Example: IFRS 10 Disposal of Subsidiary

Updated 2025: Disposal of a subsidiary step-by-step under IFRS 10 lecture:

Some time ago I published an article with an example of very simple method of consolidating a parent and a subsidiary.

This article still applies and you can learn the basic steps and methodology of consolidation with a nice video in it.

Many of my readers then asked me for a different situation:

How to actually stop consolidation, or deconsolidate, when a parent sells its share in a subsidiary?

In this article, I described various scenarios of how the group can change, so please check that out, it will give you more insights on how to assess the situation and decide what to do.

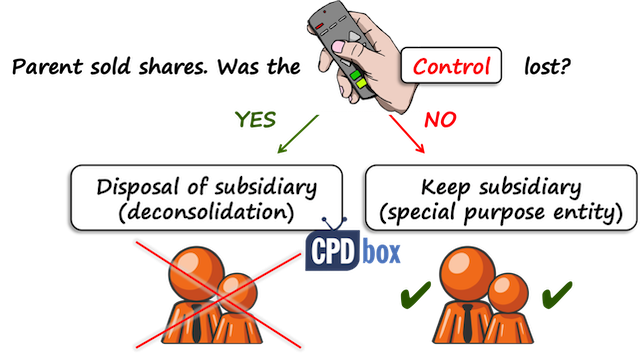

What happens when a parent sells the share in a subsidiary?

We should all look to the standard IFRS 10 Consolidated Financial Statements for guidance.

First of all, you need to assess whether the parent retains control or not.

If the parent retains control and sells the share, then well, you have a special purpose entity here and you still need to consolidate.

But of course, in this case, the non-controlling interest and other calculations will look differently and you can learn more about consolidating special purpose entity here.

If the parent loses control with selling shares, then you need to stop the full consolidation and dispose of the subsidiary.

Here I would like to show you how. Let me illustrate it all on a very simple example.

What’s the situation?

Here’s the question:

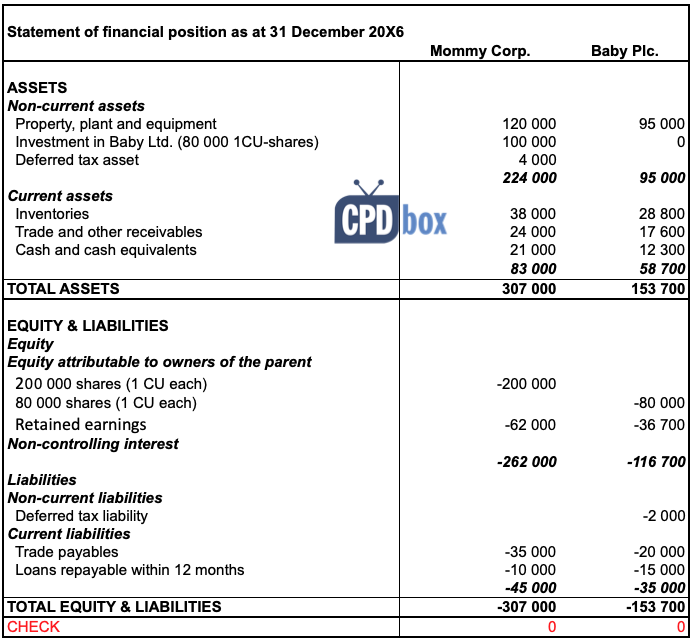

Mommy Corp acquired 80% share in Baby Plc. 3 years ago when Baby’s retained earnings were CU 12 000.

On 31 December 20X6 Mommy sold full 80%-share for CU 180 000.

Mommy accounted for non-controlling interest by the proportionate share method and no impairment of goodwill was charged. Mommy accounted for its investment in Baby at cost in its individual financial statements under IAS 27. Ignore the taxation and prepare consolidated financial statements of Mommy Group at 31 December 20X6.

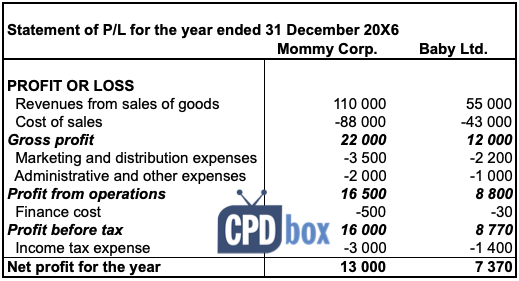

Below there are statements of financial positions of both Mommy and Baby at 31 December 20X6.

And, below are the statements of profit or loss of both Mommy and Baby for the year ended 31 December 20X6:

Prepare consolidated statement of financial position, consolidated statement of profit or loss and consolidated statement of changes in equity of Mommy Group as at 31 December 20X6. Measure NCI at its proportionate share of Baby’s net assets.

