Component accounting for PPE (IAS 16) with examples

Question:

We operate a business in which we deploy heavy equipment. Some parts of that equipment need to be replaced regularly. Our auditor pointed out that we should apply component accounting in line with IAS 16. What is it and how can we apply it?

Answer

The standard IAS 16 Property, Plant and Equipment prescribes in the paragraph 43 that

„Each part of an item or property, plant, and equipment with a cost that is significant in relation to the total cost of the item shall be depreciated separately.“

This principle is referred to as a component accounting.

Here are simple few steps to apply it:

- Identify an item of property, plant and equipment that might contain a part with a cost significant to the total cost. Focus on the factors listed below.

- Split the acquisition cost of that asset.

- Set the useful lives of the part and of the remaining asset.

- Depreciate those two parts as two separate assets.

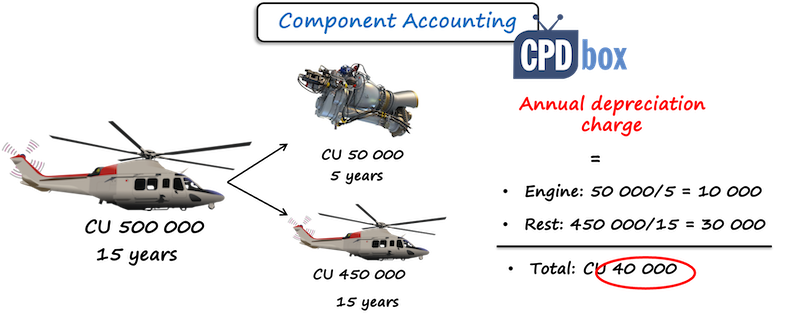

Practical example

Imagine you purchased a helicopter for 500 000 CU. Its economic life is 15 years, but after 5 years, you are required to replace helicopter’s engine due to legal regulations.

The estimated cost of a new similar engine is 50 000 CU, which is significant in relation to the total cost of the helicopter (10%).

As a result, we need to apply component accounting and calculate the depreciation charge of the helicopter as follows:

- Depreciation of an engine over 5 years: 50 000 CU / 5 = 10 000 CU;

- Depreciation of the remaining part over 15 years: 450 000 CU / 15 = 30 000 CU;

- Total annual depreciation charge: 40 000 CU.

After 5 years, the carrying amount of the helicopter excluding the engine will be 300 000 CU (450 000 – 5*30 000). The carrying amount of the engine will be zero – time to replace it.

For the sake of completeness, let me add that in line with IAS 16.70, when a component is replaced, the carrying amount of the old component must be derecognized, even if it was not separately identified when the asset was originally acquired.

Therefore, you need to derecognize the old engine after 5 years, and recognize the new one.

What factors indicate the need to apply component accounting? (+real-life examples)

Let’s see on a few real-life examples, thanks to Ms. Barbora Choi – the accounting expert and IFRS content creator.

- Maintenance and repair processes on parts

Example: Komatsu Ltd.

“We collect significant components like engines and transmissions from construction and mining equipment that has been operating at customer. Through various processes (disassembly, cleaning, salvage or replacements of parts, reassembly, painting, shipping inspections), these components are restored to be like-new.”

Likely, those components are depreciated separately at customers.

- Specific nature of a component (risk, special handlings)

Example: The Korea Electric Power Corporation

Loaded heavy water is used for cooling of condenser equipment at nuclear plants. It requires special handling, storing and disposal. Useful life is determined separately from the plant and other equipment as of 30 years (note: this demonstrates component accounting).

- Distinct depreciation pattern

Example: Airbus

“Useful life of jigs and tools is 5 years (straight-line depreciation). If more appropriate, some tools are depreciated using the number of production or similar unis expected to be obtained from the tools.”

This demonstrates that certain assets with different useful lives require separate depreciation.

- Procurement strategy

Example: Air Lease Corporation

“For new aircraft deliveries, we source many components separately, which include seats, safety equipment, avionics, galleys, cabin finishes, engines and other equipment. Oftentimes, we are able to achieve lower pricing through bulk purchase contracts with the component manufacturers such as Airbus and Boeing.”

Since these components are purchased separately, it is likely that they are depreciated separately in line with IAS 16.43.

- Reuse and/or recycling

Example: Deutsche Bahn

“If DB Group still has to discard a vehicle, it is either resold or components that can still be used are removed and the rest of the vehicle is sent for recycling.”

Although this practice does not directly relate to component accounting, it indicates that components may have a distinct useful life and residual value (thus component accounting might be appropriate).

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

Leave a Reply