Example: How to Consolidate

Last update: 01/2025

The video lecture (the written explanations are below the video)

After summaries of standards related to consolidation and group accounts, I’d like to show you how to prepare consolidated financial statements step by step.

I’ll do it on a case study, with explaining what I do and why. If you don’t like reading, you can skip to the end of this article and watch my video.

If you’d like to revise a theory first, then please read my summary of IFRS 3 Business Combinations and IFRS 10 Consolidated Financial Statements, both of them contain video in the end.

What’s the situation?

Here’s the question:

Mommy Corp purchased 80% shares of Baby Ltd. a few years ago.

Below there are statements of financial positions of both Mommy and Baby at 31 December 20X4.

Prepare consolidated statement of financial position of Mommy Group as at 31 December 20X4. Measure NCI at its proportionate share of Baby’s net assets. All retained earnings of Baby are post-acquisition.

Please note here that in the above statements of financial position, all assets are with “+” and all liabilities are with “-“. I use it this way because for me it’s easier to verify and identify mistakes, but it’s up to you.

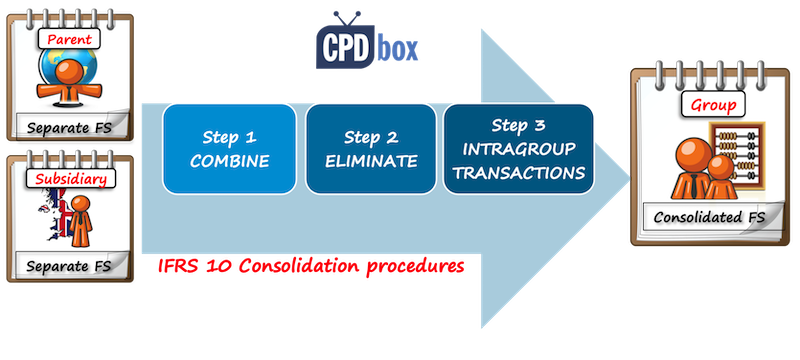

3 Steps in Consolidation Procedures

I have described the consolidation procedures and their 3-step process in my previous article with the summary of IFRS 10 Consolidated financial statements, but let me repeat it here and follow these steps:

- Combine like items of assets, liabilities, equity, income, expenses and cash flows of the parent with those of its subsidiaries;

- Offset (eliminate):

- the carrying amount of the parent’s investment in each subsidiary; and

- the parent’s portion of equity of each subsidiary;

- Eliminate in full intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between entities of the group.

Step 1: Combine

After you make sure that all subsidiary’s assets and liabilities are stated at fair values and all the other conditions are met, you can combine, or add up like items.

It’s very easy when a parent (Mommy) and a subsidiary (Baby) use the same format of the statement of financial position – you just add Mommy’s PPE and Baby’s PPE, Mommy’s cash and Baby’s cash balance, etc.

In reality, companies use their own format for presenting their financial position and therefore it can be difficult to combine. That’s exactly WHY so many groups use their “consolidation packages” and subsidiaries’ accountants must fill them up along with preparing own financial statements.

Therefore, when a group controller calls you every five minutes to remind you the consolidation package, you’ll know why!

In our case study, combined numbers looks as follows:

Of course, there are some strange and redundant numbers, for example both Mommy’s and Baby’s share capital, but we haven’t finished yet!

Step 2: Eliminate

After combining like items, we need to offset (eliminate):

- the carrying amount of the parent’s investment in each subsidiary; and

- the parent’s portion of equity of each subsidiary;

and of course, recognize any non-controlling interest and goodwill.

So let’s proceed. The first two items are easy – just remove Mommy’s investment into Baby (CU – 70 000), and remove Baby’s share capital in full (CU + 80 000).

As there is some non-controlling interest of 20% (please see below), you need to remove its share in Baby’s post-acquisition retained earnings of CU 9 000 (20%*CU 45 000).

Wait a second – how do we know that all Baby’s reserves (retained earnings) of CU 45 000 are post-acquisition?

Well, the question says that the full Baby’s retained earnings are post-acquisition, otherwise you need to trace it.

Be careful here, because you absolutely need to differentiate pre-acquisition retained earnings from post-acquisition retained earnings, but here, we’re not going to complicate the things.

Then we need to recognize any non-controlling interest and goodwill.

Non-controlling interest at 31 December 20X4

Mommy has owned 80% of Baby’s share and therefore, non-controlling interest owns remaining 20% of Baby’s net assets.

