The first thing you need to do before you even start to play with hedge accounting is to determine the TYPE of hedge relationship that you’re dealing with.

Why?

Because: the type of hedge determines your accounting entries. Make no mistake here. If you incorrectly identify the type of the hedge, then your hedge accounting will go totally wrong.

But here’s the thing:

Although all types of hedges are neatly defined in IFRS 9, we all struggle with understanding the differences and distinguishing one type from the other one.

A few weeks ago I was giving a lecture about hedge accounting to the group of auditors. Most of them were audit managers and seniors – so not really freshmen, but experienced and highly qualified people.

Yet after about 5 or 10 minutes of speaking about different types of hedges, one audit manager interrupted me with the question:

“Silvia, I get the definitions. I just don’t get the difference. I mean the real substance of a difference between fair value hedge and cash flow hedge. It looks the same in many cases. Can you shed some light there?”

Of course.

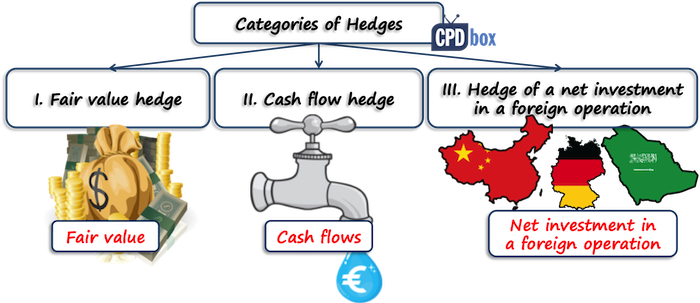

What types of hedges do we have?

Although I clearly explain a hedge accounting in details in my IFRS Kit, let me shortly explain what type of hedges we have:

- Fair Value Hedge;

- Cash Flow Hedge, and

- Hedge of a Net Investment in a Foreign Operation – but we will not deal with this one here, as it’s almost the same mechanics as a cash flow hedge.

First, let’s explain the basics.

What is a Fair Value Hedge?

Fair value hedge is a hedge of the exposure to changes in fair value of a recognized asset or liability or unrecognized firm commitment, or a component of any such item, that is attributable to a particular risk and could affect profit or loss.

That’s the definition in IFRS 9 and IAS 39.

So here, you have some “fixed item” and you’re worried that its value will fluctuate with the market. I’ll come back to this later.

How to Account for a Fair Value Hedge?

OK, let’s not go into details and let’s just assume that your fair value hedge meets all criteria for hedge accounting.

In such a case, you need to make the following steps:

- Step 1:

Determine the fair value of both your hedged item and hedging instrument at the reporting date; - Step 2:

Recognize any change in fair value (gain or loss) on the hedging instrument in profit or loss (in most cases).

You need to do the same in most cases even if you don’t apply the hedge accounting, because you need to measure all derivatives (your hedging instruments) at fair value anyway. - Step 3:

Recognize the hedging gain or loss on the hedged item in its carrying amount.

To sum up the accounting entries for a fair value hedge:

| Description | Debit | Credit |

| Hedging instrument: | ||

| Loss on the hedging instrument | P/L – FV loss on hedging instrument | FP – Financial liabilities from hedging instruments |

| OR | ||

| Gain on the hedging instrument | FP – Financial assets from hedging instruments | P/L – FV gain on hedging instrument |

| Hedged item: | ||

| Gain on the hedged item | FP – Hedged item (e.g. inventories) | P/L – Gain on the hedged item |

| OR | ||

| Loss on the hedged item | P/L – Loss on the hedged item | FP – Hedged item (e.g. inventories) |

Note: P/L = profit or loss, FP = statement of financial position.

What is a Cash Flow Hedge?

Cash flow hedge is a hedge of the exposure to variability in cash flows that is attributable to a particular risk associated with all or a component of a recognized asset or liability or a highly probable forecast transaction, and could affect profit or loss.

Again, that’s the definition in IAS 39 and IFRS 9.

Here, you have some ”variable item” and you’re worried that you might get less money or have to pay more money in the future than now.

Equally, you can have a highly probable forecast transaction that hasn’t been recognized in your accounts yet.

How to Account for a Cash Flow Hedge?

Assuming your cash flow hedge meets all hedge accounting criteria, you’ll need to make the following steps:

- Step 1:

Determine the gain or loss on your hedging instrument and hedge item at the reporting date; - Step 2:

Calculate the effective and ineffective portions of the gain or loss on the hedging instrument; - Step 3:

Recognize the effective portion of the gain or loss on the hedging instrument in other comprehensive income (OCI). This item in OCI will be called “Cash flow hedge reserve” in OCI. - Step 4:

Recognize the ineffective portion of the gain or loss on the hedging instrument in profit or loss. - Step 5:

Deal with a cash flow hedge reserve when necessary. You would do this step basically when the hedged expected future cash flows affect profit or loss, or when a hedged forecast transaction occurs – but let’s not go in details here, as it’s all covered in the IFRS Kit.

To sum up the accounting entries for a cash flow hedge:

| Description | Debit | Credit |

| Loss on the hedging instrument – effective portion | OCI – Cash flow hedge reserve | FP – Financial liabilities from hedging instruments |

| Loss on the hedging instrument – ineffective portion | P/L – Ineffective portion of loss on hedging instrument | FP – Financial liabilities from hedging instruments |

| OR | ||

| Gain on the hedging instrument – effective portion | FP – Financial assets from hedging instruments | OCI – Cash flow hedge reserve |

| Gain on the hedging instrument – ineffective portion | FP – Financial assets from hedging instruments | P/L – Ineffective portion of gain on hedging instrument |

Note: P/L = profit or loss, FP = statement of financial position, OCI = other comprehensive income.

