Example: Construction contracts under IFRS 15

Ever since the new revenue standard IFRS 15 Revenue from Contracts with Customers was issued, I get one and the same question:

What happened to construction contracts?

They were guided by IAS 11 Construction Contracts, but you might well know that after 1 January 2018, IAS 11 became superseded – it does NOT apply anymore.

Under the new IFRS 15, construction contract is treated exactly the same way as any other contract with customers.

I know I know.

Sometimes it’s hard to apply and imagine what it looks like.

Therefore in today’s article, I would like to show you HOW you should account for construction contracts under IFRS 15.

Plus, I will illustrate everything on an example with journal entries and calculations.

What do the rules say?

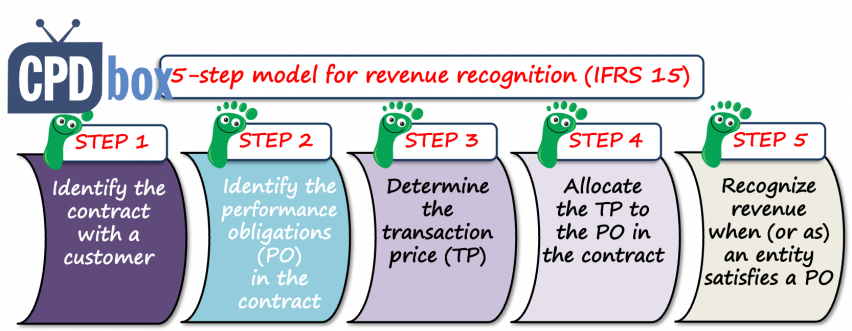

IFRS 15 prescribers the 5-step model for the revenue recognition.

You can also check out my IFRS Kit with detailed video tutorials about IFRS 15.

To sum up, here are the 5 steps:

- Identify contract with the customer;

- Identify the performance obligations in the contract;

- Determine the transaction price;

- Allocate the transaction price to the performance obligations in the contract;

- Recognize revenue when (or as) an entity satisfy a performance obligation.

If you enter into the construction contracts with your customers and you previously applied IAS 11, then you need to follow exactly these 5 steps under IFRS 15.

Let me show you straight on an example.

Example: Construction contract under IFRS 15

Construction company ABC signs a contract in June 20X1 to refurbish a building and install new windows with window blinds (let’s call it “windows”). Total contract price is CU 12 million.

Total expected contract costs are:

- CU 6 mil. for windows (purchased from external suppliers);

- CU 4 mil. for labor, materials and other costs related to the project.

As of 31 December 20X1:

- ABC handed over windows to the client, although the installation has not been completed. However, the client obtained control of windows.

- Other costs incurred to 31 December were CU 1 mil.

Just before the year-end, the client paid the first progress payment of CU 8 mil.

How should ABC account for this contract as of 31 December 20X1 in line with IFRS 15?

Let’s follow the 5 steps for the revenue recognition.

Step 1: Identify the contract with a customer

It is very clear now, we have the explicit contractual agreement between ABC and a customer.

Step 2: Identify the performance obligations in the contract

You need to identify not only individual goods and services promised in the contract, but also determine whether they are distinct or not.

Again, I will not go into theory explanations here, you can learn about distinct/not distinct either in my article here or inside the IFRS Kit.

If the goods and services are not distinct, they can’t be provided one without the other one (this is very simplified explanation) and thus they must be treated as ONE single performance obligation.

According to ABC’s assessment, the reparation services, windows and installation of windows are ONE single performance obligation.

Most construction contracts will contain just ONE performance obligation, because the contract would be to build or construct something for the customer and is negotiated as a whole package where a customer has no choice than to get the full package from the supplier.

Sometimes it’s not true and you will have TWO or more performance obligations there.

In this case you must adjust your accounting accordingly as explained below.

Step 3: Determine the transaction price

The transaction price in ABC’s contract is CU 12 million.

This is clear, but in reality, you can have some variability involved, like progress or performance bonuses.

You should take these estimates into account, too based on their probability.

Step 4: Allocate the transaction price to the individual performance obligations

This is very easy here, because as ABC assessed in the step 2, there is just ONE single performance obligation and thus the whole transaction price is allocated to this ONE obligation.

If there would had been more than one performance obligations, then ABC would need to allocate the transaction price to them based on their relative stand-alone selling prices.

You can revise the short example in this article to make it totally clear.

