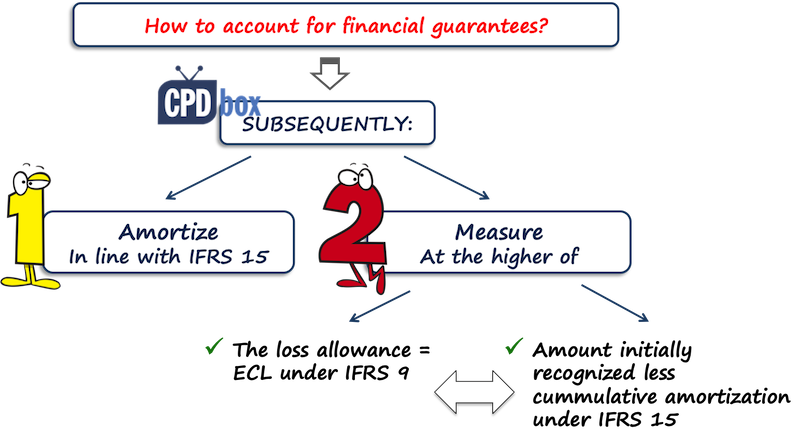

Financial guarantees: Subsequent measurement

First of all, you need to amortize the amount of your financial guarantee in line with IFRS 15 Revenue from Contracts with Customers.

In most cases, you would do it straight-line over the term of the loan.

And then, IFRS 9 prescribes to measure the financial guarantees at the higher of:

- The loss allowance determined as expected credit loss under IFRS 9 and

- The amount initially recognized (fair value) less any cumulative amount of income/ amortization recognized in line with IFRS 15.

Here, you have the challenge to determine the expected credit loss on the amount borrowed by your subsidiary.

So you would need to:

- Determine at which stage the loan of your subsidiary is – stage 1, 2, 3; and then

- Calculate the expected loss allowance as either 12-month expected credit loss or lifetime expected credit loss depending on the stage of the loan.

I wrote a few articles about expected credit loss on my website, there are nice explanations of ECL inside my IFRS Kit, so you might want to check that out.

On the other hand, you need to compare the amount of the expected credit loss with the carrying amount of your financial guarantee – which would be the initial fair value less any amortization:

- If the ECL is lower than the carrying amount, then you are all fine.

- If the ECL is higher than the carrying amount, then you need to revalue the financial guarantee and book the remeasurement in profit or loss.

Illustration: Subsequent measurement of financial guarantees

Let’s get back to our financial guarantee of CU 1 000 on 5-year loan.

You would amortize it straight-line over 5 years (just for simplicity) and the entry would be:

- Debit Liabilities from financial guarantees: CU 200 (1 000/5);

- Credit Profit or loss – Income from financial guarantees: CU 200.

Then you would need to determine the expected credit loss on the loan that you back up.

Let’s say the loan is OK, no significant increase in credit risk, so the expected credit loss is CU 500 (just making this up).

Your carrying amount is CU 800, the ECL is 500, so you keep measuring the financial guarantee at 800 as this amount is higher.

If the ECL on the loan is let’s say CU 1 200, then you would need to book the difference of 400 (which is ECL of 1200 less carrying amount of 800) in profit or loss.

Here’s the video summing up the issue:

Any questions or comments? Please let me know below. Thank you!