Example: How to Adopt IFRS 16 Leases

In my last article I tried to outline the strategy and your choices when implementing the new lease standard IFRS 16 Leases.

I am grateful for many responses and comments I got from you. Almost all e-mails I received from you asked me to publish solved numerical example to see how to implement IFRS 16 in practice.

Therefore, unlike in my other usual articles, this time I’ll solve one example with one specific lease contract for you.

You might well know that the IFRS 16 affects mostly lessees who are involved in operating leases, because under the new rules they need to bring the assets from off-balance sheet to the daily light.

In other words, they will no longer be permitted to book all rental expenses from operating leases in profit or loss, but they will need to recognize the lease liability and the right of use asset.

Therefore, in this article, I illustrate the application of the full retrospective approach and modified retrospective approach to IFRS 16 adoption.

Ready for the example? Here you go!

Example: Operating lease in the lessee’s accounts under IFRS 16

ABC, the manufacturing company, needs to adopt the new standard IFRS 16 Leases in the reporting period ending 31 December 2019.

During the preparatory works, ABC discovered that the operating lease contract related to a machine might require some adjustments.

ABC entered into the contract on 1 January 2017 for 5 years, annual rental payments are CU 100 000 in arrears (that is, 31 December each year) and at the end of the lease term, the machine will be returned back to the lessor. The economic life of a machine is 10 years.

How can ABC restate the contract under IFRS 16 using both full retrospective and modified retrospective approach?

Use the discount rate of 3%.

Little note about the discount rate

If you are a lessee, then be careful about the selection of the appropriate discount rate, because its definition in IAS 17 no longer applies.

Here, the new definition in IFRS 16 says that you should derive the interest rate implicit in the lease from:

- The lease payments,

- The unguaranteed residual value,

- The fair value of the underlying asset and

- The initial direct costs of the lessor.

This is very hard and sometimes unrealistic, because most lessors won’t share the unguaranteed residual values and their initial direct costs.

Therefore, most lessees will need to use the incremental borrowing rate – that is, the rate at which they would be able to get the new borrowings for acquisition of the same asset with similar terms.

This is quite judgmental, but at least it’s more realistic than asking your lessor for additional information in most cases.

In this numerical example, let’s assume that given 3% is the ABC’s incremental borrowing rate.

Presenting the contract under IAS 17 and IFRS 16

Before you start drafting your journal entries to adopt IFRS 16 and cease reporting the contract under IAS 17, you need to see clearly how you reported that contract under both sets of rules.

Operating lease contract under IAS 17

Here, it’s very simple and straightforward: ABC accounted for all the lease payments from the operating lease directly in profit or loss.

Operating lease contract under IFRS 16

Under IFRS 16, ABC needs to recognize the right of use asset and the lease liability.

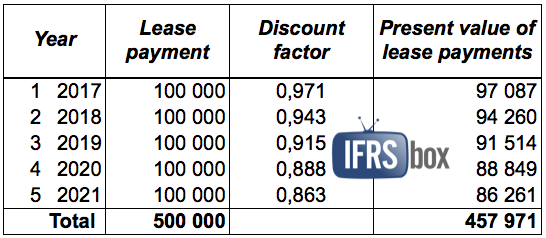

The lease liability is calculated as all the lease payments not paid at the commencement date discounted by the interest rate implicit in the lease or incremental borrowing rate.

I have done that for you in the following table:

Note: Discount factor in the first year is calculated as 1/((1+3%) to the power of year 1), etc.

Fine, we have the lease liability.

The right of use asset equals to the lease liability at the commencement date, plus lessee’s initial direct costs, plus some other things – but in this case, we have nothing like that, so let’s just say it’s the same as the lease liability.

Under IFRS 16, the initial journal entry would be:

-

Debit ROU (right of use) asset: CU 457 971

-

Credit Lease liability: CU 457 971

Subsequently, ABC needs to take care about 2 things:

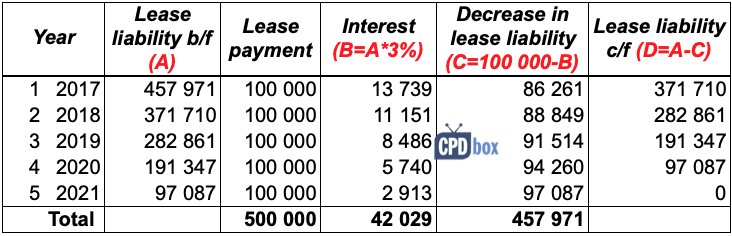

- Depreciation of the ROU asset: Let’s say it’s straight line over the lease term of 5 years, thus it’s CU 91 594 per year (CU 457 971/5).

- Lease payments: Each lease payment of CU 100 000 is split between the repayment of the lease liability and interest.

