What is the lease term of cancellable property rental contracts under IFRS 16?

“A company has opened a branch at a building, by signing a rental agreement with the landlord of the building on which branch is situated.

The initial agreement will be for 10 years and either party can terminate the agreement at any time by giving two month’s notice.

The tenure of the agreement can be extended at both parties consent. The company has no intention to discontinue the branch operations in near future. However, loss-making branches may be subject to relocation or closure in the future.

What is the lease term in this case? And, how to account for this lease?”

Answer: Watch out for non-cancellable period

This is a great question, because similar contracts are very common.

In many rental contracts there are provisions about terminating the leases by any party, either by the lessee or by the lessor and exactly these provisions can deeply affect how you are going to account for the leases.

The new lease standard IFRS 16 was issued in 2016 and it’s mandatory to apply it for the periods starting on or after 1 January 2019.

It introduced the revolutionary change in accounting for operating lease contracts by the lessees.

Under IAS 17, as long as the lease is operating, you just book the rental costs as an expense in profit or loss and that’s it.

Under IFRS 16, you as a lessee do not classify the lease anymore, but instead you recognize all the leases in the same way:

- You recognize the right-to-use asset and lease liability in the statement of financial position, and

- Each rental payment is then split to the reduction of the lease liability and finance cost,

- Plus, you amortize the right-to-use asset.

That’s very short summary of IFRS 16, but if you want to know more, I published a few articles about it, they are freely available here.

If you really need to know it well, then I recommend checking out my IFRS Kit that teaches you IFRS 16 and other standards in a very easy way, step by step, with lots of practical examples in Excel.

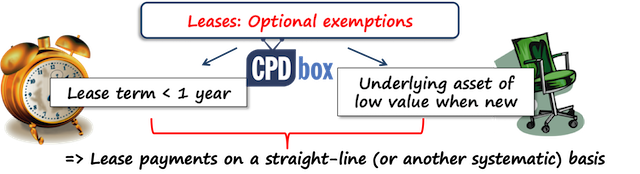

There are few exemptions when you do not have to account for the right-of –use asset:

- The lease is either short-term, that is for 12 months and less with no purchase option, or

- You are leasing the asset that has low value when new, like computer or furniture, just as an example.

These are optional exemptions, so you can take them, but you don’t have to.

Let’s get back to the question – do we have the short-term lease here? Or not?

Well, IFRS 16 says that the lease term is non-cancellable period of the lease. Non-cancellable period means that the contract is enforceable during that period.

If any part can terminate the lease unilaterally, or without the consent of the other party, and there are no significant penalties, then the contract is no longer enforceable.

The question said that the lease was for 10 years, but any party could terminate the lease anytime with 2 months notice.

What does it tell you?

Is the lease non-cancellable?

No, it is not. In fact, it is cancellable within 2 months and there’s no mention about the penalties.

In fact, the lease is non-cancellable just for the period of 2 months, not 10 years.

Here, you can’t take into account the assumption that the company does not plan to relocate within the near future.

It does not matter, because also the lessor can cancel the lease without any penalty.

The situation would be different if the right to terminate the lease on a short-term notice has just one party:

- If the right to terminate the lease with 2 months notice has just the lessee and the lessor must keep the lease term at 10 years as agreed, then the right to terminate is the same as the option to terminate.In this case, lessee would assess how long would he want to stay in the property based on many factors.

- If the right to terminate the lease has just the lessor, not the lessee, then the non-cancellable period includes the period covered by the option to terminate the lease (just 2 months in the question). However, please be careful here, because a lessor’s right to terminate is often ignored when determining the lease term, because the lessee must pay for ROU for the period of lease (until the lessor terminates). Thus it would be 10 years if the lessor’s right to terminate is ignored.

Finally, how to account for such a lease?

Well, as soon as you understand that the lease is non-cancellable only for 2 months in this case, it is a short-term lease and you have 2 options:

- Either you can apply the exemption for short-term leases and book the rental payments as expenses in profit or loss. Just be careful, because you should apply this exemption to all class, not on one-by-one basis.So, let’s say you’re a bank and you regularly rent the offices for your branches with similar terms, you have to apply the exemption to all of them, not selectively.

- The second option is not to apply exemption, but account for the lease as for any other lease, that is – right-of-use asset, lease liability, etc.But, in this case, I would not recommend it because it would be highly impractical for various reasons.

If you want to learn more about the new lease standard IFRS 16, then I strongly recommend checking out my IFRS Kit – it fully covers new IFRS 16 in step-by-step videos together with highly practical examples solved in excel.

My thanks

Hereby I would like to thank Mr. Bostjan Pecnik for the interesting conversation related to this topic and for additional guidance he provided.