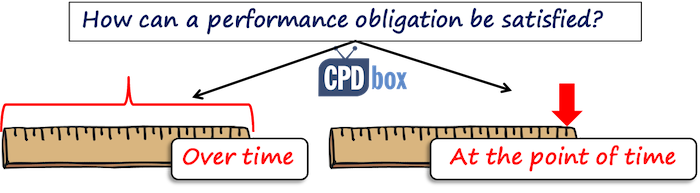

Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation

You should remember that the performance obligation can be satisfied either:

- At the point of time; or

- Over time.

The standard IFRS 15 lists a few criteria when a performance obligation is satisfied over time:

- Customer simultaneously receives and consumes as the entity performs;

- Customer controls the asset enhanced or created by the entity;

- Entity does NOT create an asset with an alternative use and has an enforceable right to payment for performance completed to date.

If you meet just one of these criteria, then the performance obligation is satisfied over time.

In most construction contracts, the performance obligations are satisfied over time and NOT at the point of time (although exceptions might exist).

In this case, you need to recognize revenue based on the progress towards completion.

How to measure progress towards completion?

You can use either input or output methods to measure the progress towards completion.

ABC uses input method, i.e. based on costs incurred to date.

Also, let me warn you about one significant factor specific especially for construction contracts:

There may be no direct relationship between your inputs and the transfer of control of goods or services to a customer.

Therefore, you should exclude the effects of any inputs from input method that do not depict your performance in transferring control of goods or services to the customer (par. B19 of IFRS 15).

Translated to human language and applied to this example:

ABC believes that costs of windows are significant item within total costs and including these costs to measure the progress to completion would not be appropriate, because it would certainly overstate ABC’s performance.

The reason is that the windows are purchased from the third party and the transfer of windows to the customer has no direct relationship with the other ABC’s work.

Therefore, progress towards completion will be measured excluding the cost of windows.

Carefully, because you should apply the resulting percentage of completion to the revenues excluding windows, too – just for the consistency!

Let’s measure the progress towards completion:

- Total costs excluding windows: CU 4 mil.

- Total incurred costs to date excluding windows: CU 1 mil.

- Progress to completion: CU 1/CU 4 = 25%

- Total contract revenue excluding windows: CU 6 mil. (CU 12 – CU 6)

- Total revenue to 31 December 20X1 excluding windows: CU 6 mil. x 25% = CU 1.5 mil.

Journal entries at 31 December 20X1

As we excluded windows from measuring progress towards completion, we will draft the journal entries separately for windows and for the remaining services.

Windows:

As ABC handed over windows and excluded them from measurement of progress towards completion due to potential overstatement, the revenue from sale of windows is recognized at the time of their delivery.

Purchase of windows by ABC (at the time of delivery from the supplier):

- Debit Inventories: CU 6 mil.

- Credit Suppliers: CU 6 mil.

ABC recognizes the revenue for windows at zero profit margin (equal to their cost – in line with par. B19(b) of IFRS 15):

- Debit Contract Asset: CU 6 mil.

- Credit Revenue from construction project***: CU 6 mil.

***Not the revenue from sale of windows – remember, the whole project is one performance obligation and we recognize the revenue under 1 caption in this case.

Cost of windows:

- Debit Costs of construction in profit or loss: CU 6 mil.

- Credit Inventories: CU 6 mil.

The remaining cost/revenues:

Labor costs, materials, etc. to complete the contracts are accounted for as contract costs (at the time when they are actually incurred):

- Costs to paint the building:

- Debit Contract costs (asset in balance sheet);

- Credit Employees (or suppliers or whatever is relevant)

- Use of paints:

- Debit Contract costs (asset in balance sheet)

- Credit Inventories

At 31 December 20X1, ABC needs to amortize the contract costs based on progress towards completion.

As the progress is measured by input method (incurred costs), all costs incurred to date are amortized.

However if different method is used to measure the progress to completion, then the company can amortize the cost based on the progress percentage.

In this case, at 31 December 20X1:

- Debit Cost of construction in profit or loss: CU 1 mil.

- Credit Contract costs: CU 1 mil.

Let’s recognize the revenue from “remaining” services (all except for windows).

We measured these revenues at CU 1.5 mil. using the progress towards completion (please see above).

Journal entry is:

- Debit Contract asset: CU 1.5 mil.

- Credit Revenue from construction project: CU 1.5 mil.

