Example: Expected Credit Loss on Interest-free On-demand Loan

Let’s face the truth: most intercompany loans (or at least many of them) are special in some way:

- They are undocumented – a parent simply sends cash to a subsidiary with no contract whatsoever and no one has an idea what the terms of the loan are;

- There is no maturity date – a loan can be documented but there is no maturity date stated and no repayments are required;

- There is no interest and/or no repayments required – probably the loan is repayable in one amount at the end (“bullet” loan) at its nominal amount,

just to name a few specific features of intercompany loans.

The first challenge is to determine whether the “loan” is indeed a financial asset under IFRS 9 or some sort of capital contribution out of IFRS 9 scope.

On top of it, if it is a financial asset, you need to recognize an expected credit loss provision if you are a lender.

However, thanks to these special features, it is quite challenging to apply the general approach as described here.

Therefore, let me come up with a very specific but frequent example of expected credit loss provision on intercompany loans.

Example: Undocumented loan

ABC has a newly established subsidiary DEF involved in a real estate development. To finance new projects, ABC sends cash of CU 10 million to DEF.

This transfer of cash is not documented in any contract, but the negotiations between ABC and DEF indicate that ABC will demand the repayment of this cash when DEF becomes profitable (not expected within the next few years).

Initial recognition

Before we even start thinking about expected credit loss on this loan, we must decide how to recognize this loan first.

Clearly, from ABC’s point of view, this is a financial asset and not a capital contribution to subsidiary’s equity, because ABC expects repayment in some future date.

Also, this financial asset is not credit impaired and therefore it can be classified at amortized cost.

Initially, ABC needs to recognize the financial assets classified at amortized cost at their fair value.

Normally, you would discount all the cash flows from the loan with some market interest rate to arrive at fair value at initial recognition.

However, what to do now – there is no clear repayment schedule, no interest…?

Well, in most cases, these undocumented loans with no clearly stated maturity date are deemed repayable on demand.

Of course, this would also depend on the local legislation.

In this case, the effective interest rate of the loan is zero and the loan is initially recognized in its nominal amount of CU 10 million.

Recognizing the loan subsequently

Let’s say that after 1 year, ABC needs to recognize ECL provision at the reporting date.

IFRS 9 says maximum period over which ECL should be measured is the longest contractual period where the lender is exposed to credit risk.

In this case, if the loan is repayable on demand, this maximum period is short – it takes only as many days as needed to transfer cash from the borrower (DEF) to lender (ABC).

Therefore, we need to calculate ECL assuming that the lender demands the repayment at the reporting date – even if the lender has NO intention to do so!

With this in mind, we can take the steps to calculate ECL:

1. Determine the stage of a loan

As you may remember, we need to assess whether the credit risk has significantly increased since initial recognition:

- If not, then the loan is at Stage 1 and we need to recognize 12-month ECL;

- If yes, then the loan is at Stage 2 (or even at Stage 3) and we need to recognize lifetime ECL

However, in this particular case, 12-month expected credit loss will be just the same as lifetime expected credit loss.

Why?

The loan is repayable on demand – which is shorter than 12 months for sure.

As a result, “lifetime” of a loan is that short period required to transfer cash when demanded by the lender.

Easy, isn’t it?

2. Calculate and recognize ECL

IFRS 9 (B.5.5.41) says that you should measure ECL as probability-weighted amount reflecting at least 2 possibilities:

- Credit loss occurs;

- Credit loss does not occur.

In this specific case of on-demand repayable loan, there are just two options:

- The borrower is able to pay immediately (if demanded), or

- The borrower is NOT able to pay immediately.

The thing is that we need to examine whether the borrower (DEF) has sufficient liquid assets to repay the loan immediately.

Now, let me outline what happens in both cases.

Scenario 1: The borrower has sufficient liquid assets.

If the borrower has sufficient highly liquid assets (cash and cash equivalents) to repay the outstanding loan, then ECL is close to zero, because probability of default is close to zero.