Please note here that in the above financial statements of financial position, all assets are with “+” and all liabilities are with “-“, similarly all revenues are with “+” and all expenses with “-“.

You can use whatever method you want, but please, think about it and be consistent!

Believe me, people make most mistakes by messing up with pluses and minuses – simple as that.

What deconsolidation procedures should a parent perform?

When you lose control of your subsidiary by the full sale of shares, IFRS 10 requires you to:

- Derecognize all assets and liabilities of the subsidiary at the date when control is lost;

- Derecognize any non-controlling interest in the lost subsidiary;

- Recognize fair value of consideration received from the transaction,

- Recognize any resulting gain or loss in profit or loss attributable to the parent.

If you are involved in more complex transaction, like selling just a part of your shares, new distribution of shares by your subsidiary and similar, then there are more steps to complete.

However, let’s keep it simple here and focus on the full sale of shares with loss of control.

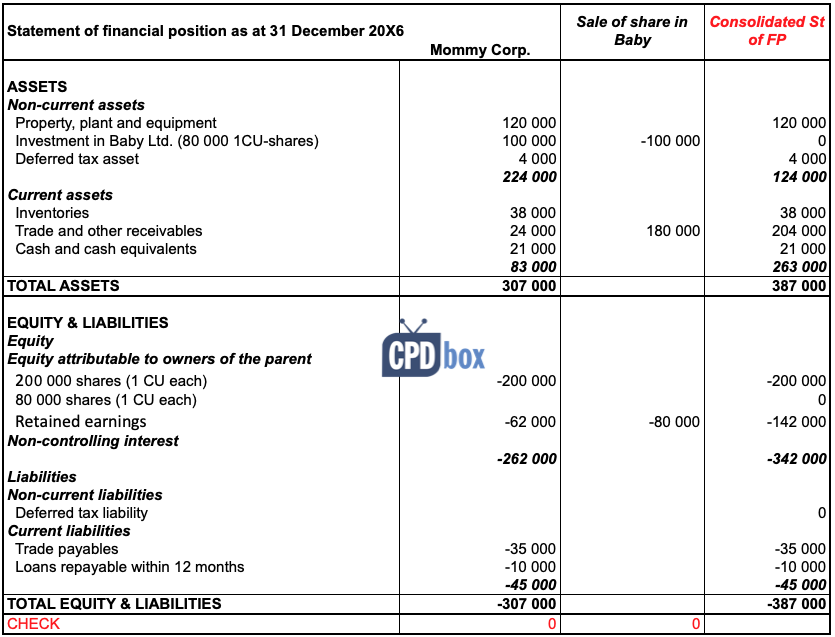

Consolidated statement of financial position after disposal of the subsidiary

First, you need to remove any assets and liabilities of a subsidiary.

This is very easy to perform because you will simply not make any aggregation of assets and liabilities of a parent and of a subsidiary.

Instead, the consolidated statement of financial position will contain only assets and liabilities of a parent.

And no, there won’t be neither goodwill nor investment in a subsidiary.

Easy!

There is one more thing to do though:

You need to calculate parent’s gain or loss on the disposal of shares and recognize it in profit or loss, which will have effect on retained earnings:

- Fair value of consideration received: CU 180 000

- Less carrying amount of investment in Baby in Mommy’s financial statements: – CU 100 000

- Mommy’s profit: CU 80 000

The journal entry is (“-“ is credit, “+” is debit):

| Description | Amount | Debit | Credit |

| Remove Mommy’s investment in Baby | -100 000 | FP – Investment in Baby | |

| Recognize FV of consideration received | +180 000 | FP – Receivables or bank account | |

| Recognize Mommy’s gain on sale of shares | -80 000 | FP – Retained earnings (profit or loss) | |

| Check | 0 |

After we transfer these entries to Mommy’s individual statement of financial position, here we go: we have a consolidated statement of financial position of Mommy group at 31 December 20X6:

Note – the numbers in the last column were calculated as a sum of previous columns.

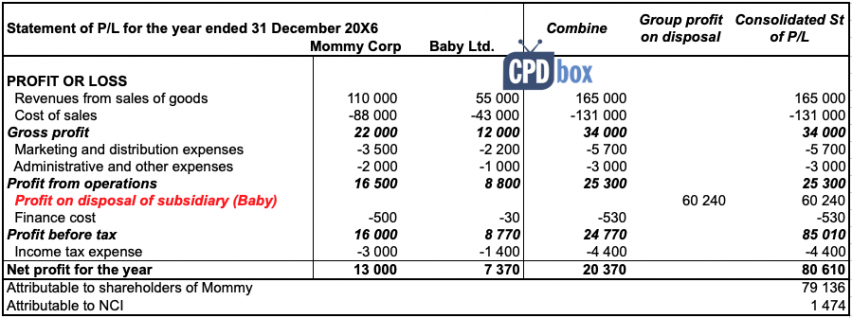

Consolidated statement of profit or loss after disposal of the subsidiary

Consolidated profit or loss statement is not that easy as consolidated statement of financial position, because this statement is NOT a picture at the certain date, but the REPORT about events during certain period.