I’ve done that in the following table:

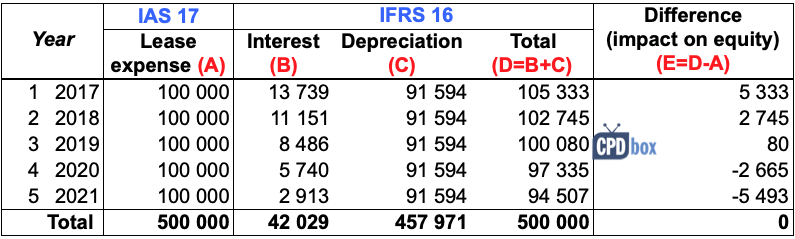

Compare the accounting under IAS 17 and IFRS 16

To calculate the adjustment in equity related to this contract, let’s summarize the profit or loss impact of the lease in individual years under both IAS 17 and IFRS 16:

As you can see, total profit or loss impact of both IAS 17 and IFRS 16 application is the same CU 500 000, however, the timing is a bit different.

So, now we have set everything and let’s see how to make adjustment in equity and how to present the restatement under both full and modified retrospective approaches.

I described both approaches in this article, so I won’t repeat it here and let me focus on numbers.

Full retrospective approach

ABC adopts IFRS 16 in its financial statements for the year ending 31 December 2019, and that means that the transition date is 1 January 2018.

We need to restate all numbers for the comparative period, too.

Most of the work has been done above (see tables 1-3), so I’ll draft the journal entries here:

- Restatement of opening balances of the earliest period presented (that is: BEFORE 1 January 2018):

- a) Recognizing ROU asset and lease liability:

-

Debit ROU (right of use) asset: CU 457 971

-

Credit Lease liability: CU 457 971

-

- b) Reversal of the lease payments before 1 January 2018 under IAS 17 (there was just one):

-

Debit Cash: CU 100 000

-

Credit Retained earnings (equity): CU 100 000

I know, I know! No cash moved! Wait until we are done with this exercise. This is just to illustrate that in fact, you are reversing the “old entries” and then making the “new entries”.

And why retained earnings and not profit or loss?

Because you are making this entry on 1 January 2018 and at this date, all profit or loss accounts from 2017 were transferred to the retained earnings.

-

- c) Accounting for the lease payments before 1 January 2018 under IFRS 16 (there was just one):

-

Debit Lease liability: CU 86 261

-

Debit Retained earnings (equity): CU 13 739 – this is for the interest

-

Credit Cash: CU 100 000

Note: The numbers come from table 2 for the year 1 (2017).

-

- d) Accounting for the depreciation of the ROU asset before 1 January 2018 under IFRS 16 (there was just one year):

-

Debit Retained earnings (equity): CU 91 594

-

Credit ROU asset: CU 91 594

-

In fact, you can do all 4 entries in one adjustment and it would look something like:

-

Debit ROU asset: CU 366 377 (CU 457 971 less depreciation of CU 91 594)

-

Debit Retained earnings in equity: CU 5 333 (-100 000+13 739+91 594, or see table 3 for the year 1)

-

Credit Lease liability: CU 371 710 (CU 457 971 less the lease liability repayment of CU 86 261, or see table 2 for the year 1)

In reality, you would adjust in in 1 single entry, but I wanted to show the rationale behind, its breakdown and logic.

- a) Recognizing ROU asset and lease liability:

- Restatement of the comparative period (year 2018):

Here, you are only restating the 2nd lease payment made. As I’ve illustrated the breakdown of all entries above, let me show you just one summarizing entry here:

-

Debit Lease liability: CU 88 849

-

Debit Interest (profit or loss of 2018): CU 11 151

-

Debit Depreciation (profit or loss of 2018): CU 91 594

-

Credit ROU asset: CU 91 594

-

Credit Operating lease expenses (profit or loss of 2018): 100 000

The numbers come from table 2 for the year 2 (2018).

-

- Restatement of the current period (year 2019):

Normally, you would have already applied IFRS 16 in 2019, but if not and you are doing everything during the closing works, here’s the entry:

-

Debit Lease liability: CU 91 514

-

Debit Interest (profit or loss of 2019): CU 8 486

-

Debit Depreciation (profit or loss of 2019): CU 91 594

-

Credit ROU asset: CU 91 594

-

Credit Operating lease expenses (profit or loss of 2019): 100 000

-

OK, that’s for the entries and adjustments.