Are they sufficient to cover the loan? And – very important – are there any other more senior loans that DEF would need to repay before it can pay to ABC?

Let’s say that the borrower’s bank account shows the balance of CU 11 million – which is great as the loan from ABC is CU 10 million.

However, if the borrower took a bank loan amounting to CU 5 million that has priority, then only CU 6 million is left to repay the loan from ABC – which is not that great.

Also, look at any restrictions on cash and cash equivalent and if there are any, do not count restricted cash as your highly liquid asset.

Scenario 2: The borrower has no sufficient liquid assets

In this case, there will be some ECL, because probability of default is NOT zero.

The reason is that if the lender requires immediate repayment, then the borrower simply cannot repay at that moment due to insufficient funds.

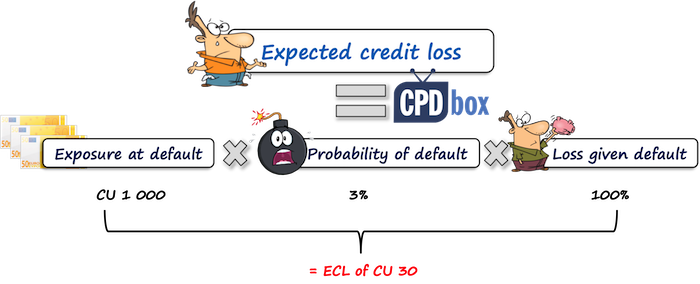

OK, so in this case, we need to calculate ECL using one of the acceptable approaches. In this article I outlined one formula of calculating ECL:

So, even if probability of default is more than zero, you still need to evaluate LGD (loss given default) and EAD (exposure at default).

EAD is clear – it is simply the balance of the loan outstanding at the reporting date.

What about LGD?

Here, you need to assess different scenarios of possible recovery of the loan.

Especially, look to the assets of the borrower and try to estimate their net realizable value – which is about the amount that the lender will be able to get from the borrower if the borrower is forced to sell all assets NOW.

In our example, the borrower is involved in real estate development and therefore it is probable, that it will have some assets with possible net realizable value greater than zero.

Imagine a different situation. Let’s say that the borrower is involved in some research with very uncertain outcome.

In this case it is quite possible that the borrower would have spent a lot of cash on research activities (i.e. expenses in profit or loss) and no assets have been generated – here, LGD would be much greater.

Except for available assets of the borrower, you should assess the following:

- Are there any more senior loans or other liabilities in the borrower’s accounts that would have to be repaid prior lender’s loan?

- Will the lender require immediate repayment? Or, will the lender grant the borrower some time sell the assets over time?

- What would be the expected cash flows from the loan in the case of over-time sale?

… just to name a few things.

Then you would need to set up a cash flow table, discount it, calculate the expected credit loss you get the point.

However, here’s the shortcut: if the borrower’s assets or expected net cash flows from their realization cover the outstanding balance of the loan, then there is probably no ECL (or immaterial ECL).

Finally…

IFRS 9 indeed requires recognizing a provision on all loans, including intercompany loans.

However, as you read here, it does not need to be a big deal, especially if the loan is interest-free and repayable on demand.

You still have to perform some exercise and document it, but it could be simple and easy.

One last remark – all lenders having intercompany loan receivable in their books MUST assess these loans for any impairment, even it there is NO intention to require immediate repayment of the loan.

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

31 Comments

Leave a Reply

Hi Silvia. If the loan is interest-free but not between related parties, how would the impairment requirements of IFRS 9 apply? Would such a loan have a significant financing component? If not, can the simplified approach be applied to it? Is it right to initially recognise the asset at fair value? If so, what happens to the difference between fair value and actual pay out?

Hi silvia, great piece and helpful.

thank you.

Hi Silvia,

Thank you for the update. It is really useful.