The question asks to measure non-controlling interest at proportionate share on Baby’s net assets, so here’s how it looks like at the end of the reporting period:

Baby’s net assets are CU 125 000 as at 31 December 20X4, including Baby’s share capital of CU 80 000 and Baby’s post-acquisition reserves of CU 45 000.

Non-controlling interest at 31 December 20X4 is 20% of Baby’s net assets of CU 125 000, which is CU 25 000. Recognize it with minus, as we are crediting equity with non-controlling interest.

Initial recognition of goodwill

There might be some goodwill arisen on initial recognition. If you’d like to learn more about goodwill, please refer to the article about IFRS 3 Business Combinations.

Let’s calculate it. Please don’t forget that we calculate goodwill based on numbers on acquisition, not on 31 December 20X4.

The goodwill is calculated as:

- Fair value of consideration transferred: in this case, we simply take Mommy’s investment in Baby of CU 70 000;

- Add any non-controlling interest at acquisition: here, we’re not adding the non-controlling interest calculated above, as it’s the measurement on 31 December 20X4. At acquisition, the value of non-controlling interest is 20% of Baby’s net assets on its incorporation of CU 80 000 (share capital only). It equals CU 16 000.

- When a business combination was achieved in stages, you would need to add the acquisition-date fair value of the acquirer’s previously-held equity interest in the acquiree, but in this example, it’s not applicable,

- Deduct Baby’s net assets at acquisition: CU – 80 000.

Goodwill acquired in a business combination comes to CU 6 000 (70 000 + 16 000 – 80 000).

The elimination entry looks as follows (sign “+” indicates a debit entry; sign “-“ indicates a credit entry):

| Description | Amount | Debit | Credit |

| Remove Mommy’s investment in Baby | -70 000 | FP – Investment in Baby | |

| Remove Baby’s share capital in full | +80 000 | FP – Baby’s share capital | |

| Remove 20% (NCI) of Baby’s post-acquisition retained earnings | +9 000 | FP – Retained earnings | |

| Recognize non-controlling interest on 31 December 20X4 | -25 000 | FP – Non-controlling interest | |

| Recognize goodwill acquired in a business combination | +6 000 | FP – Intangible assets (goodwill) | |

| Check | 0 |

I have transferred this journal entry into our consolidation worksheet and it looks as follows:

Eliminate Intragroup Transactions

Parents and subsidiaries trade with each other very often.

However, when you look at both parent and subsidiary as at 1 company, which is the purpose of consolidation, then you find out that there’s no transaction at all.

In other words, group has not performed any transaction from the view of some external user.

Therefore you need to eliminate all transactions happening within the group, between a parent and its subsidiaries.

Looking to above individual statements of financial position of Mommy and Baby you see that Mommy has a receivable to Baby of CU 8 000 and Baby has a payable to Mommy of CU 8 000. Perhaps these 2 items relate to the same transaction between them and we need to eliminate them, by debiting payables and crediting receivables:

Final steps

After we have completed all steps or consolidation procedures, we can add up all the combined numbers with our adjustments and thus we arrive at consolidated statement of financial position.

You can revise all the steps and formulas in Excel file that you can download at the end of this article.

Here’s how it looks like:

Please note the following facts:

- Consolidated numbers are simply sum of Mommy’s balance, Baby’s balance and all adjustments or entries (Steps 1-3).

- Mommy’s investment in Baby’s shares is 0 as we eliminated it in the step 2. The same applies for Baby’s share capital and consolidated statement of financial position shows only a share capital of Mommy (parent).

- There’s a goodwill of CU 6 000 and non-controlling interest of CU 25 000, as we have calculated above.

- Consolidated retained earnings are CU 98 000 and they consist of:

- Mommy’s retained earnings of CU 62 000 in full, and

- Mommy’s share (80%) on Baby’s post-acquisition retained earnings of CU 45 000, that is CU 36 000

Exam-style consolidation

I know that many of you prepare for your exams and this is NOT the way how you learned consolidation during exam preparation courses.

OK, I understand.

I prefer this way of making consolidation by far, because here, you go systematically, step by step. You can deal with each adjustment in a separate column and as a result, your numbers will always balance. You will never forget anything.

The “exam-style” of making consolidated financial statements is good and easy when there are just a few issues or complications.

But when you need to deal with more complex situations, then you can forget or omit the things very easily. Trust me, I did it too.

