Top 4 Changes in Profit or Loss Statement under IFRS 18 (with video)

The new standard IFRS 18 brought a few significant changes in the financial reporting, especially in profit or loss statement.

Let’s examine the top four of them and illustrate them on simple examples.

#1 New categories of income and expenses under IFRS 18

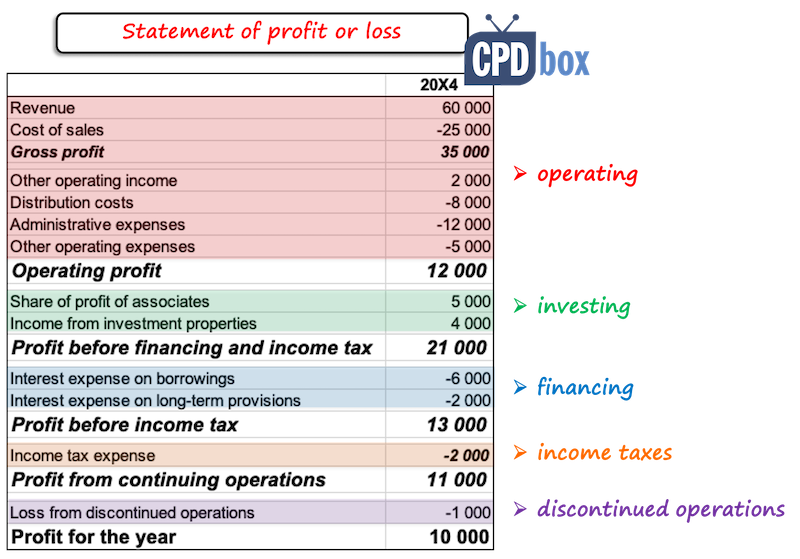

Under the new IFRS 18, we need to classify income and expenses in profit or loss into five categories (IFRS 18.47):

- Operating;

- Investing;

- Financing;

- Income tax;

- Discontinued operations.

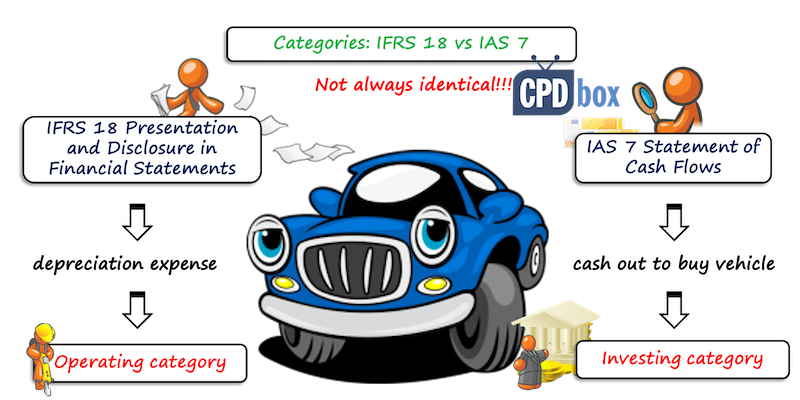

Here I’d like to stress that the first three categories (operating, investing and financing) are indeed a new requirement.

While they might resemble the categories in statement of cash flows under IAS 7, they are NOT the same.

For example, imagine a company purchases the new machine to use in the production. Here’s the difference:

- In the profit or loss statement under IFRS 18, the depreciation of that machine is classified in operating category;

- In the statement of cash flows under IAS 7, the expenditure (cash outflow) to purchase that machine is classified in investing category.

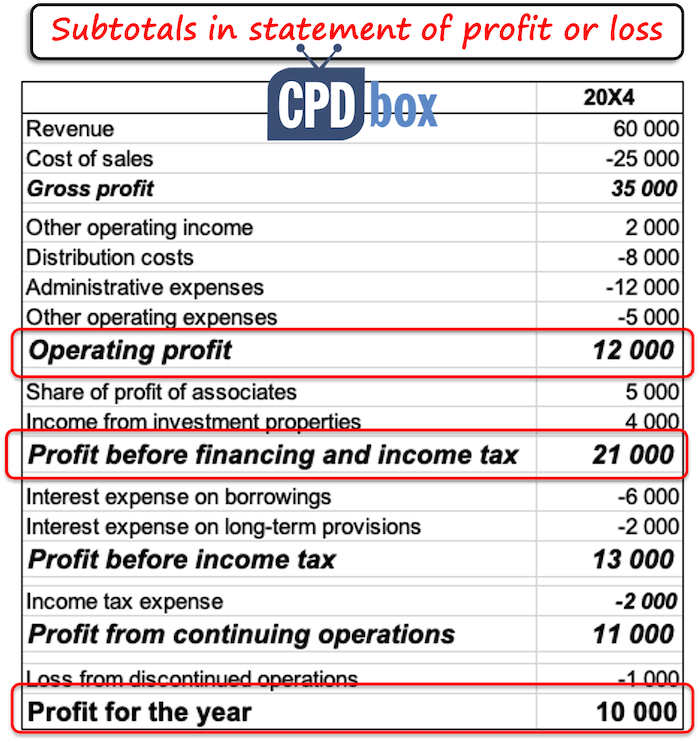

#2 New mandatory subtotals in profit or loss under IFRS 18

This is very logical requirement, because under older standard IAS 1, the companies presented subtotals as they liked, often making the financial statements incomparable between individual entities.

IFRS 18 requires presenting three subtotals (IFRS 18.69):

- Operating profit or loss: here, all the items presented in operating category are included;

- Profit or loss before financing and income taxes: this is the sum of operating category and investing category;

- Profit or loss: the resulting profit or loss including all income and expenses.

The first two subtotals are new requirement.