Finally, we need to account for the progress payment of CU 8 mil. made by the customer at the year-end:

- Debit Trade receivables (bank account, cash…): CU 8 mil.

- Credit Contract assets: 8 mil.

Let’s check the contract asset now. Its balance at 31 December 20X1 is:

- Contract asset that arose at revenue recognition (6+1.5): CU 7.5 mil.

- Less progress payment by the customer: CU 8 mil.

- The balance: CU -0.5 mil..

As the contract asset is negative at the end of 31 December 20X1, it became a contract liability and it should be presented within liabilities in the statement of financial position.

I personally prefer to see contract liabilities at the year-end, not contract assets, because:

- We have no credit risk as we have no performance completed to date which is not paid by the customer, and

- We don’t have to calculate expected credit loss and measure the impairment on contract assets – hurray!

Finally…

This is basically the method you should follow when accounting for your construction contracts.

I tried to make this simple as possible, but I can’t cover every single situation here.

If you have any questions, please ask them in the comments or you can even consider subscribing to our IFRS Helpline where I and my amazing team answer to your very specific question, issues, help you apply IFRS or even implemented for the first time. Just write me an e-mail if you’d like to get more information.

Thanks!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

126 Comments

Leave a Reply

Can you please help me with when to use which method of measurement?

How you have written that for contract liability – it is not paid by customer. it is paid right?

Is there anything like low progress ( say 20% using input methodd) on construction contracts under IAS 15.? How do we deal with such a situation regarding revenue recognition?

Hi Sylvia.

Thanks for article.

However I would like to how to present contracts asset or liability in the financial statement.

Thanks

Within current/non-current assets or liabilities, just as any other assets/liabilities.

Pеклама http://1541.ru/ и продажи в Pinterest для Etsy, Ebay, Amazon, Notify и др. от 140 usd. Тысячи за месяц Обратных, Вечных ссылок через размещение объявлений на 10-ки тысяч форумов 40 usd за месяц на 2 -х компах по 2-м базам сразу. Всего около 15 000 млн. форумов. Viber/whаtsapp +380976131437 ckайп evg7773 Telegrаm @evg7773

WEB/IT-специалисты Вёрстка сайтов, разработка разных web приложений, разработка скриптов и еще многие тысячиактуальных предложений по срочной работе для тех, кто тесно связан с WEB-IT-деятельностью.У нас опубликованы только самые свежие и реальные запросы.Всегда можно найти клиента тут , которые уже готовы заплатить за вашу работу – дело нескольких минут.!

Зарботок без проблем, получите бесплатно тестовую подписку.

I have some question on the above scenario….

1. How about booking the total cost of 1 Million initially like the inventory we bought initially we Debit Inventory and Credit Supplier — Debit Expenses and Credit Supplier? then we have to Debit Cost of Contract and Credit Expenses then recognise the Revenue….

2. i am confused with Expenses incurred here as you said we have to Debit Contract cost(Balance Sheet item) Credit Employees… You must follow Debit Expenses Credit Employees initially then Debit Contract Cost in P&L Credit Expenses and then Recognise the revenue by Debiting Contract Asset Credit Contract Revenue…

Kindly Clarify me

Hi silvia

Thank you for making easy to understand IFRS. Can you explain/make journal with figure for above example from inception to end of contract .Here i am somewhat vague to understand. I will grateful for your reply.

Hi Silvia,

How SaaS business should recognize its monthly revenue from implementation service. For Example: a contract is signed for $10,000 to implement a software for customer. The estimated hours required are 100 (20 hours per month). After the end of first month company spent 20 hours on implementation but then they find out that this work will take 40 hours more. However the contract price will remain the same at $10,000. In this case, should we recognize $2,000 ($10,000 x 20/100) in first month and from second month it should be $1,429 ($10,000 x 20/140)?

Hi Faizan, assuming the performance obligation is satisfied over time: if you picked an input method for recognizing revenue (which is logical in this case), then yes, you should update calculation prospectively as soon as you updated your estimates. However I would say the approach is similar to revising of useful life of assets – you would depreciate carrying amount over its remaining useful life. Similarly here, you would recognize revenue not-yet-recognized based on remaining cost to complete. In this example, in the second month, revenue not yet recognized is 8 000 (total 10 000 less 2 000 recognized in the first month); thus you would recognize 20/120*8 000 = 1 333 (20 = actual hours spent in the 2nd month, 120 = total revised estimate of 140 less 20 spent in the first month before estimate).