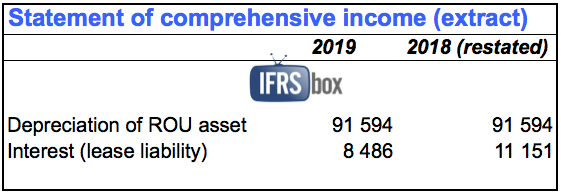

If you apply the full retrospective approach, the problem is that you have to report the comparative period – year 2018 in this case – under both IAS 17 and IFRS 16:

- In the financial statements for the year ended 31 December 2018, you are still applying IAS 17, so your current numbers for 2018 are under IAS 17, but

- In the financial statements for the year ended 31 December 2019, you apply the new IFRS 16 and also your comparatives need to be stated under the same rules – thus you need to book the above entries n. 1 and n.2 carefully.

How would your financial statements look like?

Here you go:

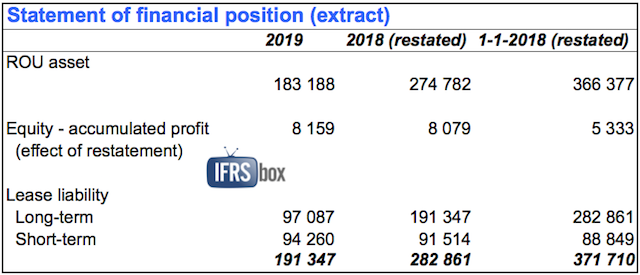

The statement of financial position (extract) is here:

All the numbers related to the lease liability come from table 2 above.

The extract from profit or loss statement:

Now, let’s show the modified approach.

Modified retrospective approach

Under the modified approach, ABC needs to make an equity adjustment on 1 January 2019 – that is at the beginning of the current reporting period.

Comparative numbers remain the same as presented before – so no restatement.

This is a way easier method to apply than the full retrospective approach, because you do not restate the previous years’ numbers.

However, the price for this relief is lower comparability.

It is quite difficult to compare current year under IFRS 16 with the previous year under IAS 17 and it does not say much about how your leases developed.

Just see it for yourself in the below extracts from the financial statements.

Before you jump into the journal entries, please note that I assumed the same discount rate at the date of application as original discount rate – just for the sake of this example, because thus I don’t need to recalculate the amounts from full approach.

In reality, you need to measure the lease liability under modified retrospective approach as present value of the remaining lease payments discounted by the rate at the initial application. You can revise the same example taking different discount rates into account here.

In this example, lease liability is effectively measured as present value of the remaining lease payments discounted by the original discount rate (as taken from above).

Let’s draft the journal entries:

- Restatement of opening balances at 1 January 2019:

- a) Recognizing ROU asset and lease liability:

-

Debit ROU (right of use) asset: CU 457 971

-

Credit Lease liability: CU 457 971

-

- b) Reversal of the lease payments before 1 January 2019 under IAS 17 (there were two):

-

Debit Cash: CU 200 000

-

Credit Retained earnings (equity): CU 200 000

-

- c) Accounting for the lease payments before 1 January 2019 under IFRS 16 (there were two):

-

Debit Lease liability: CU 175 110

-

Debit Retained earnings (equity): CU 24 890 (= interest)

-

Credit Cash: CU 200 000

Note: The numbers come from table 2 for the years 1 and 2 – you need to make a total for these 2 years (2017 and 2018).

-

- d)Accounting for the depreciation of the ROU asset before 1 January 2019 under IFRS 16 (there were 2 years):

-

Debit Retained earnings (equity): CU 183 188

-

Credit ROU asset: CU 183 188

-

-

Debit ROU asset: CU 274 782 (CU 457 971 less depreciation of CU 91 594*2)

-

Debit Retained earnings in equity: CU 8 079 (-200 000+24 890+183 188, or see table 3 for the years 1 and 2)

-

Credit Lease liability: CU 282 861 (CU 457 971 less the lease liability repayments of CU 86 261 and CU 88 849, or see table 2 for the years 1 and 2)

Similarly as with the full approach, you can make just one aggregate entry instead of these four:

- a) Recognizing ROU asset and lease liability:

- Restatement of the current period (year 2019):

It’s the same as under the full retrospective approach and if you have accounted for your operating leases under IAS 17 during the whole 2019, then you need to do this adjustment:

-

Debit Lease liability: CU 91 514

-

Debit Interest (profit or loss of 2019): CU 8 486

-

Debit Depreciation (profit or loss of 2019): CU 91 594

-

Credit ROU asset: CU 91 594

-

Credit Operating lease expenses (profit or loss of 2019): 100 000

-

Note: Here, I measured the ROU asset as if IFRS 16 has always been applied – in this case, it was easier for me as I have already calculated all the numbers above.

However, you can measure your ROU asset in the amount of the lease liability. This would be even easier, because you would not have to recalculate ROU asset in the past. You would simply calculate the lease liability (=present value of the remaining lease payments) and that’s it.