Mommy held a subsidiary during the full year of 20X6 and therefore yes, you DO NEED to aggregate all parent’s and subsidiary’s revenues and expenses and eliminate intragroup transactions.

On top of it, you also need to calculate group’s gain or loss on disposal of subsidiary in the consolidated financial statements.

Hang on a minute – isn’t it the same as we calculated above?

No, it is not.

Above, you calculated the parent’s gain in the separate statement of financial position – which happens to be the same as consolidated statement of financial position of the Group.

Here, you calculate group’s gain in the consolidated financial statements after you take non-controlling interest and goodwill into account.

So first, let’s calculate goodwill at acquisition (which happens to be the same as the goodwill on disposal, since no impairment has been charged so far):

- Fair value of consideration paid for the investment in Baby at acquisition: CU 100 000 (see Mommy’s individual balance sheet)

- Add non-controlling interest at acquisition, calculated as:

- Baby’s share capital at acquisition: CU 80 000

- Add Baby’s retained earnings at acquisition (per question): CU 12 000

- Total of Baby’s net assets at acquisition: CU 92 000

- NCI’s share of 20% (Mommy acquired 80%, remember): CU 18 400

- Less Baby’s net assets at acquisition (calculated in the above point): – CU 92 000

- Goodwill: CU 26 400 (100 000+18 400-92 000)

Now, we can calculate Group’s gain in the consolidated financial statements:

- Fair value of consideration received: CU 180 000

- Less Group’s share on Baby’s net assets at disposal, calculated as:

- Baby’s share capital at disposal: CU 80 000

- Add Baby’s retained earnings at disposal (per question): CU 36 700

- Total of Baby’s net assets at disposal: CU 116 700

- Group’s share of 80%: – CU 93 360

- Less goodwill (calculated above): – CU 26 400

- Total gain on disposal: CU 60 240 (180 000-93 360-26 400)

Once you have all these calculations, then you should prepare the consolidated statement of profit or loss in three steps:

- Aggregate or combinethe amounts of revenues and expenses of a parent with the similar line items of revenues and expenses of a subsidiary,

- Eliminate intragroup transactions (here we have none due to simplicity),

- Recognize the Group’s gain on disposal of a subsidiary.

Our consolidated statement of profit or loss is here:

Notes: Numbers in „Combine“ column were calculated as sum of „Mommy Corp“ column and „Baby Ltd“ column. Numbers in the last column were calculated as sum of „Combine“ column and „Group profit on disposal“ column.

In this particular example, we aggregated the amounts of Mommy and Baby in full, because the subsidiary was disposed of at the end of the reporting period and therefore all revenues and expenses during the full year belong to the Group.

If a subsidiary is disposed of during the year, you need to include only the amounts of revenue and expenses from the beginning of the period until the date of disposal.

How do we know this was all correct?

OK, let’s prepare the consolidated statement of changes in equity and it will all click like a puzzle!

Consolidated statement in changes in equity

Before we actually prepare this statement, we need to make two more calculations:

- Group’s retained earnings brought forward at 1 January 20X6; and

- Group’s non-controlling interest brought forward at 1 January 20X6.

Let’s start with Group’s retained earnings at the beginning of the reporting period (1 January 20X6).

Since all we have are the statements as of 31 December 20X6, we will perform so-called “roll-back”.

In other words, we will start with the numbers as of 31 December 20X6 and go back to 1 January 20X6:

- Mommy’s retained earnings at 1 January 20X6: CU 49 000, were calculated as:

- Mommy’s retained earnings at 31 December 20X6 (per question): CU 62 000

- Less Mommy’s profit for the year 20X6: -CU 13 000

- Add Group’s share on Baby’s retained earnings at 31 December 20X6: CU 13 864, calculated as:

- Baby’s retained earnings at 31 December 20X6 (per question): CU 36 700,

- Less Baby’s pre-acquisition retained earnings (per question): – CU 12 000,

- Less Baby’s profit for the year 20X6 (per question): -CU 7 370,

- It gives us Baby’s retained earnings at 1 January 20X6 (36 700-12 000-7 370): CU 17 330

- Thereof Group’s share of 80%: 80%*17 330 = 13 864

- Total consolidated retained earnings at 1 January 20X6: CU 62 864 (CU 49 000+CU 13 864)

We also need to calculate non-controlling interest at 1 January 20X6:

- NCI at acquisition (see goodwill calculation above): CU 18 400

- Add NCI’s share on post-acquisition retained earnings of Baby: CU 3 466, calculated as:

- Baby’s retained earnings at 1 January 20X6: CU 17 330 (calculated above at consolidated retained earnings at 1 January 20X6)

- Apply NCI’s share of 20%: 20%*17 330 = 3 466

- Total NCI brought forward at 1 January 20X6: CU 21 866

Fine.