Thanks Silvia. That helps.

Hi Silvia

Taking on from your discussion about the road project above with Shailesh, if the Costs to fulfil a contract relate to unsatisfied future performance obligations, are direct project costs only and are deemed recoverable it would seem we can raise a WIP work in progress Asset and Credit expenses to the extent of direct costs incurred.

However just on the ‘control’ part.

If the construction company is deemed to meet 35c)

the entity’s performance does not create an asset with an alternative use to the entity (see paragraph 36) and the entity has an enforceable right to payment for performance completed to date (see paragraph 37)

It falls into the Performance obligations satisfied over time category.

If the entity also satisfies 35b)

The entity’s performance creates or enhances an asset (for example, work in progress) that the customer controls as the asset is created or enhanced (see paragraph B5);

Does the fact of customer control, mean NO WIP can be recognised? As the proposed WIP now fails the Asset definition being:

Asset is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity (IASB Framework).

?

Alternatively if the contract states that the contractor (road builder) controls the site whilst the project runs, ie controls physical access maybe via fences, stipulates how people can visit the site (even the client) such as visitor times, PPE to be worn then and if the contractor can only be kicked off under certain defined breaches – does this then mean, the proposed WIP can be recognised?

Need an opinion on this following case:

A real estate developer obtains a piece of land from a land owner to construct a 10 storied building in this land that will be fully rented to 3rd parties. After completion of the building in 3 years of time the real estate company will hand over the entire building to the land owner and will receive the right to obtain 50% of the rents from the whole building for a period of 10 years.

Account for the revenue recognition in the above case according to appropriate IFRS with relevant reference from IFRS.

Silvia, May I ask questions, In construction, there was retention clause 10% , How should I recognise revenue ? it should recognise transaction price after deducting retention amount or not and should I recognise it contract asset or not

Silvia, thank you very much for your reply. I agree with all the examples you mentioned. Now I better understand what you meant saying that “the company amortizes the cost based on the progress percentage”. It would be great if you make a podcast or an article incorporating this analysis. There is not much information about how to apply IFRS 15 and your explanations are very helpful. Thanks a lot.

Silvia, I would be very grateful if you could tell me a paragraph of IFRS 15 where it says that for output method the company shall amortise the cost based on the progress percentage. I really would be very grateful. This is very important for me.

What I wrote above It is not my statement, it is BDO’s statement. File “IFRS IN PRACTICE 2019, IFRS 15 Revenue from Contracts with Customers”, page 72. This file can be found in the public domain on the Internet.

Would you please explain why it is not correct. I really would like to make clear this question – how to amortise contract costs.

para 31, IFRS 15 “An entity shall recognise revenue when (or as) the entity satisfies a performance obligation by transferring a promised good or service (ie an asset) to a customer. An asset is transferred when (or as) the customer obtains control of that asset.”

para 35, IFRS 15 “An entity transfers control of a good or service over time and, therefore, satisfies a performance obligation and recognises revenue over time, if one of the following criteria is met: …”

So, a contractor satisfies a performance obligation over time (and recognises revenue over time), if and only if it transfers control of a good or service to the customer over time. Contractor cannot recognise an asset in balance sheet at the reporting date (contract costs or work-in-progress) as control has been transferred to the customer. If contractor retains control, then it shall recognise revenue at the point in time.

Dear Julia,

Now I see what you are referring to, but OK let me make this more precise. First of all – you did not copy the full BDO’s comment, which precisely says in the first sentence: “For performance obligations that meet the conditions for over time recognition of revenue, an entity would not recognise any work-in-progress under IAS 2 Inventories.” Thus they refer only to situations when revenue is recognized over time, not at the point of time (here you will have WIP under IAS 2), and also – they are referring to work in progress under IAS 2 Inventories and NOT contract cost as such (as I am referring to in my article). There can be many different contract costs, not just those related to inventories. The first sentence of your quote was exactly what I did not agree with.

Let me analyze a bit:

Under par. 95 of IFRS 15, you can capitalize only costs that relate to satistying the performance obligations in the future, but not to past performance. This is crucial and very important – this implies, that yes – if the costs that the constructor incurred relate only to performance obligations that have already been satisfied – then yes, these costs can be expensed. And, in the case of constructing the building, when you are measuring progress towards completion by reference to inputs (costs), almost all costs are expensed when incurred because in general almost all costs relate to satisfied performance obligation. My example is exactly solved this way (for practical reasons I booked contract costs first to monitor them, but they are all expensed at the year-end).