However, to make you happy, you can find the same case study solved “by the exam-style” in the attached excel file that you can download in the end of this article.

Is consolidation really easy?

Sometimes.

But in most cases, there is lots of issues or circumstances that you need to take into account and exactly their significance and amount makes it all difficult.

What issues? For example:

- Consideration transferred for acquiring the shares may involve not only cash, but also some other forms, such as share issue, contingent consideration, transfers of assets, etc.

- Non-controlling interest can be measured at fair value instead of at proportionate share.

- There might be some unrealized profit on transactions within the group and it needs to be eliminated.

- There might be some transfer of property, plant and equipment at profit within the group and as a result, you need to adjust both unrealized profit and depreciation charge, too.

- Goodwill might be either positive or negative (=gain on a bargain purchase). Moreover, it can be impaired.

- Subsidiary’s net assets might be stated in the amounts different from their fair value, or even not recognized at all.

- Subsidiary may show both pre-acquisition retained earnings and post-acquisition retained earnings. You need to be extremely careful in differentiating them and dealing with them separately.

I can go on and on, but I don’t want to discourage you. However, if you need to know more about all these issues, I have covered them fully in my premium learning package the IFRS Kit, so please check out if interested.

Further reading: Here’s the list of all articles and videos published on CPDbox on consolidation – totally free.

If you like this example and explanations, please help me spread a word about it and share it with your friends. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

250 Comments

Leave a Reply

Thank you so much this was so helpful

Hi silvia,

I have 6 companies to consol with mixture of different currencies. But for consol report, it is fix at USD. I hv 2 co. with RM and GBP currencies. So on consol level, when i did at USD, my consol balance sheet s forex reserve due to translation. However, i couldnt get to balance the BS at consol level. I suspect due to RM co. with have non-controlling interest (share capital & share premium), do i need to any adjustment?

many thanks in advance

Can any body help me in these two questions. Got staked here. Help

1. Will we have to eliminate the parent entity’s investment in the subsidiaries each year as part of our consolidation entries or will we have to do the elimination only in the first year following acquisition but not there after? Why?

2. While there is a general requirement that all the parent entries must consolidate the financial statements of subsidiary over which they have the capacity to control, there is an exception for “investment entities”. What is the basis of this exception and do you think it is a justifiable exception?

Hi Cilas,

1. You have to do it all the time, not only the first time – you need to repeat this entry. The reason is that there is no investment in a subsidiary from the group’s point of view all the time, not only right after acquisition.

2. The reason is that the main business of the investment entities is to earn money on dividends or movements in the share prices on the market and NOT to exercise control over subsidiary. From this perspective it has more sense to see the fair value of all investments held by the investment entity, rather than see the aggregated assets and liabilities. So yes, I think it’s a justifiable exception. S.

Thanks. Very well presented.

I was looking for such an explanation with numerical example.

Regards

KS

HI I WOULD LIKE TO KNOW HOW THE INTER COMPANY DIVIDEND IS TREATED AND WHEN THE PARENT COMPANY HAS 50% IN THE SUBSIDIARY HOW CAM BE TREATED IS IT THE SAME AS 80% THANKS

if we need to pass eliminating entry for revenue and cost of goods sold then how to eliminate profit in that transaction. example: revenue is 12 and COGS is 10 then whether needs to eliminate 12 from voth side and adjust 2 in profit or elimate 10 from both side and eliminate 2 in profit. thanks for the article.

And for the Consolidated P/L Statement how is calculated the NCI for Profit of the year (at year end)if parent has the 80% of subisdiary?

Regards,

I have an inquiry. Why the Non-Controlling Interest is calculated at the year end and Goodwill is calculated at the date of acquisition? Thank you.

Yes, basically. Goodwill is calculated just once upon acquisition and then it’s tested for impairment subsequently. If there’s no impairment, your goodwill is the same as at acquisition.

For NCI, you need to calculated it at acquisition, but also update it at the end of every reporting period. S.

hii

If subsidiary co. issue bonus shares how will be the adjustments ?

Hi Silivia,

In some cases parent company and subsidiaries use different financial statement formats to prepare their separate financial statements.

Example;In a group,

Parent company is Manufacturing company.

one of subsidiary is bank.

here parent company format is different form subsidiary company.

which format should we use in consolidated financial statements.

Thank you.

