Last update: 2023

Transactions in foreign currencies are sometimes a nightmare.

Obviously, we are trading with each other, our own currencies are different and foreign exchange rates are jumping up and down constantly.

We are all aware of basic rules with regard to selection of appropriate exchange rate to apply.

If you would like to refresh a bit, please check out our free materials about IAS 21 and foreign currencies here.

When it comes to more complicated transactions, then it’s hard to apply the rules. Often, I receive one and the same question:

“Dear Silvia, we entered a contract for production and delivery of a machine specific to our business and we paid the first down-payment in a foreign currency.

What is the correct accounting for prepayments in foreign currency under IFRS? How do IFRS treat the effect of moving exchange rates?”

Let me tell you that here, it’s not all black or white.

It depends on more factors, especially the nature of a specific prepayment.

Let me explain why and how. And let me illustrate 2 different scenarios in the examples.

What do the rules say?

Standard IAS 21 The Effects of Changes in Foreign Exchange Rates prescribes how to convert amounts to another currency in 2 cases:

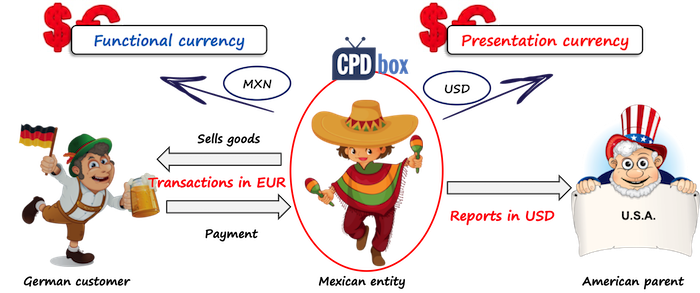

- How to translate How to translate foreign currency amounts to your functional currency;

- How to translate a foreign operation’s financial statements to presentation currency.

When you record your transactions in a foreign currency during the year, then you are translating the foreign currency amounts to your functional currency.

The standard IAS 21 prescribes:

- Initially, you should re-calculate all foreign currency amounts to your functional currency at the spot exchange rate valid at the date of transaction;

- Subsequently (that is – after initial recognition), at each closing or the reporting date, you should re-calculate:

- All monetary items in foreign currency using closing exchange rate at the reporting date;

- All non-monetary items in foreign currency carried at historical cost using the historical exchange rate (at the date of transaction);

- All non-monetary items in foreign currency carried at fair value using exchange rate at the date when fair value was determined.

To clarify the issue with prepayments, IASB issued IFRIC 22 Foreign Currency Transactions and Advance Considerations in 2016 which basically confirms that the date of the transaction, for the purpose of determining the exchange rate, is the date of initial recognition of the non-monetary prepayment asset or deferred income liability.

Now, Let’s break it down.

There are 2 crucial aspects to assess:

- Date of transaction;

- The nature of prepayment.

1. Date of transaction

It’s all crystal clear that initially, you should use the spot exchange rate at the date of transaction for the translation.

But here – what is the date of transaction?

It is the date on which the transaction first qualifies for recognition in accordance with IFRS.

Of course, it can be different for various items, for example:

- For financial liabilities: when an entity becomes a party to a contractual provisions of a contract;

- For property, plant and equipment: when it’s probable that the future economic benefits from the asset will flow to the entity and the cost is reliably measurable.

Although this sounds quite straightforward, some difficulties may arise in determining the transaction date.

For example – you receive goods in day 1, invoice for these goods in day 3 and you pay for these goods in day 4 – what is the date of transaction here? What currency rate shall be applied – day 1, 3 or 4?

We’ll cover this in our example, just go on reading.

2. The nature of prepayment

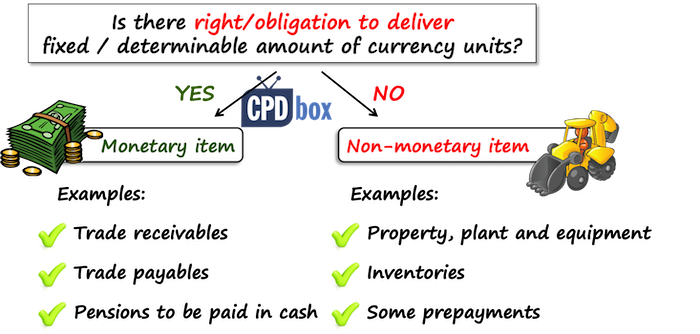

With regard to subsequent translation at the closing rate, IAS 21 makes a difference between monetary items and non-monetary items:

- Monetary items are translated using closing exchange rate;

- Non-monetary items are NOT re-translated, but kept at the original or historical rate.