Hi Silvia, Interesting debate. Assuming amortised d cost can be applied (with which I do not agree) there is a fair value issue. The article says ” In this case, the effective interest rate of the loan is zero and the loan’s fair value is simply its nominal amount of CU 10 million.”. However, a third party would never value this loan at nominal value. The interest rate of a loan to a property development company with an embedded high-risk profile would be rather high, even if the assumed maturity would be one day. Even banks ask interest for intra bank loans with such a term. So, the initial fair value would be below par and hence an internal rate of return would be available, assuming a one-day time horizon. This would create a loan with a variable interest rate (fluctuating with market interest rates) and with accrued interest at year-end. If there is no intention (or ability) to pay this interest is this a credit loss or a gift?

But do not agree with the amortised cost approach anyway, because the loan does not meet the demands of IFRS 9.4.1.2.(b) demanding specified dates, solely payments of principal and interest ( it says “and” not “or”). Even in case of a non-written contract the auditor would have to ask a confirmation of both the management of the parent and the subsidiary about the nature of this loan, which would make it a written contract.

So the only workable option seems to value this loan at fair value through P&L. Not doing so seems to walk into a minefield of problems

Thanks for the comment. It seems that you are the only one as far as I know who does not agree with amortized cost classification in this case. Maybe it would be worth for you to raise your issue to IFRS Interpretation Committee and ask for the official standpoint.

In relation to fair valuation – I slightly changed the wording in that sentence to avoid confusion (although the original wording was just as good as it was) – but the result is still the same. To me it is also a bit counterintuitive, however after reading loads of guidance and especially IFRS 13, I think that the initial valuation is simply the transaction price – exactly due to on-demand feature and thus extremely short period over which you would discount the cash flows to present value. For long-term loan yes – you discount it with market interest rate, book the gain/loss on the transaction and accrue interest in line with the effective interest method. For on-demand loan, if you hypothetically discount the nominal amount over 1 day to present value, and that same day (ON-DEMAND loan, NOT one-day maturity) you would need to book that same interest as earned revenue (yes, amortized cost) and then discount again and again book the revenue… you get the point. Again, please refer to any guidance on this topic (by FRAS Canada – the link is in my comment above, or by Big4) or you can even ask this question to the IFRS Interpretation Committee to get their viewpoint. I have nothing more to say to this.

Could I check if this loan should be recorded under equity or loan payable under the creditor side?

Thank you.

Liability at the debtor’s accounts. If this is equity – then IFRS 9 does not apply at all.

Hi Silvia,

Thanks for the update. Its much appreciated if you could ellaborate more on how did you arrive at the probability of default for rpt? And whar

Are the forward looking informations?

Thanks for this article : )

Amortized cost is not applicable in my opinion because IFS 9 par 4,1,2.b demands specified dates to cashflows that are solely payments of principal and interest on the principal outstanding. Measurement at fair value thorigh OCI demands the same as for repayment of principal and interest. Remains to value at fair value through P&L (see IFRS 9 par. 4.1.4). That introduces another issue, because the fair value in the seperate financial statements of the parent of a receivable without a maturity date and without interest rate might be less than initially transferred tot the subsidiary. (a kind of opportunity cost for the parent). Of course a loss is eliminated in the consolidated financial statements

Dear Andre,

thank you for your opinion.

However, I beg to disagree. The loan does not need to be at fair value through P/L, because no interest rate and no specific dates for future cash flows do not make it to fail SPPI test. SPPI test does not tell us that an asset MUST have cash flows solely from interest and principal repayment. Instead, it tells us that IF the asset has cash flows on some specified dates, those must come solely from those 2 items and not from any other item (like resulting from borrower’s performance or so). This is a common misunderstanding of SPPI test. All best, Silvia

I never read or understood it is IF the asset has cash flows instead of it MUST have cash flows. Silvia, after reading it over and over a few times I can now see where your interpretation comes from as 4.1.2A(b) states “the contractual terms of the financial asset give rise…”, it does not state “there must be contractual terms of the financial asset that give rise…”. The fact the the words “must” or “shall” is not included in 4.1.2A(b) makes that contractual cash flows are not a requirement.