Now, we can prepare consolidated statement in changes in equity and see whether the movement and numbers in make sense. I’ve done it here:

Notes:

- Numbers in the last row are sum of the numbers in previous rows. The same applies for columns.

- The numbers for total comprehensive income for the year, CU 79 136 for retained earnings attributable to Group and CU 1 474 of non-controlling interest, come from the consolidated statement of profit or loss above (look last column at the bottom, you have a split there).

- The balaces of equity accounts at the year-end are only those of Mommy, because Baby is gone.

- DO NOT FORGET to remove any non-controlling interest related to Baby when disposing all of your investment – here it’s in the row „Elimination of NCI at disposal of Baby“.

We are done.

All adds up and clicks.

If you want all these schemes in Excel file, it is available in the IFRS Kit.

Can a parent lose control and keep all the shares?

YES!!!

It really can happen that a parent loses control without selling one piece of shares.

For example – a subsidiary might issue new shares to the third party and parent’s voting rights will be diluted.

Or, some contractual agreement giving control to the parent has just expired and a parent lost control.

If any of these happens and a parent loses control, then you need to deal with the disposal of a subsidiary in a similar manner as described above.

Because remember – CONTROL IS KING!!!

Any questions or comments?

Please let me know below. Thank you!

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

82 Comments

Leave a Reply

Thank you so much this is what I needed.

God bless you.

Dear Silvia,

Is same applicable when parent lost the control due to the fact that subsidiary went into liquidation procedure and liquidator was established by a Court? This happen due to a huge fine from tax authority that makes business to be discontinued and parent decided to leave it as it.

Hi Silvia,

Thank you for your very educative articles.

In a scenario where 10% shareholding is disposed out of 80% holding in a subsidiary which means control is retained (transfer between owners), NCI share increases from 20% to 30%. Assuming that at acquisition date, the initial 20% NCI was measured and recognized at fair value, how should the subsequent 10% increase in NCI be measured and recognized, at fair value or at proportion of Net Assets?

We have loss of control on subsidiary. we will prepare

– Statement of financial position [this will not be referred as consolidated

– Consolidated statement of comprehensive income

– Consolidated statement of changes in equity

– consolidated statement of cash flows.

In next year , we will have Statement of comprehensive income with comparatives of consolidated statemnt of comprehensive income and so on, how will they make sense to the user? and how will it be justified by IFRS , beasue there is nothing specifically mention there. kindly explain.

Hi Silvia

What would be the journals entry to account for NCI at acquisition and disposal ?

For example, do we touch the share capital and retained earnings of Baby (sub) at acquisition eliminating them and crediting NCI? What about at disposal ? How is NCI eliminated in the normal entry?debit NCI vs credit… what?

Thanks

My question surrounds the requirement for consolidating a subsi.

Context: Entity A (parent) has control over Entity B (subsi). In one of your sentence, you mention “a parent loses control when a subsi issues new shares to dilute the parent’s shareholdings.” But the parent basically holds the power to decide whether a subsi is able to issue new shares, as the Parent itself has to authorise the new share issuance in the first place.

Question: Following the above context, can the Parent opt for consolidation exemption for a particular FYE knowing that the Parent willingly authorises the new share issuance within 12 months after the end of the reporting period? Does this dilution of control arising from the new share issuance constitute a ‘disposal’ of shares causing the Parent to lose control?

Hi Hi, please could you help me to understand the calculation of the NCI : where it says ”Add Baby’s retained earnings at acquisition (per question): CU 12 000”

Where did you get this 12.000? I do see in the baby’s statement that the Retained Earnings are 36.700…

Dear Silvia,

how do we treat related party balances between parent and 100% owned subsidiary incase of 100% disposal of subisdiary. if the deconsolidate the subsidiary from the parent. the related party balances will not be eliminated. do i need to declare dividends in parent books to close the related party balances? or is there a another way out.

Dear Silvia

Parent company NAH sold 30% of its share in SYN at a value of SR1,500,000 (FV)

NAH investment in SYN is negative due to prior year losses in NAH books (588,000)

Due to NAH is SR200,000

What will be the accounting entry in this regards.