JOIN OUR FREE NEWSLETTER AND GET

report "Top 7 IFRS Mistakes" + free IFRS mini-course

Please check your inbox to confirm your subscription.

46 Comments

Leave a Reply

Hello Silvia

Just a quick real case scenario!

A company entered into a 5 yr contract for leasing its office space, but in the contract the lessor says that the premises will be used only as an office.

The question is, shall i recognize these as a lease or not?

Best regards

Prodromos

hi Prodromos, I cannot say for sure without seeing the full contract, but I would say yes, there is a lease under IFRS 16.

Hi Silvia,

How to measure a lease contract by a Lessor under a Finance Lease at commencement: where the lessee has an option to increase the leased space (option to increase the scope of the lease) at a relatively below-market additional lease payments (the option is probable of being execised)?

For example the market value is 1000$ per sq foot and the lessee’s option is to pay 600$ per sq foot for the additional space.

So the additional lease payments for the additional space are not “commensurate” to original space and are not to be accounted as a separate lease.

The question is if the expansion option is to be treated as either:

(A) an increase in the leased space AND an increase in the lease payments (like it is an integral part of the lease contract, not an option), (like IFRS15,B43) (addition of 1000$ per the expected additional sq footage to the lease payments), (i know this is to be accounted under IFRS 16 and not under IFRS 15) ; or

(B) like a “customer’s material right”: allocate part of the contract consideration to the fair value of the option (Option’s contract price is zero the options is given for free. Options fair value is (1000-600) = 400$ times the optional square footage) and defer the revenue recognition relating to that consideration until it is exercised or expires?

Thank you 🙂

Yifat

(A) is to be addition of 600$ expected increase in lease payments, not 1000$

another possibility (C) is do nothing until the lessee exercises the option and increases the leased space (increases the scope of the lease)

Which possibility is correct? (A), (B), or (c) ?

Hi Silvia,

Thank you for making this cpdbox a very helpful place to learn IFRS.

I have one lease problem that I really need to solve. There is a Company entering the land and building lease agreement with its related party since 2012. It’s a month-to-month lease. The agreement in the lease does not specify the term of the lease, It just states that the lease period starts from 1 May 2012 until the undetermined date. Until now, there is no revision in the agreement and the Company still leases the land and building. My question is, how long I should determine the lease term if the date of IFRS 16 initial application is 1 January 2020? Thank you.

Regards.

Hi Silvia, I have an interco lease for 1 year with options to renew for another year. The lease can be terminated by either party by giving 3 months notice. Assuming the termination cost is insignificant, do we need to consider other economic terms to assess the lease if we already know that either party can terminate it by giving 3 months notice. Also would the answer be different if economic substance of the termination is not insignificant?

Hi Silvia,

I havea lease for 10 years with a break clause by the lessee after 2 and 5 years. Would we capitalise the lease upto 2 years only, dispose and then reapply IFRS 16 for a further 3 years if the break cluase was not taken?

Thanks

Hi Silvia! I have been following IFRS Box (now CPD Box), and have learned so much from you, almost my entire audit career (7 years and counting). But I disagree with you on this one. The determination of short-term lease is consistent with the definition of a lease term i.e. the options to extend should be taken into account if an entity is reasonably certain to exercise an option to extend (OR NOT TO TERMINATE) a

lease (and the lessor too, is reasonably expected to NOT terminate the lease before the end of the contract period). Even if the mutually enforceable “NON-CANCELLABLE’ period is only 2 months, but the entire lease term is 3 years, with an option to extend for 1 year – if there is an incentive for the lessee (and the lessor) to NOT TERMINATE and continue with the lease for the entire period (3 years), we need to include that as part of the “lease term”. It is like an IMPLIED option to extend, even if the explicit option to extend is the PLUS 1 after Year 3. If management assess that based on judgement, they will fully utilize the original 3 year period, and the lessor will also not terminate the contract – then that is an IMPLIED option to extend we need to add to the 2 months non-cancellable period.

We are a school. All houses/apartments we rent are for a period of one year with no option to buy. Does IFRS 16 apply to our rental agreements?

Hi Silvia. Thank you so much for your work, its help me a lot in clearly understanding IFRS.

I have a query, at the end of the lease contract, do we need to remove the ROU and its Accumulated ROU Depreciation from Balance Sheet? or just leave it in books as the NBV is Nil ?

(fyi, as I recorded the cost of ROU and its Accumulate Depreciation in 2 separate account.)

Hi LS, you will remove it completely from the books since you no longer have the underlying asset for your use.