Hi Chantal, exactly as you write. Having contractual cash flows stemming from principal and interest is NOT the requirement. Many people understand it as a requirement – however, there is quite an extensive guidance on this topic on the internet – for example, look to FRAS Canada, IFRS discussion group meeting from January – right at the Issue 1 here: https://www.frascanada.ca/-/media/frascanada/acsb/ifrsdg-past-meetings/2019-01-10-classification-of-related-party-loans-en.pdf – this is just an example.

Excellent tip. Thank you Silvia!

Dear we final financial statements after reporting period so we assume next year reporting date as demanding date? Kindly guide me thanks.

I am not sure I understand the question – but you always need to perform the impairment testing AT the reporting date of the current reporting period (if the loan is on demand, that would be the maturity date).

If i take $100 loan and recognise a financial liability of , say, 80 where the balancing figure goes? I applogies if question seems so basic, financial instrumnt is new to me.

And why do you recognize a financial liability of 80?

Dear Silvia,thank you for your contribution. But still am confused why we took inter-company cash transfers considered as loans as there is no document,no interest rate and no demand for repayment to specify it as loan or financial asset.

So what is your suggestion?

Dear Silvia, please correct me if I am wrong,

Even though this is the interCo Cash Transfer between two related parties, per transfer pricing compliance, we still need to treat this as separate legal entity’s transaction —> A cannot lend money to B for free, we need to clearly determine if this is a loan (with interest), or it is an investment, we cannot just simply state it as interco receivable.

In A’s Balance Sheet, we have to book at as 1. Interco Loan Receivable (with interest) , or 2. Investment in related party.

Yes, something like that – apart from the fact that IFRS indeed do not examine the compliance with transfer pricing, so under IFRS – if the loan is interest-free repayable on-demand, its effective interest rate is zero, thus you have to book it that way (in its nominal). If you want to be compliant with your transfer pricing rules, then you should amend the terms of this type of loans. In other words – the problem may arise at the level of the loan terms, not at the level of its recognition under IFRS. However I don’t see a compliance problem here – if you treat this transaction properly in your tax income return (e.g. the parent will add fictive interest revenue to its tax return in order to pay tax, although there is no interest revenue due to zero interest loan).

The weak spot in the amortised cost approach remains the initial fair value of a loan to a non rated subsidiary. A third party will not measure such a loan at par, implying an embedded interest rate at inception.

My suggestion is just like inter-company fund transfer with out claimed to be paid.

And that is accounted how, in your opinion? Because in substance, it is either capital contribution or some sort of a financial asset (loan).

Thanks For Your Consistent Updates.

Please how do you treat this Inter Company Loans For Tax Purposes

That depends on your tax law, not IFRS – which I really don’t know.

Thanks Silvia for this write up. It makes a lot of sense, most especially for those of us in public practice

Hi,

I do not believe the loan must be classified at amortised cost. As per IFRS it is classified at amortised cost if purpose of financial asset is solely for repayment of principal and interest at specified dates. This loan has no clear “interest rate” or dates of interest and principal payment. Therefore, financial asset was not acquired for purpose of “interest” income. Therefore, cannot be classified at amortised cost. It is more appropriately classified through P/L or OCI as per company policy. Therefore, will be subsequently measured using fair value revaluation of financial asset. There is also the intangible benefit of maintaining relationship between parent and subsidiary to be considered.

Regards

Ray-yaan

Hi Ray-yaan,

thanks for your opinion. Zero interest rate does not make an asset to fail SPPI test – please read the guidance in IFRS 9. Your reasoning just does not make it. S.

That is correct Silvia. That a loan has zero interest does not cause it to fail SPPI test. Typically on day 1, the fair value of the loan is determined by discounting at market rate. The discount is accreted over time and the face value is paid at maturity.