Dear Dinesh,

IFRS do not prescribe the exact format of the financial statements and an entity (including group) should select the format it fits them the best, while keeping the minimum requirements. Therefore, you would select the format of the business prevalent in the group. S.

Hi Silvia, would like to ask how to prepare eliminating entries in consolidating subsidiaries (partially owned) with capital deficiency? Is it proper to recognize NCI with a debit balance? Kindly give me any reference for my basis. Thank you for your inputs.

Hi Silvia, this is a very nice article. Can you please let me know the following:

Where do we record/recognised the impairment of Goodwill i.e. if the goodwill is impaired, then the expense/impairment will be recognised in the parent company FS or consolidated FS?

Thank u and Regards,

Dear Talha, thank you for your kind words. The impairment of goodwill is always recognized at a consolidated level, because in parent’s financial statements, there is no goodwill and the investment in a subsidiary is shown only in 1 line 🙂 S.

🙁

Sorry, John, terribly busy. Please be patient.

Sorry to sound in a hurry. No worries, Thanks a lot for your time and your website!

Perfect way to explain. God bless you.

Hi Silvia,

How to Compute “Goodwill” and “Non controlling interest” in a scenario like Company A has 60% shares in Company B and Company B has 70% shares in Company C. And Can you explain through an Example problem

Hi Sivia,

I want to learn more about consolidation process, but I don’t want to buy the whole IFRS Kit. do you sell only the consolidation part?

Thanks

Hi Lewis,

no, sorry, just the full IFRS Kit. S.

Hi Silvia,

While Computing Goodwill Calculation in first time acquisition of control, at what value we have to consider the existing investment shares in subsidiary ( Existing investment are 25% shares acquired at 2000 and carrying value is 2500 ). We don,t know the fair value of shares.can we consider the carrying value of investment?

Please replay me, Thank you very much.

How impairment is done, if here is positive goodwill, negative goodwill or No goodwill in the books of Investor (parent)

Ram,

I can’t respond to these questions in a comment, as it would take me too long. It’s all well explained in the IFRS Kit. Best, S.

Great article.

can I ask what CU stands for?

Thank you! CU = currency unit 🙂

please i need to know the process to deconsolidate? , how do you treat the equity and what journal entries to does it needs to make the deconsolidation? thanks

Hi Franklin,

great topic for the next article. I’ll cover that. But not here in the comments 🙂 S.

Hi Silvia,

Nice article, thanks for sharing

Did you write that deconsolidation article yet? I would be interested.

Thanks

I am also interested

Mustafa, if you look carefully to the IFRS Kit, you will find deconsolidation excel file under Consolidation/Group accounts.

Thank You !

well understood Silvia. wish you are my teacher.

Great article! Thanks for posting.

Dear,

What if am doing consolidation for different legal entities inside one country and I want to report to the ultimatum share holder one financial Statement

That’s possible, but I’m not sure what the question is. Can you please specify? S.

Dear Silvia,

Thank you very much for your in-depth explanation.

May I have a question regarding the initial recognition of goodwill. Do we have to recognize the good will at the acquisition date? I mean when the Mommy Corp. purchased 80% of Baby Ltd. at $70,000, we already have to make the following entries in the Mommy Corp. journal:

Debit Investment in Baby Lts. 64,000

Good will 6,000

Credit Cash 70,000

Or we just recognize the goodwill at the first consolidated report?

Dear Nam,

goodwill arises on acquisition, so if you are making any report on acquisition date, then yes, you have to recognize it. S.

Hi Silvia,

Thanks for the explanation and the steps I have a doubt:

The share of NCI already includes the portion of retained earnings so is it necessary to shave off the 20% share of noncontrolling interest from retained earning .Doesn’t it amount to doubling.

Jimmi,

it’s not double counting, because you are deducting from retained earnings and adding to NCI. S.

Dear Silvia

May I check with you inter-company balance differences due to exchange difference should go to profit & loss or translation reserve?

Thanks with regards

Gary Liew

Very simple and nice explanation.

Thank you 🙂

You ve really done a great job. Can you pls teach piecemeal acquisition? Kind regards

excellent explanation.

If it’s impaired, would it be common to see an adjustment to the balance sheet impairment?

Excellent

Hi Silvia,

could you please explain why there is a goodwill if the subsidiary was incorporated by the parent? I would expect goodwill calculation just for acquired companies.

Thanks in advance for clarification. S.