Is the prepayment for your fixed asset monetary or non-monetary? Well, it can be either monetary, or non-monetary!

There is one thing that makes a difference:

A right to receive or obligation to deliver a fixed or determinable number of units of currency.

Prepayments as such may or may not carry this feature and you should assess each prepayment individually and carefully.

Read the specific contract – what does it say? Is your prepayment refundable and at what conditions?

If there’s a clause of refunding you the deposit – what is the probability of a refund?

In most cases, prepayments made for the acquisition of fixed assets or any goods / services in general are rarely refundable, or the probability is very low.

Therefore, your prepayment for a machine is (in most cases) a non-monetary item and as a result, you should NOT recalculate it using the closing rate at the year-end.

The following example will show you how to account for a prepayment for the acquisition of a machine if it’s classified as non-monetary asset.

Example 1 – Prepayment for the acquisition of a machine

Your functional currency is EUR and you entered into a contract for the production of a machine with a US supplier.

Total cost of a machine is USD 100 000, and you agreed to pay in 2 parts:

- Payment 1: USD 30 000 after signature of the contract;

- Payment 2: USD 70 000 after machine’s delivery.

The relevant dates and exchange rates are as follows:

| Date | What happened | Exchange rate |

| 4 February 20X1 | Contract signed | 1.3552 |

| 11 February 20X1 | The first cash prepayment for a machine | 1.3391 |

| 31 December 20X1 | The closing date | 1.3791 |

| 15 January 20X2 | Machine delivered and ownership transferred | 1.3606 |

| 20 January 20X2 | Invoice received | 1.3566 |

| 2 February 20X2 | Invoice paid | 1.3498 |

How and when should you account for these transactions?

4 February 20X1: Contract signed

On 4 February 20X1, you entered into a contract.

However, no asset can be recognized in line with IAS 16 Property, plant and equipment, as recognition criteria are not met.

Similarly, it is necessary to assess whether you should recognize some financial liability or not.

In most cases, no financial liability related to firm commitments is recognized until the goods are delivered (or shipped, depending on Incoterms), and the risks and rewards of ownership have passed.

Conclusion: no accounting on 4 February 20X1.

11 February 20X1: You paid the first payment of USD 30 000

On 11 February 20X1, recognition criteria for recognizing a machine in IAS 16 are still NOT met. Remember, you have no machine yet.

At this point, you cannot control the machine and as a result, “the future economic benefits flowing to the entity” are not probable.

I know that many companies adopted similar practice – they simply book the first payment as debit PPE – machine and credit cash. It is NOT correct, as there is no machine.

So what is the correct entry on 11 February 20X1?

-

Debit Assets – prepayments for PPE: EUR 22 403 (USD 30 000 / 1.3391)

-

Credit Cash: EUR 22 403 (USD 30 000 / 1.3391)

In practice you would use the exchange rate depending on the circumstances:

- If you paid USD 30 000 from EUR account: you use the rate at which your bank recalculated the transaction;

- If you paid USD 30 000 from your USD account: you apply some officially pronounced rate, e.g. rate by the European Central Bank.

31 December 20X1: The reporting date

In this case, the prepayment of USD 30 000 for a machine is non-monetary.

This means no recalculation. Your statement of financial position will show the prepayment at the historical rate, that is in amount of EUR 22 403.

15 January 20X2: Machine delivered and ownership transferred

This is exactly the date when you gain control over the machine. At this point, recognition criteria under IAS16 are met and you can recognize the machine as your own property, plant and equipment.

However, the invoice for the remaining part of USD 70 000 arrived on 20 January 20X2.

What currency rate should you apply?

At the date of transaction.

In this case, the date of transaction is 15 January 20X2, when a machine was delivered and the delivery gave rise to a financial liability.

As a result, your entry should be:

-

Debit Assets – machine (PPE): EUR 51 448 (USD 70 000 / 1.3606)

-

Credit Liabilities – suppliers: EUR 51 448 (USD 70 000 / 1.3606)

This is a very strict application of IAS 21 rules, but let’s be a bit more practical.

