Sometimes, when you need to acquire some land, you often purchase it with some obstacles on it – you know, old structures like buildings, roads, fences, and other things.

What to do with the costs incurred to remove these obstacles?

In today’s article, I respond to the question from Zareena, Malaysia:

“We are auditors and need your advice on the following situation for our client:

They have freehold land with building with total cost of CU 20 mil. acquired in 2015.

The building was partly demolished in 2017 just before the year-end and right after the year end, the demolition was completed and the client intends to sell the land.

The company never split the total cost of CU 20 mil. between the land element and building element and the depreciation of building was never charged.

What shall be done with the demolition cost and the old building?”

Answer: Determine the intention!

Hmmm, I came across the same question many times during my work and it seems many companies face more-less the same issue, just slightly twisted.

Let’s start with properties for own use under IAS 16 and let’s start with the demolition cost.

Demolition cost under IFRS

IAS 16 Property, Plant and Equipment does NOT directly address the demolition or removal of obstacles.

Under IAS 16 par. 16, the cost of an item of property, plant and equipment includes any costs directly attributable to bringing the asset to the location and condition necessary for it to be capable of operating in the manner intended by the management.

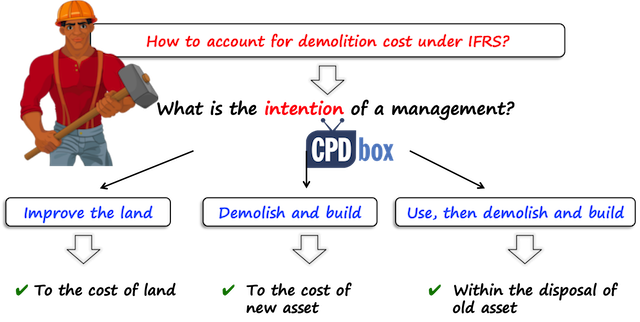

What was the intention of the management when they purchased the building together with the land?

Always look to the original intention or the reason why the building and land were acquired, because this will give you further direction.

There are few scenarios possible:

- Scenario n. 1: The company acquired land with building to demolish the building, make some improvements on the land and then sell the land.In this case, the intention was to acquire the land and the demolition cost of building is seen simply as a cost directly attributable to bringing the land to the condition to be operated in the manner intended by the management.Logically, you should add these demolition costs to the cost of the land as some land improvement.

- Scenario n. 2: The company acquired land with building to demolish the building, develop the site, build a new building and then use it.In this case, it’s a bit more complicated, because the intention is to have the new building and IAS 16 says in par. 58 that the building and land shall be classified as two separate items.Primary intention was to build a new building and therefore, demolition costs of old building are incremental to the new building, or in other words – you would not incur the demolition cost without wanting to build the new building.

So, in this case, you should capitalize the demolition costs to the cost of new building.

- Scenario n.3: The company acquired land with building, then used the old building for some short time and then demolished it with the intention to build a new building.In this case, the management’s intention at acquisition was to use the existing structure and thus demolition relates to the disposal of the old building.Therefore, you would not capitalize it to the cost of new building, but you would expense it as incurred.

You should also be careful about the fact that the demolition should occur within some reasonable time after the acquisition in order to prove the intention.

For example, you acquired the land and building in 2016 and you did nothing, and then in 2018 you decided to demolish the building and sell the land.

In this case, it’s questionable whether it was your intention to do so and whether you can simply say it’s the land improvement.

OK, that’s it for the demolition cost itself.

Carrying amount of old buildings

What should you do with the carrying amount of the old structures or buildings? Can you capitalize them to the cost of new buildings? Or expense?

There is no clear IFRS guidance on this point, but there are some accepted practices and other available guidance.

The main aspect to examine is how the old building was acquired and previously used:

- If you previously used the old building yourself and you decided to demolish it and build the new one, then you should simply derecognize the old building with gain or loss reported in profit or loss.More specifically, there’s usually some period between the decision to demolish and actual demolition, so you should probably accelerate depreciation over shorter remaining useful life and test the building for any impairment under IAS 36.

- If you acquired the land with old building to demolish it and build the new asset, the cost of the old building is incremental to the acquisition of the new assets and it’s appropriate to allocate the full purchase price to the land without splitting it.In most cases this would be acceptable, because you would rarely purchase highly valuable building with intention to demolish it, so rationally, the value of the old structure is low anyway.

Sometimes it’s not so simple.

It may happen that you acquired land with building with intention to demolish it, but that building has some fair value, it’s usable, but you want this location and you want to remove that structure anyway.

Here, there are strong arguments for not including the carrying amount of old building to the cost of the land, because IAS 16 requires splitting the land and building element and also, the building has its fair value regardless the buyer wants to demolish it or not.

In this case, you might need to allocate some part of the purchase price to the building and write it off in profit or loss. But again, you have to determine the fair value of old building really carefully with regard to the area, alternative use, etc.

Until now, I wrote about the case when you acquire building for your own use or for rentals – that would be more-less the same.

Developers: demolition within ordinary course of business

What about the developers and constructors who buy the lands with buildings and demolish them within the ordinary course of their business?

Here we are dealing with inventories under IAS 2 Inventories, so yes, the cost of old building and demolition cost are treated as inventories and it means that you need to keep inventories at lower of cost and net realizable value.

Example: Old building with land

ABC acquired a land with old building for CU 400 000 with intention to demolish the building and build the new one.

The building’s fair value is close to zero, because it is damaged and can be used only after significant investments into repairs and refurbishment.

ABC spent CU 20 000 to demolish the building.

In this case, it is appropriate to allocate all purchase price to the land.

As ABC plans to build the new building, the demolition cost is directly attributable to is and is included to the cost of the new building.

The entries are:

- Acquisition of the land:

- Debit PPE – Land: CU 400 000

- Credit Cash: CU 400 000

- Demolition cost:

- Debit PPE – New building: CU 20 000

- Credit Cash: CU 20 000

Here’s the video summing up this issue:

Do you have your own question? Send it here!