Hi Sandra,

sure, you’re right, but the example says “has owned since incorporation” – maybe parent bought it 🙂 OK, I brought this example due to pure simplicity of explanation and in reality, when someone incorporates subsidiary, there should not be any goodwill, of course. S.

good explanation

Hi,

Wrt. Consolidation of financial statements, what will be the accounting and reporting treatment when one co.has power to control but doesnot have any investment in other co.?

Hi Rahul,

the accounting technique is the same as for any other business combination with control, however here, you would have a really large non-controlling interest. S.

Great job.

Dear Mrs Silvia, thank you for the help, I am sitting tomorrow p2 for second time, I am confused with complex groups, if you can please give me your lights on the following issue:

A has a 60% over a subsidiary B, B has an investment of 25% of C, and A has a direct control over C of 30%.

In the solution of this question the A has C as a sub-subsidiary but how this could be. as the effective interest is (60%*25%)+30%=45% this rates indicates that its an associate and not subsidiary. I know may be too late for such example but I am really confused with complex groups and its logic.

Good JOB

Thanks alot, i was interviewed last week and asked about consolidation of accounts, i surely did not know about it, but now i can answer such a question through what i have learnt from your example, thanks so much

Is there an example to show what would happen in year 2 of this consolidation?

Dear Siddhart, here, I post basic examples. More complex one, like subsequent years, are solved in my IFRS Kit (http://www.cpdbox.com/ifrs-kit)

Hi,

Have a question on NCI

As Post acquisition profit – CU 9000 is eliminated

Again 25% of 125000 is eliminated – which contains retained earnings of 45000. Is it not doing it double?

Can you help me in understanding it right?

Silivia, You really making consolidation simple! Kudos to you!!

Thanks.

Sri

Hi Sri,

thank you!

Here, you need to distinguish between WHAT IS ELIMINATED and WHAT IS NEWLY RECOGNIZED:

– 9000 is just NCI’ share on post-acquisition profit – this is eliminated

– 25% of 125 000 is the full load of NCI at 31 Dec 20X4 – it is NOT eliminated, it is NEWLY RECOGNIZED, just look to the final consolidated B/S. In fact, you are transferring part retained earnings to NCI, part to goodwill (pre-acquisition) and part remains within equity (80% of post-acquisition).

Hope it’s a bit clearer.

Hi Silvia, if the subsidiary that you are consolidatingissues additional share capital and you share increase from ex. 60 to %75. How do we account for theis and does it have an effect on the P/l of the consolidated financials.

Thank you

I love the simplicity and the animation

Most slides I see online are complicated, wordy and full of techy jargon that puts many readers off.

Hi Silivia

Thanks

It is really nice. Do you have something similar for the consolidation of Statement of Comprehensive Income and Income

Statement ?

another great work Silvia; Keep up!

Great work, thanks

non-controling interest =

net assest*20%= (147-22)*20%=25.000

goodwil = 70.000+25.000-125.000=-30.0

Levon, you have calculated NCI on the reporting date 31 December 20X4 – that’s correct, it’s 25 000.

But please, be very careful at calculation of goodwill. Here, you should not add NCI at the reporting date, but ON THE ACQUISITION date, as you’re recognizing goodwill on the acquisition date.

Therefore, you should not add 25000, just 16000, as Baby’s net assets on acquisition were just 80 000 (share capital only, as all retained earnings are post-acquisition).

Hope it’s clearer now. S.

NCI at 31.12.20×4 = 80.0*20% + 45.0*20=16.0 + 9 =25.0,

is it right?

Yes, that’s correct. It’s the another way of calculating it. Although I prefer taking NCI on acquisition plus NCI’s share on post-acquisition reserves – but that’s up to you. S.

yes that’s good

If i invest in only one subsidiary in 2015 that require me to consolidate, what will be the comparative figure? Will it need to be consolidated as well?

Dear Glesie,

no, you do NOT consolidate comparatives. The reason is that in the previous period, there was no subsidiary and therefore, there’s nothing to consolidate. You start consolidating only from the current reporting period.

Hope this helps

Silvia

Dear Silvia can you please give me email address so i can ask u few question in regards my assignments.

Thanks

Thanks a lot Sylvia, these are very helpful. God bless you

Simple and straightforward explanations. I love the animations too. I find it much easier to remember the steps using the animation. Please keep up the wonderful work.

Great work Silvia!. Thanks a lot.

Excellent way of presenting , thanks

Has simplified a huge reading.

Thanks very much.