It might be acceptable to apply the exchange rate at the date of invoice rather than at the date of delivery of a machine, especially when there’s just a small delay in the invoice issuance.

However, if there’s some big change in foreign exchanges, you should really stick with the machine’s delivery date.

15 January 20X2: What about your prepayment?

On the machine’s delivery date, you need to recognize the machine and measure it at its cost.

A part of machine’s cost is your prepayment paid after contract’s signature. Cost of a machine is a non-monetary item, too – we recalculate nothing at all and keep it in historical rates.

Therefore, you do not recalculate anything and your entry is:

-

Debit Assets – machine (PPE): EUR 22 403

-

Credit Assets – prepayments for PPE: EUR 22 403

Now you may argue – but, the date when a machine appears in your financial statements is on delivery, so we should recalculate the full amount of USD 100 000 with the rate applicable on delivery.

Some companies apply this treatment, but it’s not really correct and presenting true and fair view of the transaction.

The truth is that on machine’s delivery, the recognition criteria are met and you need to recognize the machine at 1 point.

But, the measurement of its cost is a different matter.

Your real cost incurred is USD 30 000 translated with exchange rate on the date of the first payment and USD 70 000 translated with exchange rate on the date of delivery.

Please, just realize that the prepayment of USD 30 000 is no longer a USD asset. It is your EUR asset. Why?

Try to look at it this way: most non-monetary assets stop being “foreign currency” assets at the moment you recognize them in your accounts. So, you don’t have an asset (prepayment) of USD 30 000 in your books – instead, you have an asset (prepayment) of EUR 22 403.

2 February 20X2: Invoice is paid

This should be crystal clear. You record your payment with the spot exchange rate on the date of payment and any difference is recognized in profit or loss.

Your entry would be:

-

Debit Liabilities – suppliers: EUR 51 448 (USD 70 000 / 1.3606)

-

Credit Cash: EUR 51 860 (USD 70 000 / 1.3498)

-

Debit P/L – Foreign exchange loss with EUR 412 (51 860 less 51 448)

The summary of all accounting entries is here:

| When | Amount in USD | Exchange rate | Amount in EUR | Debit | Credit |

| 11 February 20X1 – Prepayment paid | 30 000 | 1.3391 | 22 403 | Assets – prepayments for PPE | Cash (bank account) |

| 15 January 20X2 – Machine delivered and ownership transferred | 70 000 | 1.3606 | 51 448 | Assets – machine (PPE) | Liabilities – suppliers |

| – | – | 22 403 | Assets – machine (PPE) | Assets – prepayments for PPE | |

| 2 February 20X2 – Invoice paid | 70 000 | 1.3498 | 51 860 | Cash (bank account) | |

| – | – | 51 448 | Liabilities – suppliers | ||

| – | – | 412 | P/L – foreign exchange loss | ||

Example 2 – Security deposit for long-term rental

Your company (functional currency: EUR) wants to rent a property in Chicago for 12 months and pays a security deposit of USD 10 000. The deposit will be refunded at the end of rental term.

The relevant dates and exchange rates are as follows:

| Date | What happened | Exchange rate |

| 24 October 20X1 | Contract signed | 1.3777 |

| 1 November 20X1 | Deposit paid | 1.3505 |

| 31 December 20X1 | Closing date | 1.3791 |

Here, the situation is a bit different because as a prepayment is refundable, it is a monetary asset.

When you make a payment, you translate it using the spot exchange rate at the date of payment.

Subsequently, you need to translate it using the closing rate on 31 December 20X1 and recognize any foreign exchange difference in profit or loss.

Here’s the summary of accounting entries:

| When | Amount in USD | Exchange rate | Amount in EUR | Debit | Credit |

| 1 November 20X1 – Deposit paid | 10 000 | 1.3505 | 7 405 | Assets – prepayments (refundable) | Cash (bank account) |

| 31 December 20X1 – Closing date | – | 1.3791 | 154 (7 405 – 10 000 / 1.3791) | P/L – foreign exchange loss | Assets – prepayments (refundable) |

What’s your own accounting practice related to deposits, prepayments or advances in foreign currencies? And, did this article help you?

Please, let me know in a comment below the article and if you know someone who can use this information, please share – thank you!

Update 05 February 2015: There was a great discussion on LinkedIn in relation to this topic. I answered several questions around, as this is very confusing topic and lots of us have some doubts around. Please, if interested, read here.