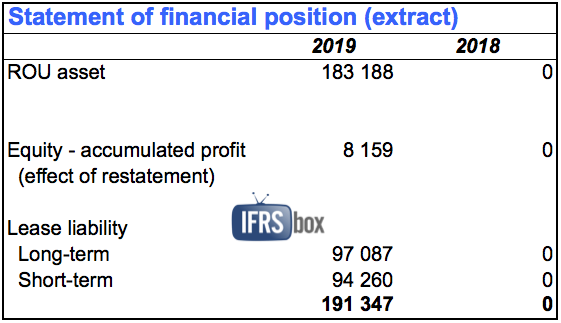

What about the ABC’s financial statements?

Here you go:

The extract from the statement of financial position:

Please note that there are zeros for the comparative year 2018 – the reason is obvious. We are presenting the previous year under IAS 17 and there was no lease liability and right of use asset under IAS 17.

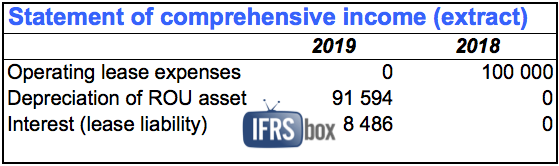

The extract from profit or loss:

This was just a basic example with a very simple and straightforward contract. If you’d like to learn more about IFRS 16, its application, adoption and see many practical examples solved in Excel, then I recommend checking out my IFRS Kit – IFRS 16 is extensively covered!

Also, here’s the same example illustrating different transition options and practical expedients, so check it out.

Any questions or comments?

Let me know below – thanks!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

284 Comments

Leave a Reply

Hi Silvia

Thanks a lot for the clarification. My question is, is it practical to get an incremental borrowing rate for a property lease which goes beyond 30-50 years. Because no loans are given for such a period of time. Kindly clarify.

Dear Silvia,

as I understood, under the simplified approach no entries to be made on 2018, it just one entry on the 1.1.2019 for transition purpose. is this correct?

Têm como me mandar estes exercícios em uma planilha em excel por gentileza

English please!

Most of the Lease contract under which payments are made normally in advance.

Then at the date of initial what will be the treatment of Prepaid Asset.

Hi. I am now struggling on this point. If my client’s office which the lease term over one year and all the lease payment paid in advance. Does it mean I don’t need to recognise the right- of- use assets for the lease due to 1.) there have prepayment to record the lease payment in advance; 2.) There have no lease liaility will be recognised in the financial position as no unpaid lease payment?

Hi Silvia,

Was wondering- lease contract is made by a yearly basis, but we will rent it next year. Is it considered as short-term lease?

Sandra, for this question, I recommend reading/listening to this Q&A session. S.

Hi Sylvia,

Thanks for the extremely helpful article.

Was wondering – If we were to measure the lease liability and ROU asset by computing the PV of lease payments as of 1 Jan 2019, does it mean that there is no need to restate the opening balances as at 1 Jan 2019?

Hi HY,

thank you! Yes, you do need to restate opening balances – these rules are just to simplify measurement for you. You need to restate the balances as described in the above example. S.

Hi Sylvia,

This example enlightened my understanding on the transitional provisions.

I have one question regarding the modified retrospective. If the operating leases is denominated in foreign currency at what rate should we remeasure to our functional currency. I understand lease liability being monetary item should be restated at each reporting period and ROU asset is non monetary so exchange fluctuations have no impact. But what about during initial measurement of these two components? Is it exchange rate rate as on date of commencement of lease or rate on date of initial application which would be on or after 1st January 2019

Hi Sylvia, great article! I do have a question after reading the 2 approaches though, and that is since the Modified Retrospective Approach you used takes it as if IFRS116 was applied all along, then why can’t the figures from “Restatement of opening balances at 1 January 2019” be used in the 2018 column of the SFP and SCI?

I noticed this as the journal entries would give the exact same result as the 2018 (restated) figures in SFP. The only issue here is SCI, since the Modified Approach would be combining 2 years of depreciation and interest instead of one year (since SCI is normally for an annual period). Could we just present the SCI figures in a separate disclosure under Notes to Financial Statements?

Under the full restrospective method, is the 1-1-2018 (restated) compulsory?

Nice article, with clear understanding of Recognition, Measurement, Presentation and Disclosures.

Please replace the blue letter (interest) to (depreciation) Under modified approach d),

Thank you for such a careful reading – that was my bad copying! 🙂

Hi Silvia,

Its been always helpful to consult your articles.

I have one question regarding the leases. How to treat if the yearly lease payments are increasing with a fixed amount.

For example if the lease payments are as follows;

Year 1: 1 million

Year 2: 2 million

Year 3: 3.5 million

Year 4: 4 million

Year 5: 5 million

Thanks,

Thanks Umar

I haver the same issue, my company leased a building for 20 years

the yearly rent is increased every 2 years.