Please advise

Hi Silvia,

How about the subsidiary in the liquidation process during the financial year? suppose control is now in the hands of the liquidator. In that case, it is no longer a subsidiary right and the parent company should consolidate the profit or loss for the period up to the date before control change hand and shown separately as a discontinued operation?

The example of the complete disposal has been very helpful. However I would love to see and learn how to handle a partial disposal where control is not lost.

Hi Silvia,

Great explanation thnx. My question is : if the parent erases its receviables from the baby as a part of the sale deal, should the amount be recognized as loss or should it not be considered because it is eliminated during the consolidation? Thnx.

Thank you Silvia!

What if company decides to convert its subsidiaries to branches?

Subsidiary needs to remove its equity of the parent’s investment. What is the counter-entry in sub? P&L? Then that subsidiary keeps that P&L in its Retained Earnings opening balance when it starts reporting as a branch?

Also, what else should be booked/thought about? Where can one find the source theory for this type of example? I can’t find much on branch reporting anywhere. I assume it’s similar to consolidation, but without investments and equity?

Hai Silver? I know impairment loss get subtracted to arrive at goodwill at disposal date, what about when goodwill is valued upwards instead of impaired, what value is used for goodwill at disposal?

Hi Silva, what if the NCI is measured at fair value? Do we need to add NCI in group profit or loss on disposal?

Hi, would you please also show the journal entry in consolidation level to record the total gain on disposal CU 60 240? Thank you!

How about going through the above comments and searching for the answer first?

Hi Silvia. Thank you! I got the answer from your above comments. However, we have already made the below entry in parent’s book.

Cr Investment in Baby -100 000

Dr Bank +180 000

CR Retained earnings (profit or loss) -80 000

When we prepared the consolidation financial statement, we book the Bank CU180,000 and recognize the consolidated gain on disposal CU60,240 again, it will be double count. Shall we reverse the above entire journal entries in consolidated financial statement, and book Cr investment in Baby and Dr Share Capital of Baby to eliminate the investment of Baby? Thank you!

Hi Silvia,

Thanks for the ‘eye-opening’ presentation. I wonder what would have happened in case of a joint venture or associate disposal.

Thanks

Dear Silvia,

If parent loss control of the subsidiary without selling one piece of shares (in which subsidiary issued new shares to third party and cause a dilution of parent’s shareholding, do we still need to calculate any gain/loss on deemed disposal when de-consolidation? How should we account for this case? Do we need to reverse 100% of the subsidiary’s net assets or need to retain the new % of its net assets?

Thanks.

Hi Jess, yes, that’s a deemed disposal and the loss of control. As soon as you lose control, you need to deconsolidate fully and account for your investment accordingly – e.g. if you maintain significant influence, then you need to apply equity method. I wrote an article about deemed disposal of an associate – the principle is more-less the same (however, apply appropriate methods). S.

Hi Silvia,

Similar to the example given by Jess above, may i know what would be the accounting treatment if parent (say, joint venture “A”) losses control of the subsidiary without selling one piece of shares (in which subsidiary issued new shares to another Joint Venture “B” and cause a dilution of A’s shareholding. Additionally, A and B has the same owners, hence the transaction may be regarded as business combination under common control. if that is the case, what would be the appropriate accounting treatment in both books? is pooling of interest method applicable? or it will be two different transaction in Joint venture “A” and “B”‘s books?

Thank you.

Hi Foo,

transactions under common control are currently under the discussion in IASB, so no clear rules, so to speak.

Basically, A needs to dispose of subsidiary (that would be “deemed” disposal and I cover similar topic of deemed disposal of an associate here) and then you need to assess the substance of the transaction and yes, perhaps pooling of interest method would work, but anyway, I recommend checking up a status of IASB project on this topic.

I have a scenario. A parent has a 100% owned subsidiary which it is liquidating. The subsidiary has not been trading and has no assets except some cash (say around $300K). The investment in subsidiary in the parent company is $500k. At 31st December, the subsidiary was in a liquidation process. What should be the accounting treatment in the parent and subsidiary books of accounts. Parent prepares individual accounts for each entity as well as the Group Consolidated Accounts. Should the investment be written off in the Parent Books 100% despite the fact that there is a cash of $300k available in subsidiary? At what point the cash should be moved back to the Parent? Should we write-off only the delta (i.e. $200K) in the Parent. Which IFRSs are applicable?

Hi Malik,

In subsidiary’s accounts – if a subsidiary is under liquidation, then I guess going concern does not apply and you should read this article.