The same day I received another interesting question from Shailesh (just above your comment) – please read it. They were constructing the road, in total 100 km, they incurred cost for 60 km, but certified only 40 km. Now, how do they measure progress towards completion? If this is based on certified work (by the client), then would you agree that they should recognize the revenue just for 40 km (and this is different method from input method)? Let’s say that this contract said that the client would pay for the road based on n. of km approved and certified, while all other conditions for recognizing PO over time are met. And my next question – would you agree that recognizing revenue for 40 km, but expensing ALL costs for 60 km would create inconsistency? Because, those 20 km are not certified yet, maybe there is some other work to do, I don’t know – but it seems that this performance obligation for 20 km has not been satisfied yet and yes, in this case you have work in progress (or cost to fulfil a contract). Therefore would you agree that the comment about expensing all contract cost is just wrong for some situations?

BUT!!! The question is whether this method of measuring progress is OK, because it creates work in progress for the goods that have already been controlled by the customer. In my opinion, output or revenue methods of measuring the progress are in many cases just not OK to apply.

However, there can be a situation, when for example, road construction company hired a consultant that made a project for all 100 km of roads. They paid him let’s say 100 000 USD. Now, clearly, this is a directly attributable cost and a part of this project relates to a performance obligation that has not yet been satisfied – to 40 km of roads that haven’t started to be constructed yet. In your opinion – is it OK to expense all consultant’s cost? So here clearly, “work in progress” is created, because the consulting work related to those 40 to-be-constructed km of roads is a “work in progress” for the goods that have not been controlled by the customer yet. In this case, it is OK to have “work in progress” (I better call them contract costs, because that’s what they are) even in the situations when a performance obligation is satisfied over time.

Therefore, it is all about assessing whether the costs incurred relate to past performance or to future performance and unlike BDO, I would definitely not generalize that all contract costs shall be expensed as incurred – this is where I don’t agree with your first statement (not BDO’s).

Finally to respond your question – paragraph 99 says: “An asset recognised in accordance with paragraph 91 or 95 shall be amortised on a systematic basis that is consistent with the transfer to the customer of the goods or services to which the asset relates.” – reading in between the lines, isn’t this systematic basis equivalent to progress towards completion in some cases? It perfectly fits to the project by the consultant I outlined above.

Sorry for this long response, I just felt that some analysis would be better here – would you agree if I make a podcast episode from this question? It would be interesting for other readers, too.

Hi Silvia,

Thanks for your wonderful explanation..

What would be the journal entries for the above example (100Km of road construction)?

Hi Silvia,

Thank you for your article. Let me make a comment.

You said:

“However if different method (input method) is used to measure the progress to completion, then the company amortizes the cost based on the progress percentage.”

This is the percentage of completion method under IAS 11, not IFRS 15.

Under IFRS 15 all costs are expenced as incurred whatever method (input or output) is used. This is because the fundamental principle underlying over time recognition is that control of the good or service is transferred to the customer continuously as the vendor fulfils its contractual obligations. Therefore for performance obligations that meet the conditions for over time recognition of revenue, an entity would not recognise any work-in-progress under IAS 2 Inventories. All such costs would be expensed as incurred under IFRS 15.

No – I think that this part of your statement is wrong – at least I do not agree: “Under IFRS 15 all costs are expenced as incurred whatever method (input or output) is used.”. Please, read paragraphs 95 and following related to costs to fulfil a contract. And, I am not commenting on the rest of your statement, because that’s just not how it works.

Dear Silvia, Thank you for enlightening our understanding with nice practical example. I need to understand if there was road construction of 100km (total cost say USD100,000)and certificate of completion has been issued for 40km and cost incurred is for about 60km (USD60,000). In this scenario how much revenue will be recognised? Performance obligation is copletion of full road but payments released for each stage certified. Thank you

It depends on which method of measuring progress to completion you (or your CFO) selected. If it is based on cost, then recognize 60%. If based on certificate of completion, recognize 40%. However, you must justify the selection of the most appropriate method. It depends on your contract – how are you satisfying performance obligation? Over time? At the point of time? I would have to see the contract to make a conclusion.

