Should you capitalize or not?

When it comes to determining the cost of your assets, most standards ask to include all directly attributable items.

What about interest and other borrowing costs?

Did you know that if you have 10 dollars in your pocket and no debt, then you are wealthier than 25% of all Americans? Trust me – the corporate scene is no different!

Well, let’s be honest, borrowing money does carry a cost, and sometimes very significant one.

Here, I’m not talking about the loss of your friends or even family members, but all these quantifiable items such as interest and similar cost.

As these are often directly attributable to the acquisition of assets, they should be capitalized.

Some time ago, the standard IAS 23 Borrowing Costs gave you a choice:

- Either you could put all your borrowing costs directly in profit or loss and thus you did not have to worry about capitalizing them, or

- You could capitalize eligible borrowing costs.

Unfortunately, this choice was removed a few years ago for most of assets, and now you have to capitalize.

How?

In this article, I tried to draft a few basic rules about capitalizing borrowing costs and also, I reply to 3 most common questions received from you.

Let’s dive in.

Let’s talk basics: What does IAS 23 Borrowing Costs say?

The core principle of IAS 23 Borrowing Costs is that you should capitalize borrowing costs if they are directly attributable to the acquisition, construction or production of a qualifying asset.

Other borrowing costs are expensed in profit or loss.

Here, let me clarify 3 essential issues:

What are qualifying assets?

Qualifying assets are assets that take a substantial period of time to get ready for their intended use or sale.

Note here that IAS 23 does not say it must necessarily be an item of a property, plant and equipment under IAS 16. It can also include some inventories or intangibles, too!

But what is a “substantial period of time”?

Well, that’s not defined in IAS 23, so here you need to apply some judgment. Normally, if an asset takes more than 1 year to be ready, then it would be qualifying.

What can we capitalize?

IAS 23 specifically mentions 3 types of borrowing costs that can be capitalized:

- Interest expenses (refer to the effective interest method under IFRS 9/IAS 39);

- Finance charges on leases under IFRS 16 Leases; and

- Exchange differences on borrowings in foreign currencies, but only those representing the adjustment to interest costs.

However, IAS 23 is pretty silent on some types of expenses and there are doubts whether they are borrowing costs or not, for example:

- Interest cost on derivatives used to manage interest rate risk on borrowings;

- Dividends payable on preference shares (or other types of shares classified as liabilities);

- Gains or losses arising from early repayment of borrowings, etc.

Here again, we need to apply our knowledge from other IFRS standards and sometimes, make a judgment, too.

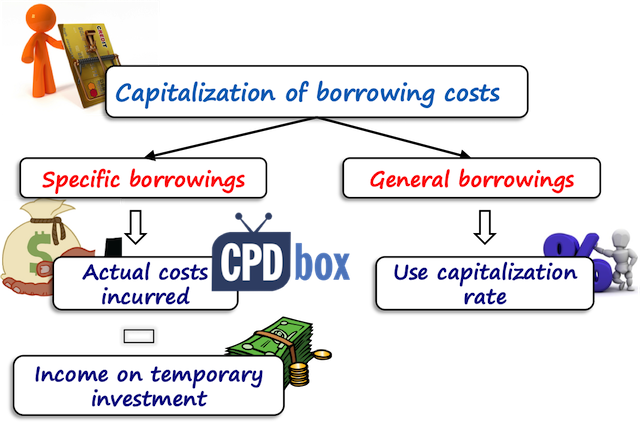

How do you capitalize?

IAS 23 differentiates between capitalizing borrowing costs on general borrowings and specific borrowings.

Specific borrowings

If you borrowed some funds specifically for the acquisition of a qualifying asset, then the capitalization is easy:

You simply capitalize the actual costs incurred less any income earned on the temporary investment of such borrowings.

Let me give you a short example:

Question:

On 1st May 20X1, DEF took a loan of CU 1 000 000 from a bank at the annual interest rate of 5%. The purpose of this loan was to finance a construction of a production hall.

The construction started on 1 June 20X1. DEF temporarily invested CU 800 000 borrowed money during the months of June and July 20X1 at the rate of 2% p.a.

What borrowing cost can be capitalized in 20X1? (Assume all interest was paid).

Answer:

Although the funds were withdrawn on 1st May, the capitalization can start only on 1st June 20X1 when all criteria were met (the construction had not started until 1st June).