In parents separate accounts – it depends which method the parent applies to report its investment, but it seems that at cost. In this case, you need to recognize an impairment. I don’t think 100% write-off is necessary, especially if the recoverable amount of that subsidiary is not zero (but at least 300 K).

As for consolidated accounts – the parent consolidates until it loses control over subsidiary (thus I guess until subsidiary is fully liquidated). Also please be aware of IFRS 5 as the liquidating subsidiary is a discountinued operation.

If you have an only subsidiary and you dispose off during the period. Will your financial statements be called “Consolidated” as at 31 Dec 2019. If my financial statements are standalone after disposal, how do I show comparatives ?

Or Do I still prepare them as consolidated financial statements for 2019 and 2020 and from 2021 standalone only ?

Hi Muhammad, yes, your financial statements will still be called consolidated, because in profit or loss, you aggregate the amounts of revenues and expenses (parent+subsidiary) from 1.1.2019 until the date of disposal. Comparatives are not restated.

As soon as there are no effects of subsidiary to be shown, you stop calling your financial statements “consolidated”. S.

Thanks, that is quite helpful. So my statements would be called ;

– Statement of financial position [this will not be referred as consolidated since as at 31 Dec 2019 you do not own any subsidiary?]

– Consolidated statement of comprehensive income

– Consolidated statement of changes in equity

– consolidated statement of cash flows.

i have a scenario, The group disposed ALL subsidiaries on 24 december, and at reporting date 31 december for interim report (financial year end is 30 June), we only have a single company, how do i recognise the group’s gain on disposal when there is no group existing on 31 december ? So on 31 december, i can only report as a single entity company right?

how we account for the subsidiary under liquidation? if the parent company who own full control over the subsidiary and during the year the BOD take a decision to put the subsidiary under liquidation, is the parent company consolidate the subsidiary or stop consolidate it? and what is the reference from IFRS?

Hi Silvia

I have a question.My Company ( “X”) has 55% in another company(“Y”) and holds 825,000 shares of the 1,500,000 shares of the Company. Company Y sold 131,250 shares at a profit. what are the entries that i need to do?

Hi Yan, not much information here. Are you saying that Y issued new share capital and sold them to the third parties? Or what shares did Company Y sold?

Hello,

What happens if parent sold 100% owned sub to 3rd party in whole, should I include sub’s profit and loss until disposal to the Consolidation?

I heard if you own 100% and sell it off then you don’t recognize daughter company’s P&L.

Thanks,

Manlai

Hi Arthur, yes you do – until the moment of losing control, you need to consolidate fully (including profit or loss of subsidiary).

Hi Silvia,

Your explanation was exactly what I needed. However, I didn’t get what about Statement of cash flows? How to prepare it?

Hi Ainur, I would say that the same way as profit or loss – all cash flows until the disposal date belong to the group and after disposal date you include only parent’s cash flows. S.

Hi Silvia,

Thanks for your reply.

However, shouldn’t we only reflect disposed subsidiary in investing part (direct method) and subtract Cash and cash equivalents of subsidiary as at the date of disposal? However, what about eliminations? Should we need to eliminate cash movements before disposal of subsidiary?

Sure. So, treat cash flows before disposal date as intercompany cash flows; i.e. include them in consolidation and eliminate intragroup transactions. And, include cash flows from the disposal (e.g. proceeds from the disposal) in investing part.

The cash is sitting in liquidated company and yet to be transfered to Parent on the closing date,

How will it be reflected in the statement of Cash flow?

Silvia, so what will happen if a branch is liquidated and the branch figures has been combined from inception ( per local regulation), and due to such a combination- consolidation, there is a carry forward OCI as a result of the translation of currency. Also the parent company does not keep record from a consolidated base, there is a combination process at the end of each reporting period that result in eliminations and adjustments and the OCI per FX translation.

Good day,

If the holding company loses control over a subsidiary and sells all the shares, how would one calculate the profit or loss on disposal if at acquisition there was a gain on bargain purchase and not goodwill?

At acquisition goodwill:

Fair value of consideration

Less: Net asset value

Less: Goodwill

= Consolidated gain / loss

At acquisition gain on bargain purchase / (excess):

Fair value of consideration

Less: Net asset value

Less: ?????

= Consolidated gain / loss

Does the gain on bargain purchase have any impact on the consolidated profit / loss on disposal of subsidiary?

Hi Silvia,

Please explain the difference between when the interest is diluted or gained.

Here is another question that am struggling to solve. P owns 90% of 100 000 outstanding shares of S. on 1 Jan 2019 S issued 20 000 new shares to an independent third party for R200 000. The carry value of identifiable net asset excluding goodwill of S in the consolidated accounts immediateely before the new shares issue is R 800 000, of which R 720 000 is attributable to the P. The carrying value of the NCI at the same date is R80 000.