Hi Silvia,

Thanks for your nice explanation on IFRS 15. A quick clarification required how revenue should be recognised in the books of supplier of manpower services company? Manpower services are being provided to construction companies/real estate developers and billed on a contractually agreed fixed monthly price based on resource utilisation/staff deployment.

The question: Should revenue be recognised on a monthly basis when services are rendered (satisfaction of performance obligation) OR should it be recognised over percentage of completion of the project being constructed by the 3rd party developers?

Please elaborate and many thanks in advance. Regards

Hi Josh, it depends on the specific contract. If the performance obligation is to provide the recurring service on a monthly basis, then it seems that the performance obligation is a series of services that are substantially the same and have the same pattern of a transfer to a customer and in this case, you can recognize revenue on a monthly basis. However, if you agreed in your contract to provide certain volume of different service during some period, then you would need to calculate the percentage of completion. Anyway – both methods should give you very similar results (if not the same).

Dear Silvia,

As per IFRS 15, the above examples has two separate performance obligations. The supply of windows and installation as they are distinct goods and services. How can we ignore this and follow the norm in the industry.

They are not necessarily distinct from the contractual point of view, but that was not the topic of this article.

Hi,

Company A contracts company B to build a plant at a cost of usd 20. USd 18 is paid upon completion and the balance of USd 2 is retained by company A for 3 months after completion (as renten tion fee).

How does company A account for the fee if at the end of the financial year usd 18 has been paid but the renten tion period is yet to lapse hence usd 2 is still outstanding?

will it be right to accrue the usd 2?

In construct, if the company received the advance payment from the contractor, what is the treatment as per IFRS 15.

Please note the advance payment received at the time of inception of contract. Percentage of completion is 0%

If the company did not do anything, just received a payment, then it’s a contract liability.

what if the company has done some work. what is the treatment?

Hi Silvia, Can you explain how to account for mobilization advances ?.

Hi Silvia, how will you recognize revenue for a certificate of say 3 million raised within the first year of the contract based of progress for contract with a total contract price of 5 million which is supposed to be completed in 3 years.

Hi Silvia, how IFRS 15 deals with the contract with uncertain outcome i.e. outcome of a construction contract cannot be measured realiably. In previous standard, the revenue recognised would be equal to cost provided that it is probable that the cost is recoverable. How should we deal with uncertain contract in IFRS 15? Thanks.

Hi Silvia, How IFRS 15 deals with Collectability of the sale proceeds or contract asset.

How credit risk and expected credit loss to be accounted?

I am a construction company and we issue performane guarantee and performance bonds to our clients to ensure them that we will complete contract also they keep retention money for one year post contract. So what wwill be entries for these three?

Cost of windows:

Debit Costs of construction in profit or loss: CU 6 mil.

Credit Inventories: CU 6 mil.

Is this cost recognised at time of purchase of window ? If so then why inventory is credited as that time of purchase it will still be in inventory.

But if its recog at year end then why the cost/expense is not recognised at time of purchase when payable is recorded?

I will be very thankful for your reply.

Is nt this entry should be

debit as inventory and

credit as supplier/payable

Instead of

Costs to paint the building:

Debit Contract costs (asset in balance sheet);

Credit Employees (or suppliers or whatever is relevant)

As contract cost is entered twice one at time of purchase of paint and other when paint is used.

Sscond, can you please also mention the time of passing entry for windows.

1) Accounting – no, my entries are correct, please revise once again (when the paints are used, contract costs are in P/L, not in the balance sheet).

2) I am not sure what you mean – I think it is mentioned up there. S.

Hi Silvia,

Kindly advice for the below point.

1. is it possible to recognize advance payment as revenue in Retrofit project?

In general no. You should recognize revenue either at the point of time, not over time and it has not much to do with payments themselves.

Hi Silvia,

Thanks for your explanation. It is simple to understand. However, I would like to inquire for input method should borrowing cost include in computation for percentage of completion as well?

Like :

Total costs : CU 4 mil. Total borrowing cost: CU 1 mil

Total incurred costs to date :CU 1 mil. + borrowing cost incurred CU0.5mil

Progress to completion: CU 1.5/CU 5 = 30% or remain CU 1/CU4 = 25%

Total contract revenue excluding windows: CU 6 mil. (CU 12 – CU 6)

Total revenue to 31 December 20X1 excluding windows: CU 6 mil. x 30% = CU 1.8 mil. or remain CU 6mil x 25% = CU 1.5mil

Hi Silva, thanks for the excellent article. What I am not so convinced is the example given in your article. It does not fit into a typical construction contract of physical asset, like a contract for construction of a building. The example is more of a service contract for refurbishing and installing windows to enhance an asset that is already owned and controlled by the customer. This is probably the rationale in B19 and IE 95-100 of IFRS 15 to split windows (goods) and services.