Calculation:

- Interest expense: CU 1 000 000 x 5% x 7/12 = CU 29 167

Note: this is very simplified calculation and if the loan is repayable in installments, then you need to take the real interest incurred (by the effective interest method). - Less investment income: CU 800 000 x 2% x 2/12 = CU 2 667

- Total borrowing cost to capitalize in 20X1: CU 26 500

Just don’t forget that the borrowing cost in May 20X1 is expensed in profit or loss, as the capitalization criteria were not met in that period.

General borrowings

Now, there’s more trouble with capitalizing general borrowings, as you need to prepare a bit more calculations.

General borrowings are those funds that are obtained for various purposes and they are used (apart from these other purposes) also for the acquisition of a qualifying asset.

In this case, you need to apply so-called capitalization rate to the borrowing funds on that asset, calculated as the weighted average of the borrowing costs applicable to general pool.

To illustrate it, let me give you an example about capitalizing borrowing costs on general borrowings.

Question:

KLM had the following loans in place at the beginning and end of 20X1:

| Description | 1 January 20X1 | 31 December 20X1 |

| Bank loan, 6% p.a. | 0 | 200 000 |

| Bank loan, 8% p.a. | 130 000 | 130 000 |

| Debenture stock, 5.5% p.a. | 50 000 | 50 000 |

The bank loan at 6% p.a. was taken in July 20X1 to finance the construction of a new production hall (construction began on 1 March 20X1).

The bank loan at 8% p.a. and debenture stock were taken for no specific purpose and KLM used them to finance general spending and the construction of a new machinery.

KLM used CU 60 000 for the construction of the machinery on 1 February 20X1 and CU 25 000 on 1 September 20X1.

What borrowing cost should be capitalized for the new machinery?

Answer:

You ignore bank loan at 6% p.a., because it is a specific borrowing for another asset.

Only general borrowings relate to the financing of the new machinery and therefore, we need to calculate the capitalization rate:

- Weighted average rate = (8% x 130 000 /(130 000+50 000)) + (5.5% x 50 000/(130 000+50 000)) = 5.78%+ 1.53% = 7.31%

- Borrowing costs for the new machinery in 20X1 = CU 60 000 x 7.31% x 11/12 + CU 25 000 x 7.31% x 4/12 = CU 4 021 + CU 609 = CU 4 630.

The hottest questions in capitalizing borrowing cost

After we know the basics, let me give you my opinion on 3 the most common and often questions I get in relation to capitalizing borrowing cost.

I receive these questions quite often, so let me shed some light there.

Question #1: Can you capitalize interest cost in the cost of inventories?

It depends.

In most cases, inventories do not take a substantial period to get ready and in this case no, you cannot capitalize.

But here, there are some examples of inventories that can take a substantial period to complete:

- Wine, cheese or whiskey that matures in bottle or cask for a long period of time;

- Large items of equipment, such as aircraft, ships etc.

In this case, you can capitalize borrowing cost, but it’s up to you if you will or won’t.

While you have no choice for PPE (you have to capitalize), you have a choice for inventories: either you capitalize, or expense in profit or loss.

Question #2: Can you capitalize foreign exchange loss on specifically borrowed money in a foreign currency?

No, you cannot do it fully.

Yes, IAS 23 says that exchange differences on foreign currency borrowings are a borrowing cost to the extent that they are regarded as an adjustment of interest cost.

Simply speaking – you can capitalize the difference between the interest on the foreign currency loan and the hypothetical interest expense in your own (functional currency), because that’s regarded as borrowing cost.

The rest must be expensed in profit or loss.

Question #3: Can you capitalize interest cost on intercompany loan for qualifying assets?

Yes, in the separate financial statements of the borrowing company.

However, be a bit careful about the consolidated financial statements, because based on the intercompany relationship (subsidiary or associate?), the intercompany loan might be eliminated.

Also, let me point out one more issue in relation to intercompany loans: often, they are provided interest-free.

Under IFRS 9, you should recognize almost all financial instruments at their fair value (sometimes plus transaction cost) and if a subsidiary gets an interest-free loan from a parent, it’s nominal amount is not at fair value.

Therefore, a subsidiary needs to set the fair value of the loan received using the market interest rates and book the difference between the loan’s fair value and the cash received in profit or loss (based on the substance of a transaction).

Then, interest expense calculated by the effective interest method is capitalized.

I know, this might sound odd: the loan is interest-free, but you still need to capitalize some borrowing cost on it. Careful!

Do you face any other issues with the borrowing cost? Please leave a comment below and share this article with your friends. Thanks!