On the above question am struggling to do the analysis of owner’s equity for S for 1 Jan 2019

Hi Waseem,

As for it is about separate financial statements , it is correct to record gain of CU 10…

Hi Silvia,

Thank you for this, it was really enlightening! However, I have a question regarding income tax: in your example, the income tax does not change even if the profit on disposal of a subsidiary is recognised pre-tax. Could you explain why?

To keep it simple I ignored the tax effects. Maybe I should mention it up there. Thanks.

Hi Silvia,when do we use the following on disposing the fully owned subsidiary,to calculate the G/L on the group level?

Proceeds X

Add: FV of investment still held X

Add: NCI X

Less: Net assets (X)

Less: Goodwill (X)

Profit/(loss) on disposal X/(X), in your example,we did not add the NCI and Investment.

Hi Silvia, for the calculate group gain in the consolidated FS, I can find the same answer based on the difference between the disposal proceed and the group’s share of the post-acquisition profits (losses) of the subsidiary up to the date of disposal (180,000 – 100,000 – 19,760). The CJE should be: Debit Profit on the sale of subsidiary 60,240 and Credit Beginning retained profits 60,240. Is that correct?

Hi Liew,

well, I quoted the full entry somewhere up in the comments, please let me copy it:

Debit Cash received: 180 000

Credit Goodwill: 26 400 (to derecognize it fully)

Credit Baby’s net assets: 116 700 (to derecognize them fully; of course, you need to go item by item – Debit Baby’s liabilities, Credit Baby’s PPE… you get the point I hope)

Debit Non-controlling interest on disposal: 23 340 (to derecognize it fully)

Credit Group’s gain on disposal: 60 240

Hi Silvia,

Thank you for the clear explanation. but I am a little bit confused with this journal, we have debit cash when we recognized disposal of investment in the subsidiary (in parent’s book, 1st journal that you wrote). Then we debit the cash again in the consolidated FS. It looks like we record cash twice.

Melissa, this entry is the full entry – that is, not an adjusting entry. It means you would book this entry to the consolidated FS as if nothing happened in the individual accounts. You can do it if you like, but then do not forget to reverse entry in the individual FS. I only brought this entry because someone asked. If you are doing just adjusting entry, please look to the article and you will see there is no cash involved. I hope it helps.

thanks Silvia, but how do we eliminate the investment held by parent in the above entry?

Please, do not confuse the individual parent’s statements with consolidated ones. The above entry is for consolidated statements and there is no single line for investment held by the parent. Instead, you eliminate the investment by crediting the individual line items (PPE, etc.). Your question relates more to individual parent’s statements where the entry is simply Debit Cash (or receivable) from sale of investment, Credit Investment in subsidiary, Credit Profit on sale of investment.

Hi Silvia, If a fully owned subsidiary is recorded at CU 100 and separate goodwill of CU 20; we sell 20% stake at a price of CU 30 (gain of CU 10). What entries will be recorded, Any gain will go to P&L? will the proportionate goodwill be de-recognized and charged to P&L?

Hi Silvia

I was wondering if you could assist me with the “acquisitive ” case study?

Really desperate for some help and would really appreciate it.

Regards Zee

Hi Zee, what is that?

Thank you for the timeous response,Silvia. It is part of the framework based IFRS teaching material, Is there anyway that i could upload it or email you so that you can have a look? It can be found at http://archive.ifrs.org/Use-around-the-world/Education/Documents/Framework-based%20teaching%20materials/Acquisitive-case-study-2015-final.pdf .

I am confused about issue 3. Reorganisation. Hope you can provide assistance,

Regards zee

A parent is holding following in wholly owned subsidiary S

100 shares bought at Rs, 10 since inception

plus 20 shares issued as onus shares .

Subsidiary S has bought back 10 shares at 15 each

Question 1 – In separate financial statement for recognising profit Cost of the shares sold should be calculated using average cost of holding or Taking FIFO method.

Question 2 – what will be the treatment. In CFS.

Dear Silvia,

my company had 100% share in X Plc. During 2018 the subsidiary entered into bankruptcy procedure, and I assume we have lost the control. However, the subsidiary was operating with heavy losses, and entered the bankruptcy procedure with 1,7 Mil negative shareholders equity. The bankruptcy trustee now manages the subsidiary, and we have no control over assets or liabilities of the subsidiary. How should we account for this in our consolidated financial statements? I assume, we have to derecognize our investment in balance sheet statement, aggregate revenues and expense until the date of loss of control, but what should we do in statement of changes in equity? There are no net assets (i.e.) they are negative. Do we have a loss on disposal or nothing? Thanks!