We will be more happy if Silvia answered it.

Any fixed increment is part of lease payment should be considered now and discounted to obtain present value of lease liability.

Any fixed increase should be added to calculate PV of lease liability.

In your example, all each year’s payments including incremental to be discounted to get PV of lease liability.

Hi Silvia, thank you for cool instruction. But at the same time, using Full retrospective approach, I can’t get the same amounts of BS.Retained earnings (equity) comparing movements of bookings with Statement described by you.

BR,

Vasyl

Sorry, I can’t check how that could happen!

Hi Silvia,

Thanks for the article, but please let’s we go further…

Can you please share your approach in term of an invoice, when there are more details:

contract 3 years for car

Depreciation : 686

Interest :52,93

Management fee: 17

Road Tax: 16,36

Maintenance: 76,42

Tyres: 89,37

Nett monthly charge : 938, 08

My question is:

which components are included in deprecation of ROU?

and next issue was raised , when I am going through contracts is CPI ?

What about CPI if it is included in contract?

thank you

Br

Krystyna

Hi Krystyna,

I think that this is well covered in the IFRS Kit – please study the chapter about separating lease components from non-lease components (chapter 2 of IFRS 16). You have to do this right in the commencement of the lease and then you will treat each individual components in the same way. If you are a lessee, then you don’t even need to separate, but simply add everything up and treat it all as a lease (add up everything and see it as one payment).

As for CPI – consumer price index (inflation) – this is also very well covered in the IFRS Kit. Please study chapter #7 of IFRS 16, you will see the exact numerical example with payments increased for inflation. S.

Dear Silvia,

Thanks for the article. This is easy to understand.

Since property tax is part of the lease payment calculation in a gross lease, can you shed some light on how to deal with the annual property tax adjustment please?

Dear Silvia,

I have been able to follow this complex area based on your article(s) so WELL DONE.

for the only purpose of clarifying your article and not being petty:

There was a tiny copy/paste error that threw me a bit in the “Modified….” section where you referred to Debit Retained earnings (equity): CU 183 188 (= interest) where it should read Debit Retained earnings (equity): CU 183 188 (= DEPRECIATION) but I was able to decipher that from the full model further above.

Secondly in my Excel model I managed to calculate the discount factor as “=1/EXP(i*n)” it gives me some minor rounding errors but I think that is the right way to use that formula.

Thanks again – very very comprehensive.

Hi Silva,

If we have previously recognised a Dilapidation provision for our leased properties then should this be included in the ROU asset in accordance with IFRS 16. As a result, should the double entry be that we Dr ROU asset and Cr Retained earnings (i.e. adjustment through equity). Thank you.

Hi Silvia, i would like to ask, we currently have an operationg lease that terminates this year, December 31, 2018. Earlier this year, there was a bid for that same property, we were able to win the bid and were able to have a new lease for 5 years starting 2019. Do we still have to do the retrsopective application of IFRS 16? or can we just leave the past years as is and just treat this one as if a new lease, which technically is.? Thank you

Hi Lorebel,

if you apply the practical expedient, it will give you the same effect. You can just calculate the lease liability on the lease as at 1 January 2019 as the present value of future lease payments and take this amount as your right of use asset. S.

Thank you very much, we really appreciate it 🙂

Hi Sylvia,

First of all thanks for such a rich answer. I have one question. How do you calculate Discount factor in year 2 (0,943)?

Thanks again

Hi Slavoljub,

I believe the answer is in the note right below the table, but let me repeat: it is 1 divided by ((1 plus 3%) to the power of 2).

Hi Silvia

If we have a large number of property that we have signed Property lease agreements: These lease would have been established prior to Jan 1, 2019. The payments are paid periodically and today these leases are treated as Rental Expense.

Would we be required to recognize these leases under Right to Use (ROU) based on the PV of future lease payment obligation + any restoration costs that would be estimated?

Would we need to identify each Property individually and add these to a category called ROU under the Fixed Assets or would we need to create a New Category within the Financial Statements?

Dear Silvia, I am stuck with 3 different leases and need your help. As of 31-Dec-2017, I have following 3 leases together with their prepayment amount as of 31-Dec-2017 and annual lease rental amount:

Lease 1: Jan 2015 to Dec 2019 Annual rental $ 120,000 Prepayment $60,000

Lease 2: Jul 2016 to Jun 2021 Annual rental $240,000 Prepayment $ 40,000

Lease 3: Jan 2017 to Dec 2019 Annual rental $ 60,000 Prepayment $ 60,000

What I did, as of 01-Jan-2018:

I have reversed the prepayments by Dr RUA and Cr Prepayments and will depreciate RUA during the remaining period of lease.

I have discounted PV of remaining lease payments (Which are payable during 2018 – 2020).