In a typical construction contract of physical asset that bundles equipment, materials and services (labour and overheads) in a single performance obligation, do we apply the same approach to allocate revenue to equipment delivered to the construction site on commencement? And if there are many items of equipment that will be delivered progressively over time to the construction site, are we required to recognise revenue at cost amount each time an item is delivered? Thanks.

Hi Tan,

I would say that contrary to what you wrote, this is a typical construction contract of physical asset – however, I made it more difficult here by twisting the input method a bit. Please note that here, there is also just one performance obligation – only the progress towards completion is calculated a bit differently, separately for windows from the rest, as bundling windows with the remaining service would simply not depict the real performance.

In reality you should assess yourself whether such subdeliveries depict your performance or not (in some cases, you would indeed need to calculate progress towards completion separately for certain parts of the contract). S.

Hi Silva. Thank you very much for your clarification. Allow me to ask another question on your ABC Example. If the contract has no enforceable right for payment, we need to apply the so-called completed contract method i.e. revenue recognised at a point in time rather than over time. In this case, do we still need to recognise revenue for the 6m cost of windows delivered to the customer (presumably control of the windows has passed to the customer)? Thanks.

Dear Silvia,

Is there a Template with set of questionnaire to implement IFRS 15 in an organisation? Like a model questionnaire to begin working on the implementation.

Hi Hemant, yes, I guess so. I would try searching Big4 materials as the first step.

Hi Silvia,

Yesterday, a friend of mine referred me this website. Today I am here and straight away on IFRS 15. I found this explanation of Construction Contracts revenue accounting totally helpful.

Thank yo so much!

Hi Silvia

Regarding the cumulative catch up method, could you provide example how to do it?

Regards

Arif

Hi Silvia, I have one doubt regarding the revenue recognition for those windows in your example. Suppose the customer has not obtained control of the windows and control is transferred only when the windows are installed. Also assume that the windows have unique designs, made specifically for this project by ABC. Now, as per the previous Standard, ABC can recognise revenue for the cost of windows, since the cost incurred in relation to the windows can be said to be specifically incurred for the refurbishing project (even though control has not been transferred). However, in IFRS 15, I understand that revenue is recognised for windows to the extent of their cost, provided the “control” has been transferred to the customer – my doubt is, what will be the treatment in IFRS 15, if control has not been transferred to the customer in respect of these uninstalled materials (windows)? Should we recognise no revenue or recognise some revenue, considering that specific contract expenditure has been incurred? Kindly provide your views on the same

Hi Rishidar, if ABC is going to make some work on the windows, then it may be the case that there will be direct relationship between ABC’s inputs and the transfer of control of goods or services to a customer. In other words, no need to treat windows separately as in the above example and you would not exclude windows from the input method. Thus windows would be treated just as the remaining project, based on the progress towards completion and as such, you would recognize revenue based on the progress towards completion at the year-end on all project (we all agree that the performance obligation is satisfied over time).

Hey Silvia, thank you very much for an excellent example, I am wondering why did you allocate the revenue excluding the windows on the bases of the whole contract value ie C 12 Million rather than C 10 Million ( part of the profit margin was included when you did that). Did you assume that there was no margin on the windows purchased from the suppliers or what,

I think I answered that in the article above.

Hey Silvia, Great insight to IFRS 15. I was wondering how you would calculate the Revenue and Cost of sales in the next year? Would it be Revenue= (contract price*current year % completion) less the amount of revenue from prior year OR contract price*change in %completion? And would cost of sales= estimated costs*change in %completion OR (Estimated costs*current year %completion) less prior year cost of sales?

Hi Silvia,

If i show Contract Asset & Contract Liability in the financials not netting off, that is also correct?

Yes, can be, if they relate to different contracts then you should not net off.