Hey Silvia, thanks for the insight provided. I want to know how to interpret (a) and (b) of the lease term definition? As IFRS 16 states that (a) periods covered by an option to extend the lease if the

lessee is reasonably certain to exercise that option; and (b) periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option. So if the lease in your example is 10 years with an option to extend for 5 years – assume its certain that the option will be excercised – I will include the 5 years but ignore the 10 years that I am likely to use within the agreement itself? This makes no sense. Also, does this mean where I have a lease with a related party which is not in writing it will be treated as an expense even if it is likely that the lease will continue perpetually?

Hi Selvia

I confused for if I’m in operating lease with no intention to buy at the end of agreement beside in contact a condition of lessee has a wright to terminate put he should pay a full period.

I.E

the rent from related party in a monthly rent invoice as before

need your advise in applying IFRS 16

Hi Silvia,

I have one situation which is confusing.

For this current Financial Year ending 31 December 2019, the contract already expired on 31/12/19 and the contract is actually started in 2017. The company already renewed the contract for another 3 years which is until Dec 2020. Please noted that the current contract(expired 2019) doesn’t provide option to renew.

So my questions is, for FYE 2019, should i consider the renewed 3 years in 2019 lease term calculation?

Thank you

Sorry. typo. The company renewed the contract for another 3 years until Dec 2022.

Hi Sylvia,

I have always refer to you IFRS box when i have something difficult to understand regarding any MFRS. In here, your explanation was understandable and sufficient to confirm the understanding after reading other materials and the standards itself.

Your article is like summary of other length materials where it would confirm and strengthen of what i understand elsewhere.

I would like to say thank you for this.

Thank you. Teacher!

I just want to say

Well, as soon as you understand that the lease is non-cancellable only for 2 months in this case, it is a short-term lease and you have 2 options:

1. Either you can apply the exemption for short-term leases

2. The second option is not to apply exemption (I would not recommend it because it would be highly impractical for various reasons.)

Hi Silvia,

Thanks for the explanation on IFRS -16, as usual.

I have a small query on your non recommendation of option 2 in the above point.

What can be the impractical reasons ?

Further, as we know that the IFRS 16 is a game changer standard which will have significant impact on the financial statements.

All other contents assuming same ” and with addition of One line stating that either party can terminate the agreement at any time by giving two month’s notice.” and you recommending for shot term leases gives an indication that the lessee may enter (or gets encouraged to enter) into similar contracts with such conditions and easily escapes from the provision of IFRS 16.

Thanks!!!

If the lease is short-term and you do not apply the exemption, then you would need to account for ROU asset and lease liability even for 2 months – that is impractical and this was my point. And I understand your point about easily escaping the provisions of IFRS 16 – but I am not so sure that this would genuinely happen. In general – if the lessee has a right to terminate with 2-months notice, then this is taken as an option to terminate as I wrote above and then the lessee must assess for how long the asset will be used (that is – not automatically apply short-term lease exception). I write about it more above.

Hi Silvia, Thank you so much. Your work has help me a lot in clearly understanding IFRS.

In the above question you have considered termination clause due to which lease contract will be considered as short term contract and accounted accordingly but if the same contract also has an option with lessee to extend the lease term for another 5/10 years and he is reasonably certain to avail that option whether the same will again be considered as long term lease contract?

Thank you so much in advance. I really admire your work

I would also really like to know what we should do in such a case. Because, the lease term is actually, not only the “non-cancellable period” but rather (As per the standard) :

The non-cancellable period for which a lessee has the right to use an underlying asset, together with both:

(a) periods covered by an option to extend the lease if the lessee is reasonably certain to exercise that option; and

(b) periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise that option.

Currently dealing with such a situation, looking forward to a reply from you Silvia 🙂

The determination of short-term lease is consistent with the definition

of a lease term i.e. the options to extend should be taken into account if an entity

is reasonably certain to exercise an option to extend (OR NOT TO TERMINATE) a

lease. I have loved Silvia ever since she started the IFRS Box, and have learned so much form her, almost all my entire audit career (7 years and counting). But I disagree with her on this one. Even if the enforceable “NON-CANCELLABLE’ period is only 2 months, but the entire lease term is 3 years, with an option to extend for 1 year – if there is an incentive for the lessee to NOT TERMINATE and continue with the lease for the entire period (3 years), we need to include that as part of the “lease term”. It is like an IMPLIED option to extend, even if the explicit option to extend is the PLUS 1 after Year 3. If management assess that based on judgement, they will fully utilize the original 3 year period – then that is an IMPLIED option to extend we need to add to the 2 months non-cancellable period.