Is it correct approach?

,

Yes, I think so. You should reverse everything and then if you apply modified approach, just discount the remaining lease payments and it is equal to ROU at 1 Jan 2018 – it means you applied one of the practical expedients at transition. S.

Thanks. Stay blessed.

The reduction in Prepayment as a result of the reversal of the prepayment of leases is it considered a cash item ? or non cash item? if its not considered a cash item do we need to add it back to the working capital

Hi, could you help solve a difference of opinion please? If you have a lease with 34 quarterly payments, paid in advance, would you consider the lease term to be (and therefore the interest and depreciation to be spread over) 100 months, because the last payment is made in month 100, or 102 months? Many thanks for any help on this!

Hi Silvia,

Great Sharing. Thanks a lot.

Could you please help me to give a solution as blows:

My Co. Rented a factory for 5 years and after 2 years passing making an infrastructure (child care) by own cost. So now can we considering the cost as lease Hold Improvements under IFRS 16?

we want to amortize within 2 years equally. Is it possible?

Again Thanks.

Hi Bappy,

is the infrastructure firmly attached to the factory? In this case, I agree. S.

Hi Silvia.

Thanks for reply.

Yes its attached with the factory.

Hi Silvia!

What if the rental of an office is for capital purposes? I mean, an area is rented for a group of people, providing a capital work (workers’s salaries are also capitalized). Do we need to use the IFRS 16, or capitalize the monthly payments as a part of the investment project? Or is there any other way to treat the Lease agreement.

P.S. The contract is made for one year with an automated prolongation option for additional year if not cancelled. It’s been 3 years for now that the initial contract hasn’t been cancelled (so it’s prolonged).

Thanks in advance.

Hi Natalia,

I publish weekly podcast with answered questions and the next week, I answer the question of capitalizing the rentals (episode n. 019). Maybe you should check that out. The short answer is no capitalizing. S.

Hi Silvia,

Thank you for this article. Could you help me to solve one issue. Take the scenario below.

Scenario:

Restaurant company sign property lease contract as a leasee. And monthly rent is calculated as basis of actual sales revenue with no fixed rent or even fixed rent is too small compared with variable rent.

Question:

Whether to recognize ROU asset or not if there is no fixed rent? If ROU asset should be recognized, what is the calculation logic?

Looking forward your precious answers and comment!

Thanks a lot!

Hi,

I have a query,regarding the same. if i take 30 year lease with monthly rental payment and escalation after every 3 yeras @ 10% on 01.01.2010.

If i wanted to discount it @10% monthly compounding rate i will get the finance cost which is more than actual rental period at initail stage and didnt get cleared at the end?

What will be the accounting treatment for the same i.e finance cost which is more than actual payment during initial stage.

Hi, thank you for the simple explanation. I have one example I am unsure of, if a company has a lease term of 5 years and at the end the residual value is £50K. If the company chooses to keep the asset and buy outright do we depreciate over the remaining life or write off in current period?

Hi I am just wondering do you need to use an inflation rate to get the FV of the lease payments before using the discount rate?

No, you are taking current lease payments into account. Adjustments for the inflation are done when the lease payments are adjusted and it is treated as the lease remeasurement. I have solved few detailed examples on this in my IFRS Kit. S.

Hi Silvia,

Great article, thanks. I was wondering if you could explain the below:

1. How do we treat rent free period in the lease liability calculation?

2. On the inception date, how do we treat the lease credit that is already in the balance sheet derived from from the rent free period (this was recorded in accordance with IAS 17)?

Your reply is very much appreciated.

Thanks

Dear Perminerjeet,

as soon as the asset is available for use to the lessee, lessor starts recognizing the lease receivable. In rent-free period, no repayments of principal are recognized, just interest is charged. You should adjust the effective interest method accordingly. I have solved very detailed example on this in my IFRS Kit. S.

Hi Silvia

Please could you explain the second point that Perminerjeet has asked?

2. On the inception date, how do we treat the lease credit that is already in the balance sheet derived from from the rent free period (this was recorded in accordance with IAS 17)?

Dear Abby, the response is still the same – it is simply included within the effective interest method and leased liabilities. The IFRS Kit brings detailed example on this. I am sorry, it’s not possible to give a detailed response in the comment. Thank you for your understanding.

Hi Silvia, are you referring to your example 4 – Var.payments? It’s a clear example but unfortunately I do not see the transition to IFRS 16 from a lease credit due to lease incentives under IAS 17. Is this lease credit transition reported in retained earnings?

Hi. This is a very informative article on IFRS 16.

I need little clarifications on the following issue:

An entity (ABC) is a first time IFRS adopter in 2018 (i.e., it will issue first IFRS financial statements as of Dec 31, 2018). ABC intends to apply IFRS 15 from 2017 (which is actually effective from 2018), accordingly, can it also early adopt IFRS 16 in 2017?

