{kind=link}

How to account for intercompany loans under IFRS

How to account for intercompany loans under IFRS when there is no documentation, loans are not at commercial terms or there is no fixed repayment date? Learn here!

{kind=link}

Accounting for Deemed Disposal of Associate (IAS 28)

Sometimes, the things can happen behind your back – without you even noticing. And, these things can affect you somehow. Let me tell you a short story. I participated in an audit of a big insurance company and our senior asked me to look at…

{kind=link}

How to Make Consolidated Statement of Cash Flows with Foreign Currencies

Did you know that many groups prepare their consolidated cash flow statement completely incorrectly? And, if you are well-experienced accountant, you can actually spot the faulty numbers instantly when you look to the statement of cash flows. Sadly, this wrong method is often taught in…

{kind=link}

How to Test Goodwill for Impairment

When a company acquires control over another company, then often a goodwill arises, too. You should present it as an intangible asset, but when you think about it carefully, a goodwill is not a typical asset, because unlike other assets, you cannot sell it to…

{kind=link}

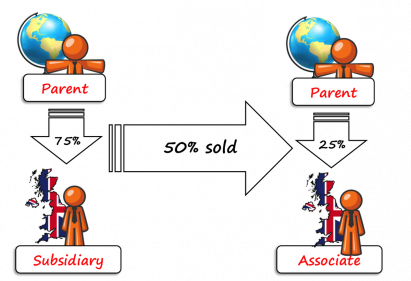

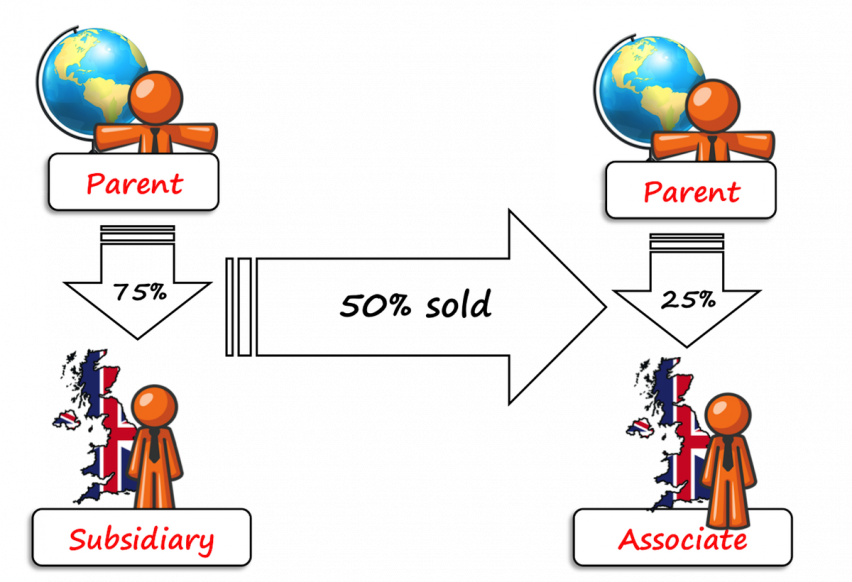

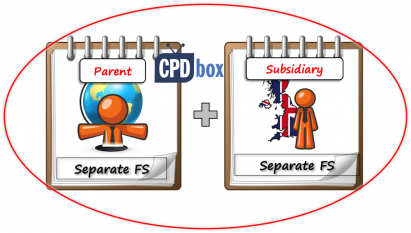

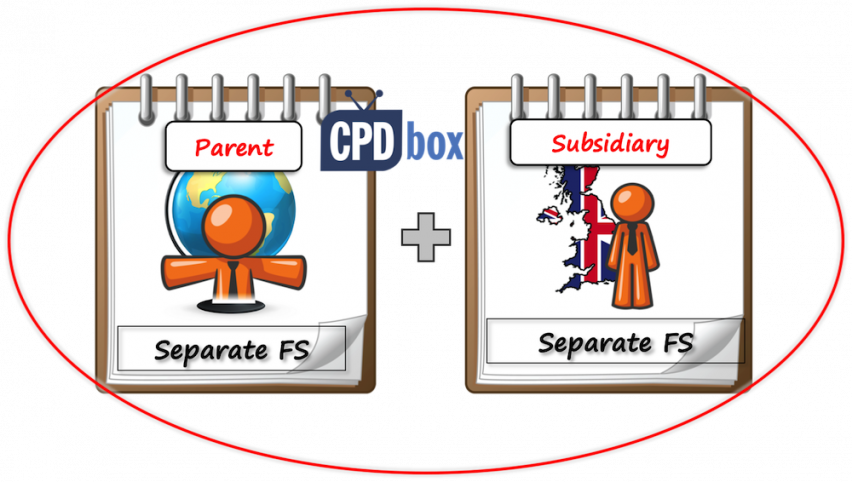

How The Groups Change

Group accounts are a very popular topic and yes, I can understand it as it’s a main topic for many accounting exams. I have written a few articles about it, including: Intro to group accounts and consolidation; Example: How to consolidate; and a few summaries…

{kind=link}

Top 5 IFRS Changes Adopted in 2014

The year 2014 brought us some very significant changes in IFRS. While some changes might not give you a hard time to adopt, the other changes can cost you a lot of money and time to make them effective in your company. The year 2014…

{kind=link}

IFRS 11 Joint Arrangements

Joint venture or joint operation? What is joint control? How to account for joint arrangements? In our consolidation series, we have already covered investments in subsidiaries (IFRS 3 and IFRS 10), associates (IAS 28) and other financial instruments. Today, we’ll take a look at the…

{kind=link}

IAS 28 Investments in Associates and Joint Ventures

Let’s focus on associates, joint ventures, significant influence and equity method today. You have already learned various aspects of having control over some investment: how to identify it, how to account for it and we also learned basic consolidation procedures step by step. It was…

{kind=link}

Example: How to Consolidate

Updated in 2025: Step-by-step solved example of consolidation under IFRS 10 with video. You will learn exactly WHAT you are doing and WHY you are doing this. If you apply this systematic method, your balance sheet will always BALANCE with no errors.

{kind=link}

IFRS 3 Business Combinations

When should you apply IFRS 3 and when IFRS 10? What is the difference between IFRS 3 Business Combinations and IFRS 10 Consolidated Financial Statements? Today, I’d like to continue our “consolidation” series and after the introductory lesson and the summary of IFRS 10, let’s…