Please note that there is no need to present the separate subtotal for investing category or financing category like in statements of cash flows.

Instead, the profit or loss is built up adding more and more line items to the operating profit or loss subtotal.

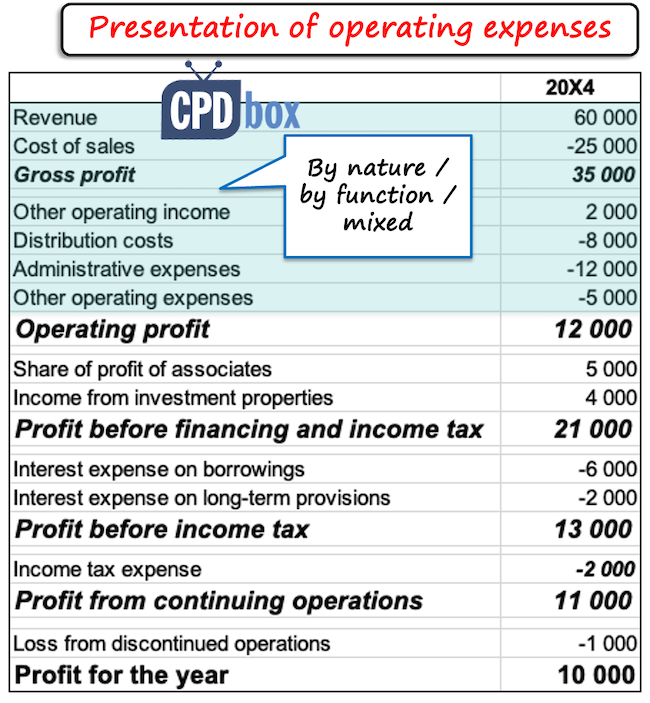

#3: Presentation of operating expenses by function, by nature or on a mixed basis

This requirement is not totally new, but IFRS 18 is making them more precise, explicitly permitting to present the mixed basis presentation.

The method of presentation is not the choice – IFRS 18 gives guidance on how to determine which presentation is most useful.

If you are presenting on “by-function” basis on the face of profit or loss statement, then you need to disclose also “by-nature” presentation in the notes (so effectively, you need to work out both methods).

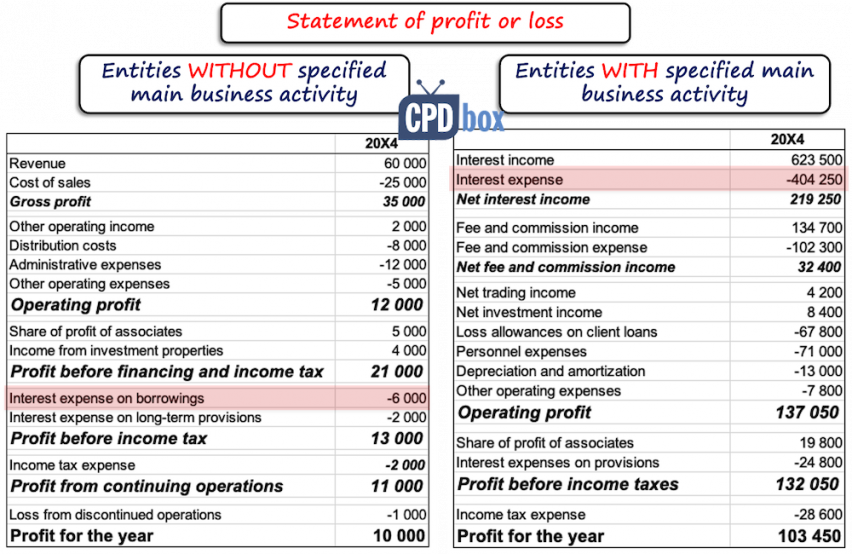

#4: Additional requirements for entities with specified main business activity

Prior we classify income and expenses into operating, investing or financing category, we must determine whether the entity has specified main business activity or not.

This is also logical, because the general format of profit or loss might not fit all the businesses.

More specifically, IFRS 18 sets additional requirements for two types of business activity:

- Investing in assets: for example, investment property companies, investment entities (e.g. funds), insurers;

- Providing finance to customers: for example, banks, lessors, manufacturer/dealer financing companies, etc.

If the company assesses that it indeed has one of these specified activities as its main business, it classifies certain items differently from other entities.

For example, interest expenses on loans:

- Manufacturing company without specified main business activities classifies interest expense in financing category; but

- Bank providing loans to customers classifies interest expense in operating category, especially when it is incurred on borrowings used to provide financing to customers.

Here’s the comparison of the two statements of profit or loss:

Video lecture: Top 4 changes in Profit or Loss explained

You can watch the free lecture here:

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

9 Comments

Leave a Reply

Thank you for the answer. Just one more thing to clarify please. You wrotr thaht under IFRS 18, gains and losses from trading securities are classified within the operating category. But if my company is not financial company? Would that mean gains and losses on equity holdings less then 2% would be classified in investing category having in mind paragraph B47. of IFRS 18? It says same category as dividends from that holding.

Will gains and losses for securities held for trading be categorized within investing category?

No — under IFRS 18, gains and losses from trading securities are classified within the operating category, not investing.

Excellent Silvia

Many thanks Silvia for the heads-up. At least we can be thinking it application before effective date. How do these changes play out in the NGO accounting?

Hi Ameyedowo,

thank you! Well, that depends whether NGO applies full IFRS or not. If yes, then accordingly as any other entity.

Under IFRS 18 where we classify the following

1. Extraordinary expenses ( Reveunues )

2. Interest Expenses Under IFRS 16

1. Operating category, because it is default – which means that if you cannot classify some expense or income as either investing or financing (or income tax or discontinued operation), then it is automatically in operating.

2. For most entities financing.

Very informative