Suppose if ABC decides on modified retrospective approach under IFRS 16 then all the cumulative impacts would go to retained earnings as on 1 January 2017 (which is the opening balance sheet for the purposes of IFRS 1), right? In a similar way that all cumulative adjustments (entity adopts for cumulative catch-up basis) for IFRS 15 would go to retained earnings as on 1 Jan 2017.

Yes, you can adopt IFRS 16 earlier if you adopt IFRS 15, too.

Hi Silvia,

Thanks a lot for your detailed illustration on IFRS 16.

I would like to clarify how should we treat in your example, if we have paid a 100,000 (Altogether 200,000) in advance during the year 2018?

Should we treat 100,000 as an advance payment in year 2018 and allocate it according to the table in 2019?

Or, do we need to adjust the table to reflect the correct present value by adjusting the lease payment in 2018 from 100,000 to 200,000 (so that the liability b/f will be adjusted in year 2019)?

Your guidance on this would be highly appreciated.

What happen if a company’s financial year end is 30 June 2019? Do we just adjust from Jan 2019?

Thanks.

Hi Larry, no. You apply the IFRS 16 in the financial statements for the period that begins AFTER 1 January 2019 – that is, in your case, first time for the period 1 July 2019-30 June 2020. S.

Hi. I can’t find any information online about leases provided for free indefinitely, in exchange for potentially having access to the client base of the company using the premises. Any help would be greatly appreciated. I would have thought that some income must be implied, perhaps at arms length? Many thanks.

Thanks Silvia.

appreciate your kind efforts.

I wonder that How the lessor will recognize.It will similar with financial lease

Hi Tu Tu, the lessor will keep recognizing it as before, because IFRS 16 has not changed much with regard to lessor’s accounting. S.

Hi Silvia, i would like to know how to recognise tenants deposits by both tenant and landlord…thnx

Thank you very much. Found clear and easy to understand as well as very useful.

Thanks its very useful

Thank Silvia, as usual, very clear and easy to understand 🙂

Dear Silvia M. thank you for helping us by doing numerical example on the lease IAS 17 and IFRS 16 for implement.

Dear Silvia M. Could you help us on IAS 36 impairment of asset by doing numerical example on the recoverable amount or if you can, help me by doing numerical example on value in use For Cash Generating Units and single item.

We had as services provider a lot of agreemnets and contratcs in repsect of rent equipment and tools as well as manpower with sub-contractors.

in the same time we had Rent contrcats for offices and land.

so according to that, rent conracts of offices and land will be subject to IFRS 16 as well the manpower conracts.

Thank in advance

the rent contract for building & Land will be subject to IFRS 16 also(ROU) assets.

I’m studying for DipIFR from your post and IFRS Kit as well. Very easy to understand. Thank you very much.

Great, thank you and good luck 🙂

Thank you

Hi, under modified retrospective approach why you reversed previous year leases payments. In my point of view, lease liability/ROU Asset will simply be the PV of outstanding lease payments. Please clarify!

Regards

Ali

Hi Ali,

well, the lease liability IS measured at PV of outstanding lease payments. It might not be clear from the first view, but I will clarify in the article – thank you. As for ROU, you can measure it in 2 ways – yours is one way, I measured it the second way – amount equal to the lease liability, adjusted by the amount of any prepaid or accrued lease payments relating to that lease recognised in the statement of financial position immediately before the date of initial application, because it was easier (I already had all those numbers).

For leases previously classified as operating leases, a lessee that elected the modified retrospective application should apply the requirements of IFRS 16 as follows on the date of initial application:

“Recognize a lease liability → measured at the present value of the remaining lease payments, discounted using the lessee’s incremental borrowing rate.”

In my point of view, ROU Asset and Lease liability to be recognized for 282,861 as of 01-Jan-2019, while using modified approach. This is also called cumulative catch-up approach.

Waiting for your reply!

Regards

Oh, I understand your point. You want to measure the ROU asset in the amount of the lease liability – yes, that’s an option, too. Another option is to measure ROU asset as if IFRS 16 has always been applied – that’s what I used. But it’s a good point and I’ll add it to the article – thank you.

By the way – the lease liability IS measured at the present value of the remaining lease payments 🙂

Thanks, you got my point. ROU asset can be recognized as follows:

Recognize a right-of-use asset* → measured at either (accounting policy choice):

Carrying amount as if IFRS 16 was applied (discount at incremental borrowing rate); or

An amount equal to the lease liability adjusted for prepaid or accrued lease payments in the statement of financial position directly before the date of initial application.