I need your opinion on following lease –

We are taking various Motor Car on lease for use by our employees, mostly are 12 months contract period but some have contract period of more than 12 months as well, but all such lease are cancellable on 1-2 month notice period.

Does we need to capitalize such motor car as ROU

Hi Silvia,

If the lease contract includes a penalty clause on early termination, how the lease term will be determined in such a case ? And what would be the treatment of penalty, as to whether it would be considered while calculating present value of lease liability on inception or will be charged to P&L when incurred ?

Thanks in advance !!

Hello Silvia,

Can housing/ accommodation benefit in kind provided to company executives be recognized under IFRS16?

Hi Silvia,

Thank you for this article, it’s so helpful. Can you please clarify, You indicated above that there are ‘few exemptions when you do not have to account for the right-of –use asset;

•The lease is either short-term, that is for 12 months and less with no purchase option, or

•You are leasing the asset that has low value when new, like computer or furniture, just as an example.

Shouldn’t it be ‘AND’ and not ‘OR’? Kindly confirm. Thank you

OR 🙂

That is – you can lease a furniture costing 500 USD for 3 years – that is a “low value lease” and you can apply the exemption although the lease is for 3 years.

Or, you can lease a big car valued 100 000 USD for 11 months – again, you can apply exemption as the lease is shorter than 12 months (although the value is not low).

how about extension another 11 months

Dear Silvia, hope you are doing great, got a quick quiz, if a machinery has a purchase option but at the time of the agreement it is not known that it would be exercised or not after say payment of 3 year of lease rental as per the agreement, how it is accounted in the books, is only the PV of lease rentals is considered for the capitalization.

Thanks

Hannan

Hi Hannan, well the standard IFRS 16 contains the guidance to assess whether it is probable that the option will be exercised or not. E.g. if the conditions of the options are more favorable than the market conditions, then there is an incentive to take that option. In any way, you should assess the terms of the option at the inception of the contract as your best possible guess based on the terms of the option and then set up your lease schedule. If the outcome is different, then you need to account for lease remeasurement.

Dear Silvia,

appreciate your quick reply, but this is in particular a new business, producing a whole new product and there’s no such product in the market, so presently do not know how well the company will perform in the market place therefore feel it would be prudent to capitalize the lease rentals and wait for the option time to exercise or not and depreciate the residual based on the remaining life. in your opinion what do you think.

Thanks,

Hannan

Well, if this is your best judgment and estimate, then do so. However – is it probable that you would run the operations just for those 3 years and then abandon the business if it is not satisfactory? Speak to your managers about it and you will be on the safe side.

Dear Silvia, appreciate your prompt reply as always.

Hannan

Hi Silvia,

If the company entered into a lease contract with 2 years and it can be terminated within 2 months notices after 1 year. Can we apply for the exemption and just charge the rental into Profit & Loss?

Thanks

Hi Susanna

In the given scenario, the initial lease term is 14 months i.e. 12 months break period and 2 moths notice period thereafter. Hence, you can’t apply for exemption in this case.

Thanks

If a lease contract renews every year than in that case what will be the lease end term to be taken?

Hi Silvia,

My company is currently renting an office from the landlord. It’s not cancelable until Sept 2019. My question is on Jan 1, 2019, can we use the practical expedient to count the rest of the lease as operating lease(not to recognized ROU)? or we have to recognize it retrospectively?

Thanks!

HI Silvia

If the contract term ends and the assets then continues on a month to month basis – can it then be expensed until a decision is made whether to return the asset or renew the contract terms

If you assess that both parties can cancel within 12 months unilaterally, then yes. And I assume yes, because you have no contract after the original term expires.

Hi Silvia,

Thanks for the detailed explanation. If a company has property (under IAS 40) that has been given on rent and it is earning rental income. Is IFRS 16 applicable from lessor point of view ?

Thanks

Haroun

Oh yes!

Hi

Does the branch of a limited company which only prepare profits & loss account and receipt payment accountrequire to follow IFRS 16 ?

Dear Silvia thanks again for nice explanation ! Please advise if a company hires marine vessels mostly for period of time less than 12 months but it also has several vessels with lease contracts for more than 12 months how it should recognize them :separately , as short terms and long terms(ROU) or all lease contracts with ROU?

Hi Olga, of course, separately.

Thanks for the answer.

Just to be clear, regarding accounting treatment, should the rental expenses be booked as per actual rental cost payable or should it be on a straight line basis over the term of the lease by taking into account 10% increment on rent amount every 2 years ?

If there’s no right of use asset and you book the expenses straight in profit or loss, then you book them as they are incurred.

Hi Silvia

If there is a right of use asset does it have to be straight lined first by taking into account increments?