Thank you for very insightful sharing. By the way, do you have share before this how to recognised revenue based on output method which i think it very important for me because all of my construction project using output method . I think i have applied the wrong way the output method because i just use general provision to hit expenses to get let say 10% percentage of completion . For example, the progress at site showed 10% from consultant report and my revenue with customer worth 1 Mil and my budget 0.8 Mil. In order for me to recognise 10% revenue, i also hit expenses 10%. So it can be concluded actual cost divide by budget 0.08 Mil/0.8 Mil equal to 10%. is that appropriate method to recognise using output method.

Thank you silvia , you explained very well

could you please tell me when the networking equipment’s are on “leased to owned” business model (ie; after certain years ownership of equipment’s deployed to run the network will be transferred to buyer ) . In such cases should we apply IFRS 15 or IAS 17 leas standard

Thank you Silvia a great article!

could you please, explain what is the difference between the control approach and risk and reward approach?

Hi Sylvia, u explained very well with simple example. Now in the above example the cost for the first year will be high as we are recognizing entire windows cost but not revenue for that. So net profit may not be in trend right? And when will we recognize the revenue for windows, is it at the completion date??

Surya, but yes, we recognized the revenue for windows in the first year in the amount equal to its cost (zero profit margin). S.

Hi Silvia but if it is cost plus margin ,how the double entry would be ya?

Thank you Sylvia.

Hi Sylvia,

Thank you for the explanations!

Hi Silvia,

We are in the business of selling already developed and serviced residential stands. Customers initially pay 50% deposit and the remainder over installments. Once the customer has finished paying the full amount, an agreement of sale is signed by both parties. how would i apply IFRS 15?

Well, this is not so much about the construction contracts then – business is simply selling inventories. Here, from what I see, the control is transferred to the customer at the point of time, so you would recognize revenue when you transfer control of the apartment to the customer (in one amount). S.

Say , We have a proposed building of 15 floors. 10 of whom are already sold but we have so far constructed till 4th floor.

Assumption- contract price for each of the floor is 100,000 cu. Signing amount for sold floor space is 70,000 cu (for 10 sold floors) Cost incurred so far; basement-80,000 cu, cost for each floor 50,000 cu (up to 4th Floor).

How will we recognize revenue for each sold floor?

Sahil,

I can’t say from this information how because I haven’t seen what you wrote in your contracts with customers. You need to assess first whether the control is transferred over time or at the point of time – in this type of business it can be both. Please read more in this article (find real estate part). S.

Hi,

Want to know can IAS 11 can be applied on the networking business. Entity sells the equipment and install the same on various sites.

Well, you don’t apply IAS 11 anymore, it is not valid since 1 January 2018. But yes, you apply IFRS 15 on networking business, in a similar manner as described here (but this is specifically described for previous construction contracts).

Hi Silvia,

Your demostrated example is crystal clear and easy to understand. I would like to ask if we use “Output Method”, do we need to exclude the elevator “revenue” (say 0% profit) from calculating percentage of completion?

Hello, I have read your article and it is full of information with clarity. I have some questions please guide about the following

If a company own land and start to construct the residential building for sale purposes so how I have to account for the followings

1-Land-Initially need to recognize as Assets or what else? Subsequently also…?

2-How to recognize the expenses incurred in relation to the construction like Govt. Fee, Consultant & Architecture fee Fee & Legal Consultancies?

3-If we can categorize the expenses between Direct and Indirect expenses then how to account for?

Hi Faisal,

well, if there is no customer contract at the beginning, but a company develops property for sale, then it’s not a construction contract. The company is in fact developing inventories, if the sale of apartments is a main revenue-generating operating activity. As for capitalizing, the fees that you are mentioning are eligible for capitalizing as they are directly attributable to construction, and the answer to the question n. 3: well, I’m not sure what you are asking for, but as you are developing inventories, then you are using certain WIP accounts and allocation methods. I can’t answer longer in the comment. S.

Hi Silvia. Thanks for the great article. Can you please shortly explain what would customer book? Only advance paid (8 mil) or would he recognize also part as PPE – maybe elevators and some part of finished work?

Thanks

Hi Tanja,

the customer is acquiring PPE (property, plant and equipment) under IAS 16, so she must follow the recognition principles to book the asset. If they are met, then PPE is booked, if not, then advance payment. The customer must assess at which point she gets control of asset. S.

Saliva, dear can you tell me how if running bills are also treated as Advance???

Or customer should record its expense?

What an interesting and practical article. You are simply the best. IFRS master. Regards

Thank you!

thank you very good effort