Regards

Dears

based on Modified retrospective approach, and if we used this option measure the ROU assets in the amount of the lease liability at translation date, my question , are there any impact on retained earning,

Regards,,

Yes, I think so in some cases.

Dear Silvia,

Many thanks for your prompt reply, but how is it ( impact in RE), if we calculate the BV for lease and the same amount for ROU assets as at translation date, and how can calculate the impact if i didn’t calculate it from commencement date.

Thanks again,

🙂

OK, so if you have a simple scenario, like your ROU equals exactly to lease liability, then I agree that the impact on retained earnings is zero.

In reality, to be totally precise – your ROU asset can be equal to lease liability PLUS any prepaid or accrued lease payment recognized in the balance sheet immediately before the date of initial application – and that would make an impact on your retained earnings (sorry I was lazy in my previous response!)

Hi Silvia – the usual excellent, informative, well written/explained awesome article !!!

Rasel – Just to quote Silvia’ previous article, re exceptions:

‘There are 2 exceptions from this rule:

1. Lease of assets for less than 12 months (short-term leases), and

2. Lease of assets of a low value (such as computers, furniture etc.).’

She also mentioned the need to separate out the service element in a rented item, and again I quote the previous article:

‘When you lease some assets under operating lease (as called by older IAS 17), in most cases, a lessor provides certain services to you, such as maintenance, repairs, cleaning, etc.

Under older IAS 17, you did not need to think about it too much, because you put all lease payments as some rental expense to your profit or loss.

BUT!!!

Under new IFRS 16, you need to split the rental or lease payments into lease element and non-lease element, because you need to:

• Account for a lease element as for a lease under IFRS 16 (if it meets the criteria in IFRS 16); and

• Account for a service element as before, in most cases as an expense in profit or loss.’

Thanks, Rich.

Thank you RICH

HI Silvia

Thank you in deed for your understandable explanation.

Just 1 question,

Is it right that under IFRS 16 operating lease is no longer exist, there is only finance lease?

Hi Rasel, well, it is true that lessees do not classify leases anymore. All the leases are accounted for in the same way (similarly as finance leases under IAS 17) – but there are some exceptions – please see How to adopt IFRS 16 Leases. Lessors classify leases into operating or finance. S.

Thank you Silvia

I became a fan at your explanation. Our company has appointed auditor for the implementation of IFRS 16 and they couldn’t narrate this as simple as you have done. Great job Sylvia???

Thank you Silvia!

AWESOME……………

Hi Silvia,

Thnak you for yrou great instruction on this topic.

In this connection, would you mind telling us further how to derive the incremental borrowing rate in practical life?

And are both methods, full retrospective and modfied ones, acceptable under the new IFRS?

You could easily use the Capital Asset Pricing Model Formula for this

Very useful – thanks again!

Dear Silvia

Thanks for the wonderful explanation.

One question for you.

Scenario:

Currently there is operating lease for cars and after the end of lease term, cars are purchased directly by the employees from the lessor. No disposal in company financial statement is recorded.

Now, the impact of IFRS 16 will be that cars will be assets of the company and in order to be transferred to employees after the lease period, disposal needs to be recorded in the financial statements.

Query:

Is there any way in IFRS 16 that assets directly transferred to employees without disposal being recorded in the Company financial statements?

Hi Huzaifa,

under IFRS 16, the company will NOT have cars in its financial statements. Not at all. Instead, you will have ROU (right-of-use) asset to these cars in the financial statements. That’s slightly different. So, you will depreciate ROU to zero and then remove it from the financial statements as soon as the lease term is over. You can’t avoid it. Then when employees get the cars and the legal title passes to them from the lessor – it’s none of your business 🙂 S.

Hi Ahmed, please i wouldnt mind if you can share your company employees car policy with me.. I will like to know how the policy works, maybe i can introduce it to my company.. fawemimooladele@gmail.com

Hi,

the interest you calculated is an annual interest, how to record monthly interest. Should i simply divide the interest by 12 or do I need to use monthly effective interest rate?

You cannot divide by 12, it will not work due to compound interest. You need to calculate monthly effective interest rate, or derive it from the annual rate.

Hello Silvia,

Thank you for sharing this important information with us,

kindly i need quick answer for my case.

i am auditor and i have one client have contract for lease land for 28 years and the contract starting from 1 January 2014 and all rent expenses from 2014 to 2019 he capitalize it because he build factory under this land, now if i apply IFRS 16 for this case what i think all rent amount from 2014 to 2019 should go to P&L yes?

if this case applicable in IFRS 16 please i need the correct process for it,

Thanks&Regards,

Only one word – Thanksssssssssssssssssssssssssssssssssssssss

You’re welcome 🙂

Hellow Silvia

Thank you for your atticles….it’s so helpful for begginers in practices…..can we communicate privately?

Thanx in advance