Thanks for the detailed explanation .Kindly clarify , how the gain on sale of investment in subsidiary will be reversed if we do a line by line consolidation. Will it amount to double accounting of gain in consolidated financials when we compute gain on loss of control in consolidated financial statements (group books ).

Hello Silvia, Thank you for the detailed example.

Have doubt on the following two points.

When you say there is a profit of 60,240 at group level. Where will the second impact in the Consolidated financial be?

And also how will 80,000 profit at Standalone level will get reversed in Consolidated Financials?

Dear Silvia, I have a question. Let’s assume a 31 December year end and Mommy Corp sold Baby on 30 September. Assuming it’s a share deal where the acquirer takes on all assets and liabilities, does it mean: (1) that Mommy must derecognise all assets and liabilities, including cash collected on sales

(2) Revenue recognised up to 30 September must also be de-recognised? Let’s assume Baby booked $10 million in sales up to 30 September.

Thanks Silvia.

Regarding 1/1/20×6 (opening) retained earnings 62,864, does it automatically tie to prior year 12/31/20×5 closing retained earnings ?

Same question. will it tie?

Hi Silvia.

Thanks a lot for this explanation. That is very clear.

The only thing I do not understand is what is the journal entry to recognise the group gain on consolidation?

Thanks in advance.

Hi Celia,

great question. Actually, I did not prepare consolidated statement of financial position after disposal from consolidated statement of FP before disposal – instead, I chose the easier method of just doing it from Mommy’s individual statement of FP as this is what is left.

But, if your starting point is consolidated balance sheet, then you must derecognize all Baby’s assets and liabilities (=net assets), all goodwill and all non-controlling interest left. The entry would look something like:

I hope it helps! S.

Hi

What about the profit on disposal of subsidiary in parent company books? is it same figure?

Hi Silvia, this has been extremely helpful as I’m quite rusty on these concepts, thank you. I was wondering how the consolidated Financial Position balances if the Group Profit/Loss on disposal recognised in P/L on consolidation differs to the gain/loss recognised in the parent – adj to Retained Earnings as per your example. So you have R60 240 going through the P/L for group gain which ultimately goes to retained earnings on the consolidated financial position right? Perhaps if you could send me the jnl entries for the R60 240 group gain recognition that would be helpful…

HI Sylvia,

Thank you for your great explanation,

I understand that if a subsidiary is liquidated with loss situation during the year, de consolidation is dealt with in a similar manner as described above because a parent loss control. Is it correct?

Thank you very much for your help

Hi Silvia, can you explain how to record the transactions, when a subsidiary is sold among the same group, that is subsidiary shareholding is changing from one entity to another entity, but with in the same group.

Hi Praveen, interesting question. It depends what the relationship between the new parent and the “old” parent is, so I cannot give one general answer to this question.

Silvia, hello.

I can give you more details, as it is my case, as well

My entity, Parent, is 100% subsidiary of GrandParent. Also my Parent till October’2019 owned 100% of Daughter (which previously was 100% subsidiary of GrandParent directly).

In October’2019, Daughter was sold to GrandParent.

What I’ve understood after consultations with my colleagues, as we use “predecessor valuation method”, we simply do the same, – write-off all assets, liabilities and equity of Daughter, without any P&L effect.

Hello silvia thanks for explanation. Would you mind please send examples of the following or where i can get examples of these:

1.Parent hold 80% and disposed 20%, retaining 60% control. How to do the consolidated SOFP and SOCI with debit and credit entries in standalone parent and standalone subsidiary FS

2. Parent hold 80%, dispose 40% mid year, retained 40% and loss control. How to do SOFP and SOCI with double entries in parent and subsidiary stand alone accounts

Hello Silvia,

There was a question on this in ACCA Dip IFRS June 2018 exam for the first time.. Somehow I managed and passed. But, your explanation enhanced conceptual clarity.

You are doing great work for IFRS students and professionals..

Thanks.

Congratulations, that’s great Thank you for your kind words! S.

Thank you for your kind words! S.

Thank Silvia! This very interesting.

Miss silvia,

I thought that we need also to show and apply discontinued operation in income statement or in the notes.

Actually, if the transaction met the definitions as per IFRS 5, then yes, of course. But this was not the aim of this article and I wanted to illustrate just one piece of knowledge to focus on disposals. But you had a great point

To qualify as a discontinued operations it has to meet 3 criteria mentioned in IFRS5. If the disposed subsidiary is not a separate major line of business, then it it does not meet IFRS 5, and should not be presented separately as discontinued operation in the financial statement.

This is an indeed interesting way of reading IFRS 5.

miss Silivia, this is helpful. god bless you.

this is what I needed – thank you so much!