As you can see, you don’t even touch the hedged item here and you only deal with the hedging instrument. So that’s completely different from fair value hedge accounting.

How to Distinguish Fair Value Hedge and Cash Flow Hedge?

What I’m going to explain right now is my own logic of looking at this issue. It’s not covered in any book.

It’s how I look at most hedging transactions and this is a very simplified view. But maybe it opens up your mind to logical thinking about hedges.

Please, ask first:

What kind of item are we hedging?

Basically, you can hedge a fixed item or a variable item.

Hedging a Fixed Item

A fixed item means that the item has a fixed value in your accounts and it may provide or require fixed amount of cash in the future.

The same applies for unrecognized firm commitments that have not been sitting in your accounts yet, but they will be in the future.

And when it comes to hedging fixed items, then you’re practically dealing with the fair value hedge.

Why is that?

Well, here, you are worried, that in the future, you would be paying or receiving a different amount than the market or fair value will be. So you don’t want to FIX the amount, you want to GET or PAY exactly in line with the market.

I’m referring to “GET” or “PAY” only for the sake of simplicity. In fact, you don’t even need to get or pay anything in the future – you’re just worried that the item will have a different carrying amount in your books that its’ fair value.

Fair Value Hedge Example

You issued some bonds with coupon 2% p.a.

It’s nice that you always know how much you’ll pay in the future.

BUT you are worried that in the future, market interest rate will be much lower than 2% and you will be overpaying (in other words, you could get the loan at much lower interest in the future than you will be paying at the fixed rate of 2%).

Therefore, you enter into interest rate swap to receive 2% fixed / pay LIBOR12M + 0.5%. This is a fair value hedge – you tied the fair value of your interest payments to market rates.

Hedging a Variable Item

A variable item means that the expected future cash flows from this item change as a result of certain risk exposure, for example, variable interest rates or foreign currencies.

When it comes to hedging variable items, you’re practically speaking of a cash flow hedge.

Why is that?

Here, you are worried that you will get or pay a different amount of moneyin certain currency in the future that you would get now.

In fact, in a cash flow hedge, you want to FIX the amount of money you’ll get or pay – so that this amount would be the same NOW and IN THE FUTURE.

Cash Flow Hedge Example

You issued some bonds with coupon LIBOR 12M+0.5%.

It means that in the future, you will pay interest in line with the market, because LIBOR reflects the market conditions.

BUT – you don’t want to pay in line with market. You want to know how much you will pay in the future, as you need to make some budget, etc.

Therefore you enter into interest rate swap to receive LIBOR 12 M + 0.5% / pay 2% fixed. This is cash flow hedge – you fixed your cash flows and you will always pay 2%.

To Sum This All Up

Now you can see that the same derivative – interest rate swap – can be a hedging instrument in a cash flow hedge as well as in a fair value hedge.

The key to differentiate is WHAT RISK you hedge. Always ask yourself, why you undertake the hedging instrument.

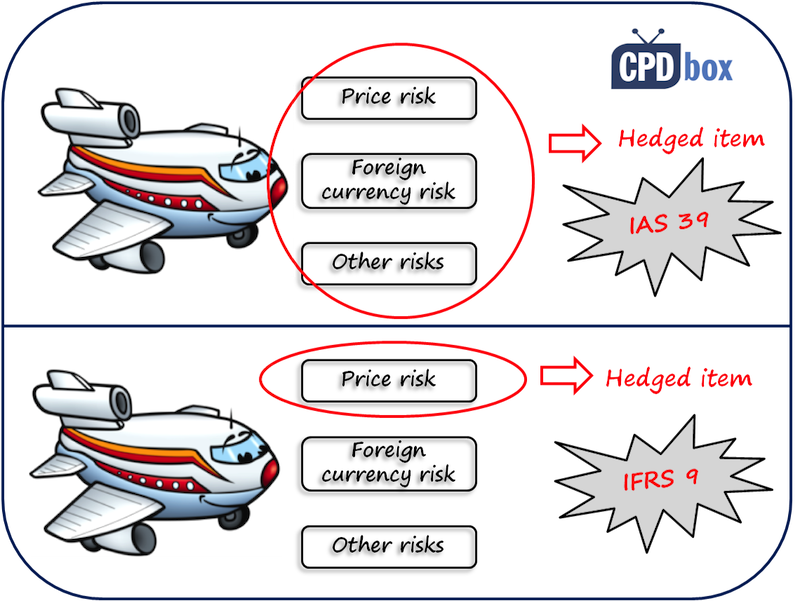

But it’s not that simple as it seems because there are some exceptions in IAS 39 and IFRS 9.

For example, even when you have a fixed item, you can still hedge it under cash flow hedge and protect it against foreign currency risk.

Equally, you can hedge a variable rate debt against fair value changes – and that’s the fair value hedge.

Therefore, please refer to the following table summarizing the types of hedges according to risks and items hedged:

| Item hedged | Risk hedged | Type of hedge |

| Fixed-rate assets and liabilities | Interest rates, Fair value, Termination Options | Fair value hedge |

| Fixed-rate assets and liabilities | Foreign currency, credit risk | Fair value hedge or cash flow hedge |

| Unrecognized firm commitments | Interest rates, Fair value, Credit risk | Fair value hedge |

| Unrecognized firm commitments | Foreign currency | Fair value hedge or cash flow hedge |

| Variable-rate assets and liabilities | Fair value, termination options | Fair value hedge |

| Variable-rate assets and liabilities | Interest rates, foreign currencies, credit risk | Cash flow hedge (most cases) |

| Highly probable forecast transactions | Fair value, interest rates, credit risk, foreign currency | Cash flow hedge |

Now, I’d like to hear from you. Please leave me a comment and let me know whether you have dealt with some hedge accounting in practice, what issues you faced and how you solved them. Thank you!